Blank Utah Tc 65 Form

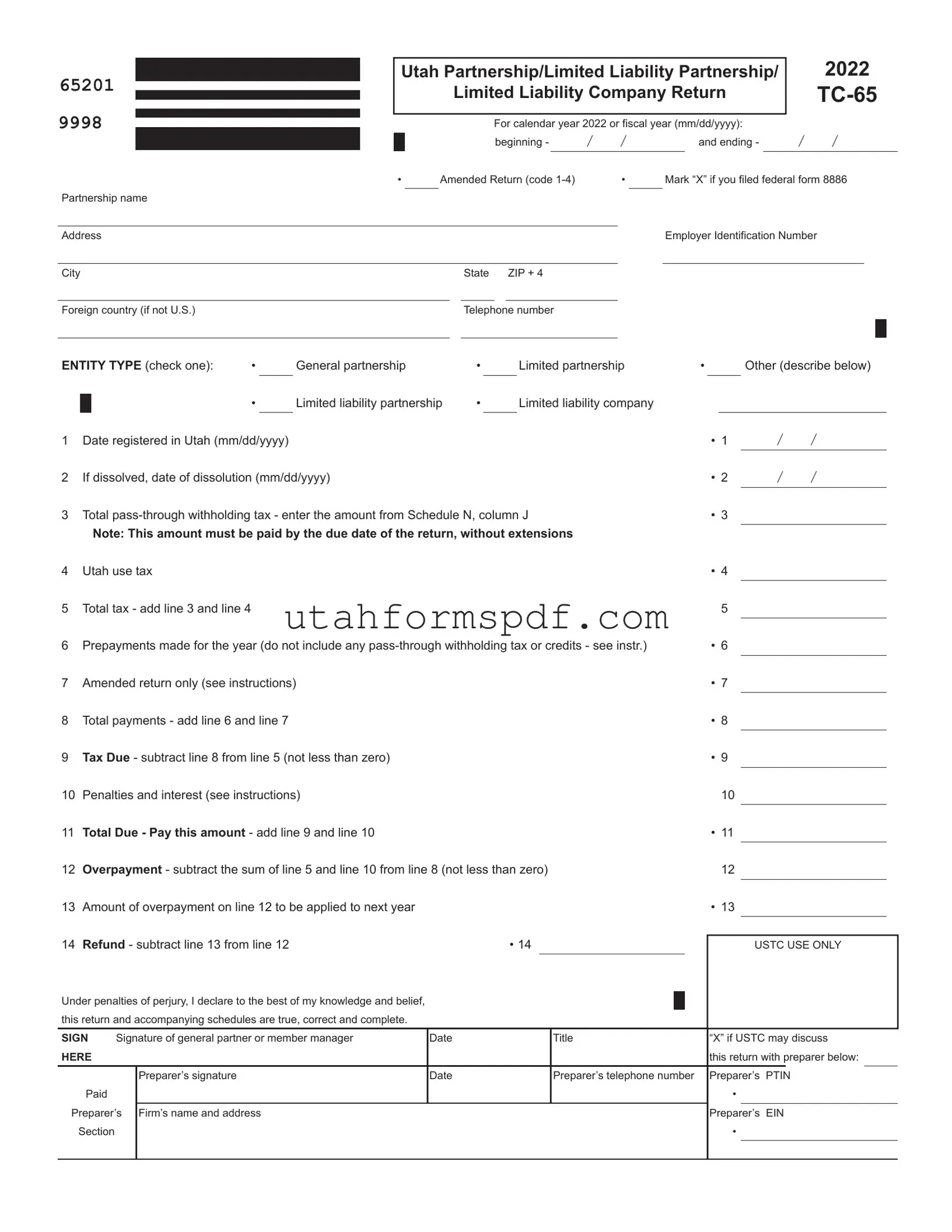

Businesses operating within Utah that are structured as partnerships or limited liability companies (LLCs) find the TC-65 form crucial for tax purposes. This document, officially known as the Utah Partnership/Limited Liability Company Return, is designed for the calendar year 2020 or the corresponding fiscal year, offering a structured way to report income, deductions, and taxes owed to the state. The form accommodates various entity types, including general partnerships, limited partnerships, limited liability partnerships, and LLCs, ensuring a broad spectrum of business structures can comply with state tax obligations. It encompasses sections for detailing the partnership's financial activities, calculating Utah use tax, and managing pass-through withholding tax, all of which are essential for transparent and accurate tax reporting. Amendments to the return can be indicated directly on the form, highlighting its flexibility to accommodate changes. Moreover, completions of schedules like Schedule A for Utah Taxable Income, Schedule H for Utah Nonbusiness Income, and Schedule J for Apportionment underscore the comprehensive nature of this form in facilitating detailed tax calculations. The form demands meticulous attention to detail, from income reporting to tax calculations and apportionment, ensuring that partnerships and LLCs operating in Utah maintain compliance while accurately reflecting their fiscal activities within the state.

Form Preview Example

65201

9998

USTC ORIGINAL FORM

Partnership name

Address

City

Utah Partnership/Limited Liability Partnership/ |

|

2022 |

||||||||||

|

|

Limited Liability Company Return |

|

|||||||||

|

|

For calendar year 2022 or fiscal year (mm/dd/yyyy): |

|

|

|

|||||||

|

|

beginning - |

/ |

/ |

|

|

and ending - |

/ |

/ |

|

||

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||

• |

|

Amended Return (code |

|

• |

Mark “X” if you filed federal form 8886 |

|||||||

|

|

|

|

|

|

|

Employer Identification Number |

|

|

|||

|

|

|

|

|

|

|

|

|

||||

|

|

State ZIP + 4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Foreign country (if not U.S.)Telephone number

ENTITY TYPE (check one): |

• |

