Blank Utah Tc 941D Form

In the ever-evolving landscape of business operations and tax obligations, companies find themselves navigating through myriad forms and requirements to stay in compliance with state laws. Utah is no exception, offering a specialized tool for businesses undergoing changes—a tool designed to ensure that tax withholdings are accurately reported and reconciled. This tool, the Utah Tc 941D form, serves as a critical piece for businesses that have experienced a change in entity type or merged with another company during the tax year, ensuring their tax documentation accurately reflects these changes. Detailed instructions guide businesses through the reconciliation process, requiring them to document discrepancies between reported withholdings on the Annual Withholding Reconciliation (form TC-941R) and the actual W-2s or other withholding documents issued. The form not only facilitates the smooth correction of these discrepancies but also outlines scenarios like entity conversions and mergers that may necessitate such adjustments. Moreover, it provides a structured reconciliation calculation method, allowing for a straightforward comparison and adjustment of withholding totals to mirror accurate annual tax withheld amounts. With penalties in place for inaccuracies, the encouragement towards precision and correctness is unequivocal, emphasizing the form’s role in maintaining the integrity of tax reporting for businesses within Utah.

Form Preview Example

Get forms online - tax.utah.gov

Utah State Tax Commission

Discrepancy Report

For Annual Withholding Reconciliation

Rev. 5/12

Tax year for this report

Check box if Amended Report

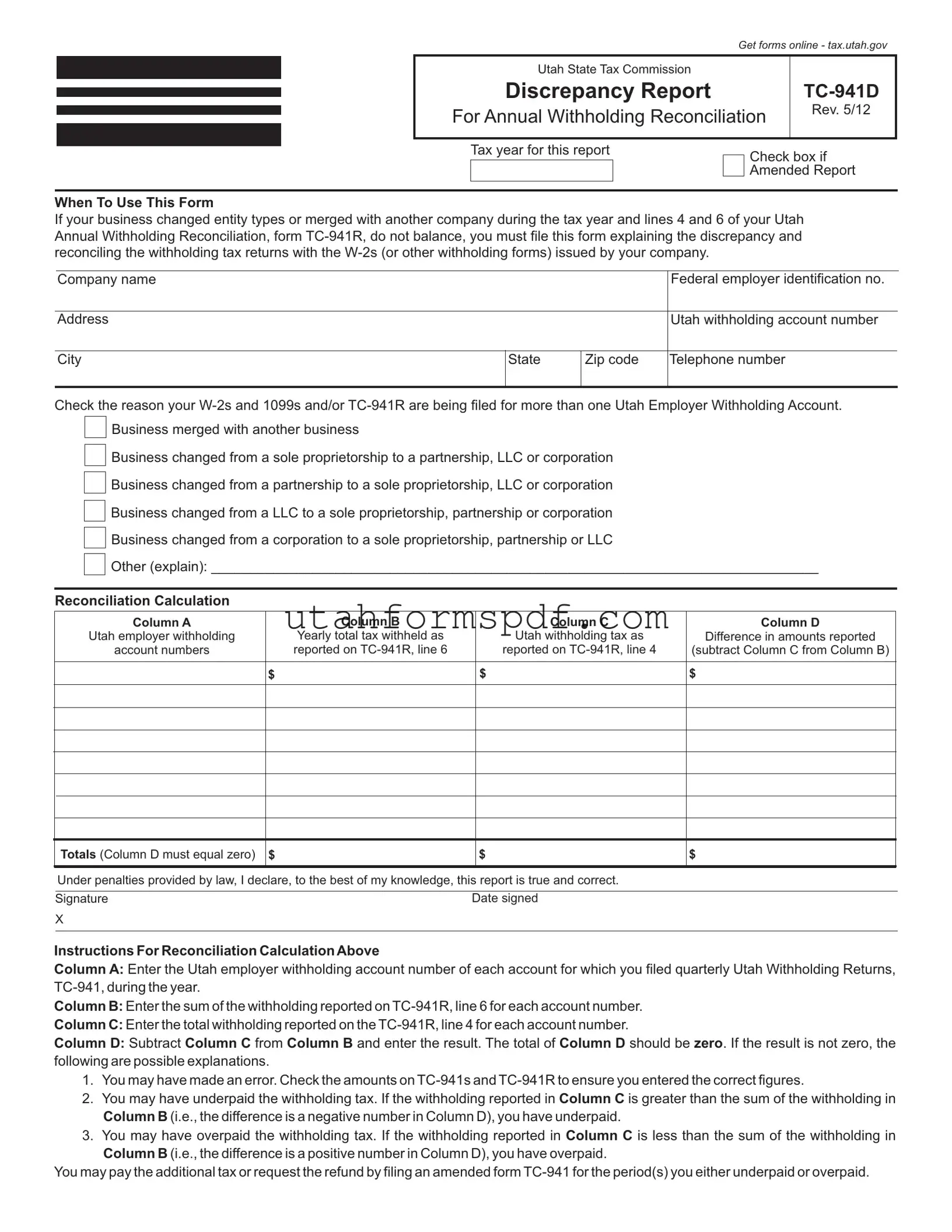

When To Use This Form

If your business changed entity types or merged with another company during the tax year and lines 4 and 6 of your Utah Annual Withholding Reconciliation, form

Company name

Federal employer identification no.

Address

Utah withholding account number

City

State

Zip code

Telephone number

Check the reason your

Business merged with another business

Business changed from a sole proprietorship to a partnership, LLC or corporation

Business changed from a partnership to a sole proprietorship, LLC or corporation

Business changed from a LLC to a sole proprietorship, partnership or corporation

Business changed from a corporation to a sole proprietorship, partnership or LLC

Other (explain): ______________________________________________________________________________

Reconciliation Calculation

Column A |

Column B |

Column C |

Column D |

Utah employer withholding |

Yearly total tax withheld as |

Utah withholding tax as |

Difference in amounts reported |

account numbers |

reported on |

reported on |

(subtract Column C from Column B) |

|

|

|

|

$ |

$ |

|

$ |

Totals (Column D must equal zero)

$

$

$

Under penalties provided by law, I declare, to the best of my knowledge, this report is true and correct.

Signature |

Date signed |

X |

|

|

|

Instructions For Reconciliation Calculation Above

Column A: Enter the Utah employer withholding account number of each account for which you filed quarterly Utah Withholding Returns,