General partnership |

• |

|

Limited partnership |

• |

|

Other (describe below) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

Limited liability partnership |

• |

|

Limited liability company |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Date registered in Utah (mm/dd/yyyy) |

|

|

|

|

|

|

• 1 |

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2 |

If dissolved, date of dissolution (mm/dd/yyyy) |

|

|

|

|

|

• 2 |

/ |

/ |

||||||

3 |

Total |

|

• 3 |

|

|

|

|||||||||

|

|

|

|

||||||||||||

|

|

Note: This amount must be paid by the due date of the return, without extensions |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

||||||||

4 |

Utah use tax |

|

|

|

|

|

|

|

|

• 4 |

|

|

|

||

5 |

Total tax - add line 3 and line 4 |

|

|

|

|

|

|

|

5 |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||||

6 |

Prepayments made for the year (do not include any |

|

• 6 |

|

|

|

|||||||||

|

|

|

|

||||||||||||

7 |

Amended return only (see instructions) |

|

|

|

|

|

• 7 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

8 |

Total payments - add line 6 and line 7 |

|

|

|

|

|

|

• 8 |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|||||||

9 |

Tax Due - subtract line 8 from line 5 (not less than zero) |

|

|

|

|

|

• 9 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

10 |

Penalties and interest (see instructions) |

|

|

|

|

10 |

|

|

|

||||||

|

|

|

|

|

|

|

|||||||||

11 |

Total Due - Pay this amount - add line 9 and line 10 |

|

|

|

|

|

• 11 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

12 |

Overpayment - subtract the sum of line 5 and line 10 from line 8 (not less than zero) |

12 |

|

|

|

||||||||||

|

|

|

|||||||||||||

13 |

Amount of overpayment on line 12 to be applied to next year |

|

|

|

|

|

• 13 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

14 |

Refund - subtract line 13 from line 12 |

|

|

• 14 |

|

|

|

|

|

||||||

|

|

|

|

|

|

USTC USE ONLY |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare to the best of my knowledge and belief, |

|

|

|

|

|

|

|

|

|

||

this return and accompanying schedules are true, correct and complete. |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

SIGN |

Signature of general partner or member manager |

Date |

Title |

“X” if USTC may discuss |

|||||||

HERE |

|

|

|

|

|

|

this return with preparer below: |

||||

|

|

|

|

|

|

|

|

|

|

||

|

|

Preparer’s signature |

Date |

Preparer’s telephone number |

Preparer’s |

PTIN |

|||||

Paid |

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Preparer’s |

Firm’s name and address |

|

|

|

|

Preparer’s |

EIN |

||||

Section |

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule A - Utah Taxable Income for |

||||||

65202 |

EIN |

|

|

2022 |

|

|

||

USTC ORIGINAL FORM |

|

|

|

|

||||

1 |

Net income/loss from federal form 1065, Schedule K, Analysis of Net Income (Loss), line 1 |

• 1 |

||||||

|

|

|

|

|

|

|||

2 |

Contributions from federal form 1065, Schedule K, line 13a |

• 2 |

||||||

|

|

|

|

|

|

|||

3 |

Foreign taxes from federal form 1065, Schedule K, line 21 |

• 3 |

||||||

|

|

|

|

|

|

|||

4 |

Recapture of Section 179 deduction from all federal Schedules |

• 4 |

||||||

|

|

|

|

|

|

|||

5 |

Payroll Protection Program grant or loan addback (see instructions) |

• 5 |

||||||

|

|

|

|

|

|

|||

6 |

(Reserved, see instructions) |

• 6 |

||||||

7 |

Total income/loss - add lines 1 through 6 |

7 |

|

|

|

|||

|

|

|

||||||

|

|

|

|

|

|

|||

8 |

Total guaranteed payments to partners (see instructions) |

• 8 |

||||||

|

|

|

|

|

|

|||

9 |

Health insurance included in guaranteed payments on line 8 |

• 9 |

||||||

10 |

Net guaranteed payments to partners - subtract line 9 from line 8 |

10 |

|

|

|

|||

|

|

|

||||||

|

|

|

|

|

||||

11 |

Utah net nonbusiness income from |

• 11 |

||||||

|

|

|

|

|

|

|||

12 |

• 12 |

|||||||

13 |

Add lines 10 through 12 |

13 |

|

|

|

|||

|

|

|

||||||

|

|

|

|

|

||||

14 |

Apportionable income/loss - subtract line 13 from line 7 |

• 14 |

||||||

|

|

|

|

|

||||

15 |

Apportionment fraction - enter 1.000000, or |

• 15 |

||||||

|

|

|

|

|

|

|||

16 |

Utah apportioned business income/loss - multiply line 14 by line 15 |

• 16 |

||||||

|

|

|

|

|

||||

17 |

Total Utah income/loss allocated to |

• 17 |

||||||

|

|

|

|

|

|

|

|

|

Schedule H - Utah Nonbusiness Income Net of Expenses |

Pg. 1 |

|||||

20261 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Failure to complete this form may result in disallowance of the nonbusiness income. |

|

|

|

|

|||||||

Part 1 - Utah Nonbusiness Income (nonbusiness income allocated to Utah) |

|

|

|

|

|||||||

|

|

|

|

||||||||

|

|

|

|

||||||||

|

A |

B |

|

|

C |

D |

|

E |

|||

|

Type of Utah |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

Utah Nonbusiness Income |

||||

|

Nonbusiness Income |

Utah Nonbusiness |

|

Used to Produce Utah |

Used to Produce Utah |

|

|

|

|||

|

|

|

Asset(s) |

|

|

Nonbusiness Income |

Nonbusiness Income |

|

|

|

|

1a |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1b |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1c |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1d |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1e |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

2Total of column C and column D

3Total Utah nonbusiness income - add column E for lines 1a through 1e

|

Description of direct expenses related to: |

Amount of Direct Expense |

||

4a |

Line 1a above |

|

||

|

|

|

|

|

4b |

Line 1b above |

|

||

|

|

|

|

|

4c |

Line 1c above |

|

||

|

|

|

|

|

4d |

Line 1d above |

|

||

|

|

|

|

|

4e |

Line 1e above |

|

||

|

|

|

|

|

5Total direct related expenses - add lines 4a through 4e

6 |

Utah nonbusiness income net of direct related expenses - subtract line 5 from line 3 |

|

• |

||

|

|

Column A |

Column B |

||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

||

|

Utah Nonbusiness Income |

Utah Nonbusiness Income |

|

|

|

7 |

|

|

|

|

|

|

(enter in Column A the amount from line 2, col. C) |

|

|

|

|

|

|

|

|

|

|

8

(enter in Column A the amount from line 2, col. D)