Column B: Enter the sum of the withholding reported on

Column C: Enter the total withholding reported on the

Column D: Subtract Column C from Column B and enter the result. The total of Column D should be zero. If the result is not zero, the following are possible explanations.

1.You may have made an error. Check the amounts on

2.You may have underpaid the withholding tax. If the withholding reported in Column C is greater than the sum of the withholding in Column B (i.e., the difference is a negative number in Column D), you have underpaid.

3.You may have overpaid the withholding tax. If the withholding reported in Column C is less than the sum of the withholding in Column B (i.e., the difference is a positive number in Column D), you have overpaid.

You may pay the additional tax or request the refund by filing an amended form

Form Breakdown

| Fact Name | Description |

|---|---|

| Form Purpose | The Utah TC-941D form is specifically designed to report and reconcile discrepancies in withholding tax amounts between the Annual Withholding Reconciliation (form TC-941R) and the W-2s or other withholding forms issued by a company. |

| When to Use | This form should be used if a business has undergone changes such as entity type modifications or mergers during the tax year, leading to imbalances between lines 4 and 6 on the TC-941R form. |

| Reconciliation Calculation | Companies must report Utah employer withholding account numbers, total yearly tax withheld, Utah withholding tax as reported, and the difference that must equal zero in the reconciliation calculation section. Errors in this section could indicate underpayment or overpayment of the withholding tax. |

| Governing Law | This form is governed by Utah state law, specifically relating to the procedures set forth for reporting and reconciling withholding taxes by businesses operating within the state. |

Detailed Steps for Writing Utah Tc 941D

Filling out the Utah TC-941D form is a step forward in ensuring your business's tax records are accurate and up to date, especially if your company has undergone significant changes such as merging or altering its business type within the tax year. This form is used to explain and reconcile any differences between your annual withholding reconciliation and the W-2s or other withholding documents your business issued. By carefully following the instructions below, you can successfully complete and submit your form to align with Utah State Tax Commission requirements.

- Gather all required documents: Before you start filling out the form TC-941D, ensure you have your completed Utah Annual Withholding Reconciliation form TC-941R and all W-2s (or other relevant withholding forms) issued by your company.

- Fill in basic company information: At the top of the form, write your company name, federal employer identification number, Utah withholding account number, and your company’s address including city, state, and zip code. Don’t forget to add your telephone number.

- Indicate the report type: Check the box next to "Amended Report" if you are filing an amendment to a previously submitted report. If this is your first report for the tax year in question, leave it unchecked.