9Sum of beginning and ending asset values (add line 7 and line 8)

10Average asset value - divide line 9 by 2

11Utah nonbusiness assets ratio - line 10, Column A, divided by line 10, Column B (to four decimal places)

12Interest expense deducted in computing Utah taxable income (see instructions)

13Indirect related expenses for Utah nonbusiness income - multiply line 11 by line 12

14 Total Utah nonbusiness income net of expenses - subtract line 13 from line 6 |

|

• |

|

Enter on: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule H - |

Pg. 2 |

|||||

20262 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Part 2 -

|

A |

B |

|

|

C |

D |

|

E |

||

|

Type of |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

||||

|

Nonbusiness Income |

|

|

Used to Produce |

Used to Produce |

|

Income |

|||

|

|

|

Nonbusiness Asset(s) |

|

Nonbusiness Income |

Nonbusiness Income |

|

|

||

15a |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15b |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15c |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15d |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15e |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

16Total of column C and column D

17Total

|

Description of direct expenses related to: |

|

|

|

|

|

Amount of Direct Expense |

|

18a |

Line 15a above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18b |

Line 15b above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18c |

Line 15c above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18d |

Line 15d above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18e |

Line 15e above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 |

Total direct related expenses - add lines 18a through 18e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

20 |

• |

|||||||

|

|

|

Column A |

Column B |

|

|

||

|

|

|

|

|

||||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

|

|

|||

|

|

|

|

|

||||

21 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. C) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

22 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. D) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

23Sum of beginning and ending asset values (add line 21 and line 22)

24Average asset value - divide line 23 by 2

25

26Interest expense deducted in computing

27Indirect related expenses for

28 Total |

• |

|

Enter on: |

|

|

|

|

|

|

|

|

Schedule J - Apportionment Schedule |

Pg. 1 |

|||||

20263 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Use this schedule only if the entity does business in Utah and one or more other states and income must be apportioned to Utah.

Briefly describe the nature and location(s) of your Utah business activities:

Apportionable Income Factors

|

|

|

|

|

Column A |

|

Column B |

|||

1 |

Property Factor |

|

|

Inside Utah |

|

Inside and Outside Utah |

||||

|

a |

Land |

• 1a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

b |

Depreciable assets |

• 1b |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Inventory and supplies |

• 1c |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Rented property |

• 1d |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Other allowable property (see instructions) |

• 1e |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

f |

Total tangible property - add lines 1a through 1e |

• 1f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

2 |

Property factor - divide line 1f, Column A, by line 1f, Column B (to six decimal places) |

• |

2 |

|

|

|

||||

3 |

Payroll Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total wages, salaries, commissions and other compensation |

• 3a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

4 |

Payroll factor - divide line 3a, Column A, by line 3a, Column B (to six decimal places) |

• |

4 |

|

|

|

||||

5 |

Sales Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total sales (gross receipts less returns and allowances) |

|

|

|

• |

5a |

|||

|

b |

Sales delivered or shipped to Utah buyers from outside Utah |

• 5b |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Sales delivered or shipped to Utah buyers from within Utah |

• 5c |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Sales shipped from Utah to the United States government |

• 5d |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Sales shipped from Utah to buyers in states where the corp. |

• 5e |

|

|

|

|

|

||

|

|

has no nexus (corporation not taxable in buyer’s state) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f |

Rent and royalty income |

• 5f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

g |

Services and other allowable sales (see instructions) |

• 5g |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

h |

Total sales (add lines 5a through 5g) |

• 5h |

• |

|

|

|

|

||

|

|

|

|

|

|

|

||||

6 Sales factor - line 5h, Column A, divided by line 5h, Column B (to six decimals) |

• |

6 |

|

|

|

|||||

|

|

Continued on page 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule J - Apportionment Schedule |