- Select the reason: Check the appropriate box that describes why your W-2s and 1099s and/or TC-941R are being filed for more than one Utah Employer Withholding Account. If none of the provided reasons apply, select "Other" and provide a brief explanation in the space provided.

- Complete the Reconciliation Calculation section:

- Column A: Enter the Utah employer withholding account number for each account for which you filed quarterly Utah Withholding Returns, TC-941, during the year.

- Column B: For each account listed in Column A, enter the sum of the withholding reported on TC-941R, line 6.

- Column C: Enter the total withholding reported on the TC-941R, line 4 for each account number listed in Column A.

- Column D: Subtract the amount in Column C from Column B for each account and enter the result. The totals of Column D must equal zero to show that your reconciliation is balanced.

- Examine the results in Column D: If the result is not zero, review your calculations. A non-zero result could indicate an error, or that you've either underpaid or overpaid the withholding tax. In such cases, consider filing an amended TC-941 form for the relevant period(s).

- Sign and date the form: After you've completed all necessary calculations and confirmed the accuracy of the information provided, sign and date the form at the bottom. This acts as a declaration that, to the best of your knowledge, the information is correct and true.

Once your Utah TC-941D form is completely filled out and you've double-checked for accuracy, it's time to submit it to the Utah State Tax Commission. Typically, you would send it to the address provided by the Commission or as directed in the instructions accompanying the form. Timely submission ensures your business remains compliant with Utah's tax laws, helping you avoid potential penalties and interest for any discrepancies in your reported withholdings.

Common Questions

Frequently Asked Questions about the Utah TC-941D Form

- What is the purpose of the Utah TC-941D form?

The Utah TC-941D form, also known as the Discrepancy Report for Annual Withholding Reconciliation, is intended for businesses to explain and reconcile any differences between the total annual withholding tax reported on their Utah Annual Withholding Reconciliation (form TC-941R) and the actual withholding amounts documented on W-2s or other withholding forms. This form is necessary when discrepancies occur due to changes in business entity types or mergers with other companies during the tax year.

- When should a business file the TC-941D form?

A business should file the TC-941D form whenever discrepancies between lines 4 and 6 of the TC-941R cannot balance. This might be the result of the business undergoing a change in entity type, such as transitioning from a sole proprietorship to a corporation or merging with another business. Filing this form is required to ensure accurate reconciliation of withheld tax amounts against reported totals.

- How do I complete the reconciliation calculation on the TC-941D form?

Completing the reconciliation calculation involves a few steps. First, in Column A, list each Utah employer withholding account number for which you filed quarterly Utah Withholding Returns (TC-941) during the year. Next, in Column B, write the total withholding reported on TC-941R, line 6, for each account. Then, in Column C, enter the total withholding reported on the TC-941R, line 4, for each account number. Finally, subtract Column C from Column B and report the result in Column D. The total in Column D should be zero to indicate no discrepancy. If not, it suggests either an overpayment or underpayment of withholding tax.

- What are the next steps if I discover an overpayment or underpayment?

If, upon completing the TC-941D form, you find that you have overpaid or underpaid the withholding tax (as indicated by a positive or negative number in Column D, respectively), you must rectify this discrepancy. For overpayments, you can request a refund by filing an amended TC-941 for the specific period(s) where the overpayment occurred. For underpayments, you should also file an amended TC-941 form for the respective periods to pay the additional tax owed.

- Where can I find the TC-941D form?

The Utah TC-941D form is available online through the official website of the Utah State Tax Commission at tax.utah.gov. This enables easy access to the form for taxpayers needing to report discrepancies in their annual withholding reconciliation. It's recommended to download the form directly from the website to ensure you have the most current version.

Common mistakes

Filling out the Utah TC-941D form, an important document for employers to reconcile discrepancies in their withholding tax reports, can be challenging. The accuracy of this form is crucial for ensuring compliance with tax laws and avoiding potential penalties. Unfortunately, several common mistakes are made during this process which can impact the accuracy of the submitted form.

- Incorrect Employer Identification Number: One of the most critical errors involves entering an incorrect Federal Employer Identification Number (EIN). This mistake can lead to misidentification and processing delays, as this number ties the form to the specific entity reporting the taxes.

- Not Checking the Amended Report Box When Applicable: If submitting an amended report, failing to check the appropriate box can cause confusion and may result in the incorrect processing of the form as an original submission rather than as a correction to previously filed information.

- Entity Type Confusion: It's important to correctly identify changes in business entity types when they occur. Misidentifying the business's current status can lead to discrepancies in reported information, especially if the change in structure affects tax liabilities or reporting requirements.

- Miscalculations in Reconciliation Columns: Miscalculating the totals in the reconciliation calculation section is a common error, especially in Columns B, C, and D. These figures need to align precisely with the company's financial records and previously submitted forms (TC-941R).

- Failure to Accurately Report Mergers or Changes: Not correctly checking the reason for filing more than one Utah Employer Withholding Account, especially in cases of mergers or entity changes, overlooks the necessity of detailing these significant changes, potentially leading to reconciliation issues.

- Omitting Account Numbers: Neglecting to enter the Utah employer withholding account number for each account can delay processing. Each number is essential for identifying the specific accounts and returns being reconciled.

- Incorrect Year Entered: Entering the wrong tax year can lead to significant confusion and may result in the form being processed for an incorrect period, affecting tax liabilities for both the reported and actual required years.

- Ignoring Discrepancies: Not addressing or incorrectly explaining discrepancies between reported withholding amounts on TC-941R and W-2/1099 forms can trigger audits or penalties, especially if these discrepancies suggest underpayment or overpayment of taxes.

- Unsigned or Undated Forms: Submitting a form without the necessary signature and date compromises its validity. The declaration under penalty of perjury that the information provided is true and correct is a critical component of the form's submission process.

In all instances, carefully reviewing the form instructions and verifying all entered information can prevent these common errors. Proper attention to detail ensures compliance, helps maintain the company's good standing with tax authorities, and avoids unnecessary penalties.

Documents used along the form

When dealing with the complexities of business tax compliance in Utah, particularly with the TC-941D form—designed for Annual Withholding Reconciliation discrepancies—it is crucial to be well-prepared with the right documentation. The TC-941D form serves as a pivotal piece in ensuring that your business's withholding tax records are accurately aligned with the tax filings and the distributed W-2s or 1099s. However, navigating these waters smoothly often requires a set of complementary forms and documents, each serving a unique role in the reconciliation and reporting process.

- TC-941R (Utah Annual Withholding Reconciliation): This form is foundational for reconciling the total annual withholding tax reported to the state with the amounts withheld from employees' wages as indicated on W-2s and 1099s.

- TC-941 (Utah Withholding Tax Return): Filed quarterly, this document reports the total income tax withheld from employees' wages during each quarter, forming the base data for annual reconciliation.

- W-2 (Wage and Tax Statement): Employers use this to report annual wages and the amount of taxes withheld from their employees' paychecks to the IRS and the employee, integral for cross-verifying with TC-941R.

- 1099 Forms: These documents are used for reporting income other than salaries, wages, and tips. For businesses, forms like 1099-NEC and 1099-MISC are essential for reporting payments made to non-employees, which must align with the records reported on TC-941R.

- Utah State Tax Commission Power of Attorney (Form TC-737): This form may be needed if a business delegates the task of dealing with tax discrepancies and reconciliations to an external accountant or agent.

- Amended Return Filing Instructions: Not a form per se, but a critical document that provides detailed guidance on how to correctly file amended returns if errors are discovered in previously filed TC-941 or TC-941R forms.

- TC-40W (Withholding Tax Schedule): This document is crucial for individual tax return filings in Utah, ensuring that personal state income tax credits are correctly claimed for all withheld taxes reported on W-2s and 1099s.

The landscape of tax documentation and compliance is intricate, each form playing a specific role in ensuring businesses meet their responsibilities accurately and on time. Properly completing and understanding the interplay among forms like the TC-941D, TC-941R, and associated documents helps maintain the fiscal health of your business and ensures compliance with state tax laws. It is always advisable to consult with a tax professional or accountant to navigate these requirements effectively and ensure all documentation is correctly prepared and submitted.

Similar forms

The Form 941, Employer's Quarterly Federal Tax Return, shares similarities with the Utah TC-941D form in its focus on reconciling company payroll taxes. Both documents are essential for businesses to report earnings, withholdings, and payroll taxes to government tax agencies. Form 941 is a federal requirement that details the amount of income, Social Security, and Medicare taxes withheld from employees' paychecks by the employer. While the TC-941D is specific to discrepancies in annual withholding reconciliation for Utah, Form 941 serves the broader purpose of quarterly reporting on a national scale. Despite their different intervals and jurisdictional focuses, both forms play critical roles in ensuring tax compliance and accuracy in withheld payroll taxes.