Pg. 2 |

|||||

20264 EIN |

|

|

2022 |

|

|

|

||

USTC ORIGINAL FORM |

(use with |

|

|

|||||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

7 All entities - enter your NAICS code here (see instructions) |

• 7 |

|

|

||||

Apportionment Fraction |

|

|

|

|

||||

|

|

|

|

|||||

|

Optional apportionment taxpayers (see instructions) complete Part 1 or Part 2. |

|

|

|

|

|||

|

Sales factor weighted taxpayers (see instructions) complete Part 2. |

|

|

|

|

|||

Part 1:

8 |

Total factors - add lines 2, 4 and 6 |

|

8 |

9 |

Calculate the Apportionment Fraction to SIX DECIMALS |

• |

9 |

|

Divide line 8 by 3 (or the number of factors present) |

|

|

Part 2: Sales Factor Formula (see instructions for those who qualify) |

|

|

|

10 |

Apportionment Fraction - enter the |

• |

10 |

Enter the fraction from line 9 or line 10, above, as follows:

Schedule K - Partners’ Distribution Share Items |

|

|

|||

65203 EIN |

|

|

2022 |

||

USTC ORIGINAL FORM |

|

|

|

||

Number of Schedules |

• |

||||

|

|

|

|

|

|

Income/Loss

Deductions

Utah Credits

Federal Amount |

Utah Amount |

1Ordinary business income/loss

2Net rental real estate income/loss

3 Other net rental income/loss

4 Guaranteed payments

5a U.S. government interest income

5b Municipal bond interest income

5c Other interest income

6Ordinary dividends

7 Royalties

8 Net

9 Net

10 Net Section 1231 gain/loss

11 Recapture of Section 179 deduction

12 Other income/loss (describe)

13Section 179 deduction

14Contributions

15Foreign taxes paid or accrued

16Other deductions (describe)

17 Utah nonrefundable credits - enter the name of the Utah credit |

Code |

|

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18 Utah refundable credits - enter the name of the Utah credit |

Code |

|

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 Total Utah tax withheld on behalf of all partners from Schedule N, column J

|

Schedule |

|

65204 |

of Utah Income, Deductions and Credits |

2022 |

USTC ORIGINAL FORM

Partnership Information

APartnership’s EIN:

BPartnership’s name, address, city, state, and ZIP code

Partner Information

C Partner’s SSN or EIN:

D Partner’s name, address, city, state, and ZIP code

EPartner’s phone number

F Percent of ownership

G Enter “X” if limited partner or member

H Entity code from list below: |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I = Individual |

|

|

P = Gen’l Partnership |

|

|

||||||

|

C = Corporation |

|

L = Limited Partnership |

|

|

|||||||

|

Codes |

|

|

|

||||||||

|

S = S Corporation |

|

B = LLC |

|

|

|

|

R = LLP |

||||

|

N = Nonprofit Corp. |

|

T = Trust |

|

|

|

|

O = Other |

||||

|

|

|

|

|

|

|

||||||

I |

Enter date: |

|

/ |

/ |

/ |

/ |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

affiliated |

|

|

|

|

withdrawn |

|||

|

|

|

|

|

|

|

|

|

||||

Partner’s Share of Apportionment Factors |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

Utah |

|

|

|

|

|

Total |

|

J |

Property |

$ |

|

|

$ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||

K |

Payroll |

$ |

|

|

$ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

L |

Sales |

|

$ |

|

|

$ |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Information

Note: To complete lines 1 through 16:

*Utah residents, enter the amounts from federal Schedule

*Utah nonresidents, see instructions to calculate amounts.

All filers complete lines 17 through 19, if applicable.