The W-2, Wage and Tax Statement, is another document closely related to the Utah TC-941D form, as it provides detailed information on employee earnings and taxes withheld over the tax year. Employers are required to furnish W-2 forms to their employees and file copies with the Social Security Administration. When discrepancies arise in the reconciliation process outlined by the TC-941D, it often involves cross-referencing the figures reported on W-2 forms. The necessity to explain discrepancies between aggregated W-2 withholdings and reported amounts on the Utah Annual Withholding Reconciliation highlights their interconnection in accurately reporting and reconciling an employer's tax liability.

The 1099 series, including forms like the 1099-NEC and 1099-MISC, is akin to the TC-941D form in terms of reporting income and withholdings, but for non-employees. Similar to the role W-2s play for employee compensation, 1099 forms are used for reporting payments made to independent contractors and other non-employees. In situations where a business’s annual withholding reconciliation involves payments reported on 1099 forms, the TC-941D form becomes relevant. The process of identifying discrepancies may require an analysis of payments and withholdings reported on 1099 forms, underscoring the similarity in their use for clarifying and justifying tax withholdings to tax authorities.

Form W-3, Transmittal of Wage and Tax Statements, is closely related to the Utah TC-941D form as it accompanies W-2 forms sent to the Social Security Administration. It summarizes the total earnings, Social Security wages, Medicare wages, and withholding for all employees for the year. When discrepancies arise on the TC-941D, it's often necessary to review the W-3 to ensure the totals match what was reported throughout the year and reconciled on the Utah Annual Withholding Reconciliation. Both forms serve as summary documents that facilitate the reconciliation process and ensure compliance with reporting requirements.

The Utah Annual Withholding Reconciliation, form TC-941R, is directly related to the TC-941D discrepancy report. The TC-941R is the summary of withholding for the entire year and directly precedes the need for the TC-941D when discrepancies are discovered. The TC-941D serves as a follow-up to address and explain any differences between what was initially reported via the TC-941R and the actual withholdings for the year. The direct relationship between these forms highlights the step-by-step process Utah employs to ensure accurate withholding tax reporting and reconciliation.

Form TC-941, Utah Employer's Quarterly Withholding Return, while addressing a different reporting period, is fundamentally similar to the TC-941D in its focus on withholding tax. Employers in Utah use the TC-941 to report and pay taxes withheld from employees' wages each quarter. When discrepancies arise in annual totals, as reported on the TC-941R, the TC-941D is employed to reconcile these differences. Thus, both the quarterly and the discrepancy report forms are integral components of Utah's system for monitoring and ensuring the accuracy of withheld payroll taxes.

The Change of Entity Form, often required when a business undergoes a significant change in structure, has an indirect relation to the Utah TC-941D form. Such changes can affect the reporting and reconciliation process of withholding taxes as indicated on the TC-941D. For instance, if a business transitions from a partnership to a corporation or undergoes a merger, these structural adjustments could explain discrepancies in withholding tax reports. While the Change of Entity Form itself does not deal directly with tax withholdings, the ramifications of such changes bear significantly on the circumstances under which a TC-941D form would need to be filed.

The Amended Federal Tax Return (Form 1040-X), serves a purpose analogous to the Utah TC-941D, although in the realm of individual income taxes. When individuals discover discrepancies or need to make changes to previously filed tax returns, they use Form 1040-X to correct the record. Similarly, the TC-941D allows businesses to rectify discrepancies in reported versus actual withholding taxes. Despite serving different taxpayer categories, both forms underscore the tax systems’ mechanisms for ensuring accuracy and providing pathways to correct past submissions.

Dos and Don'ts

When filling out the Utah TC-941D form, a Discrepancy Report for Annual Withholding Reconciliation, it is important to follow specific guidelines to ensure accuracy and compliance with state tax laws. Below is a list of things you should and shouldn't do:

- Do:

- Ensure you're using the form for the correct tax year. This is essential to provide accurate information for the specified period.

- Check the "Amended Report" box if you are making corrections to previously submitted information, to clearly indicate the revision.

- Provide your company name, federal employer identification number, address, Utah withholding account number, city, state, zip code, and telephone number accurately to avoid processing delays.

- Clearly indicate the reason for filing more than one Utah Employer Withholding Account by checking the appropriate box or providing a detailed explanation if you select "Other".

- Accurately fill out the reconciliation calculation section, ensuring Column A, B, C, and D are completed correctly. The total of Column D must equal zero to show no discrepancy.

- Sign and date the form, verifying the information is true and correct to the best of your knowledge under penalty of law.

- Don't:

- Leave any section blank. If a section doesn’t apply, enter “N/A” to indicate this.

- Estimate or guess figures in the reconciliation calculation. Ensure you double-check these figures against your records for accuracy.

- Forget to review the entire form for errors before submission, as mistakes can lead to processing delays or require filing an amended report.

Adhering to these guidelines will help ensure the accurate and timely processing of your Utah TC-941D form. It's crucial to provide complete and correct information to meet regulatory requirements and support your business's compliance with Utah's tax laws.

Misconceptions

Understanding the Utah TC 941D form is crucial for businesses operating within the state. However, there are several misconceptions about this form that can cause confusion. Addressing these will help ensure compliance with Utah State Tax Commission requirements.

Misconception 1: The TC 941D form is required for all businesses.

Actually, only businesses that have experienced changes in entity type or mergers, resulting in discrepancies on their TC-941R form, need to file the TC 941D form.Misconception 2: The TC 941D can be used to report new employees.

This form is specifically for reporting discrepancies between withholding tax returns and W-2s or other withholding documents, not for reporting new hires.Misconception 3: Filing the TC 941D rectifies all issues with withholding taxes.

While it’s used to explain discrepancies, additional steps may be necessary to fully resolve withholding tax issues.Misconception 4: Only corporations need to file the TC 941D when there are discrepancies.

In truth, any business entity that faces the specified discrepancies must file this form, regardless of its structure.Misconception 5: The TC 941D form replaces the need for an amended TC-941R form.

Actually, in some cases, you may also need to file an amended TC-941R alongside the TC 941D for complete reconciliation.Misconception 6: Businesses do not need to explain the discrepancies in the TC 941D.

Contrary to this belief, a thorough explanation of the discrepancies is essential for filing this form correctly.Misconception 7: Any discrepancy requires filing the TC 941D immediately.

First, discrepancies should be reviewed to ensure they are not clerical errors that can be corrected otherwise.Misconception 8: You need to file a TC 941D form every tax year.

This form is only necessary when specific discrepancies that can’t be corrected through normal amendments arise.Misconception 9: The TC 941D form can be filed electronically at any time.

While electronic filing may be available, it is important to confirm the current filing requirements and deadlines with the Utah State Tax Commission.Misconception 10: Filing the TC 941D form is voluntary.

If the conditions described for the form apply to your business, filing is mandatory to remain compliant with state tax laws.

Understanding these key points about the Utah TC 941D form will aid in accurate and timely compliance, ensuring that your business operations proceed smoothly without unnecessary tax obstacles.

Key takeaways

Filling out and using the Utah TC-941D form is a crucial process for businesses that have undergone changes in their entity type or merged with another company during the tax year. Here are key takeaways to guide you through the process:

- The Utah TC-941D form serves as a discrepancy report for annual withholding reconciliation, primarily used when there is a mismatch between the tax withheld as per Utah Annual Withholding Reconciliation (form TC-941R) and the withholding forms issued to employees or contractors.

- It is specifically needed if your business's entity type has changed or if a merger occurred during the tax year, leading to inconsistencies in withholding tax reporting.

- The form requires information about the company, including the company name, federal employer identification number, address, Utah withholding account number, and contact details.

- Reasons for filing the form can vary from business mergers to changes in the business's formation type, such as shifting from a sole proprietorship to a corporation or vice versa.

- Reconciliation calculation involves detailing Utah employer withholding account numbers and comparing the yearly total tax withheld against the reported Utah withholding tax, aiming to identify any discrepancies.

- The difference in reported and actual withholding amounts must ideally be zero; discrepancies might indicate overpayment or underpayment of withholding taxes.

- In cases of overpayment or underpayment, businesses can rectify their tax obligations by filing an amended form TC-941 for the respective periods.

- Accuracy is paramount when filling out the TC-941D form. Errors in reporting or calculation can result in processing delays or potential issues with tax compliance.

The completion and submission of the Utah TC-941D form is a testament to a business's commitment to ensuring tax compliance and financial integrity. Proper attention to detail and understanding of tax obligations are essential for accurately reconciling withholding taxes and maintaining good standing with the Utah State Tax Commission.

Common PDF Templates

What to Write on Subject When Sending an Email for a Job Sample - The application form is not just a tool for gathering data but also a pledge of the State's commitment to fair and inclusive hiring practices.

Utah State Withholding - Requirements for providing organizational dates and identifying numbers help ensure that businesses are properly cataloged from the start.

Utah 15C - Ensuring the 15C form is filled out with the most current and accurate information facilitates a smoother permitting process.