Partner’s Share of Utah Income, Deductions and Credits

1Utah ordinary business income/loss

2Utah net rental real estate income/loss

3 Utah other net rental income/loss

4 Utah guaranteed payments

5a Utah U.S. government interest income

5b Utah municipal bond interest income

5c Utah other interest income

6Utah ordinary dividends

7 Utah royalties

8 Utah net

9 Utah net

10 Utah net Section 1231 gain/loss

11 Utah recapture of Section 179 deduction

12 Utah other income/loss (describe)

13Utah Section 179 deduction

14Contributions

15Foreign taxes paid or accrued

16Utah other deductions (describe)

17Utah nonrefundable credits:

Name of Credit |

Code |

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18 Utah refundable credits:

Name of Credit |

Code |

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19Utah tax withheld on behalf of partner “X” if withholding waiver applied for

Schedule N - |

|

|||

65205 EIN |

|

|

|

2022 |

USTC ORIGINAL FORM

A partnership with nonresident individual partners, resident/nonresident business partners, or resident/nonresident trust or estate partners must complete the information below to calculate the Utah withholding tax for these partners. See instructions for column G, column H and column I.

WITHHOLDING WAIVER CLAIMED under |

|

• |

|||||||||||||||||||||||||||

Enter "1" to claim a waiver for ALL partners (enter "X" in column B and "0" in column F for all partners) |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

Enter "2" to claim a waiver for SOME partners (enter "X" in column B and "0" in column F for those partners claimed) |

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||

|

See Schedule N instructions for liability responsibilities when claiming a waiver. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

A |

Name of partner |

|

|

|

|

E |

Income/loss |

F |

4.85% of income - |

G |

Mineral production |

J Withholding tax |

|||||||||||||||||

B |

Withholding waiver for this partner |

|

|

attributable to Utah |

|

|

E times .0485 |

|

|

|

withholding credit |

|

to be paid by |

||||||||||||||||

|

(enter “X” in column B and “0” in column F) |

|

|

plus Utah source |

|

|

(not less than zero) H |

|

this partnership |

||||||||||||||||||||

C |

SSN or EIN of partner |

|

|

|

|

|

|

guaranteed pymts |

|

|

|

|

|

|

|

through withholding |

|

F less G, H and I |

|||||||||||

D |

Partner’s % of income or ownership |

|

|

(see instructions) |

|

|

|

|

I Tax paid by PTE |

|

(not less than 0) |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

#1 |

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

|||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Report the partner’s |

|

|

|

|

Total Utah withholding tax to be paid by this partnership: |

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

tax from column J on Schedule |

|

|

|

|

Enter on |

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

Credits Received from |

|||

25201 and Mineral Production Withholding Tax Credit on |

2022 |

||

EIN |

|

|

(use with |

USTC ORIGINAL FORM

Part 1 - Utah Nonrefundable Credits Received from

1

2

3

4

5

6

|

|

|

|

UT nonrefundable |

Name of |

|

Credit |

credit from |

|

from Utah Schedule |

|

Code |

Utah Sch. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter these credits on Utah

Part 2 - Utah Refundable Credits Received from

Name of |

Credit |

UT refundable credit |

from Utah Schedule |

Code |

from Utah Sch. |

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Enter these credits on Utah

Part 3 - Utah Mineral Production Withholding Tax Credit Received on

|

|

Mineral production |

Producer EIN from |

|

withholding from |

Producer’s name from |

1

2

3

4

5

6

7

8

9

10

Total Utah mineral production withholding tax credit received on

Enter total credit on Utah

Form Breakdown

| Fact | Detail |

|---|---|

| Purpose | The Utah TC-65 Form is used for reporting the income, deductions, and tax for partnerships, limited liability partnerships (LLP), and limited liability companies (LLC) that are classified as partnerships for tax purposes. |

| Entity Types | This form accommodates various business structures, including general partnerships, limited partnerships, limited liability partnerships, and limited liability companies, providing flexibility in reporting for different organizational forms. |

| Governing Law | Administered under Utah state tax laws, the TC-65 form ensures compliance with state-level taxation requirements for pass-through entities operating within Utah. |

| Due Date | The form is due for the calendar year or fiscal year ending, with specifics provided by the Utah State Tax Commission. The due date is crucial for avoiding penalties and ensuring that the pass-through entity's tax responsibilities are fulfilled on time. |

Detailed Steps for Writing Utah Tc 65

Filling out the Utah TC-65 form is an essential process for partnerships and limited liability companies (LLCs) in Utah to comply with state tax obligations. This task may seem complex, but by breaking it down into step-by-step instructions, it becomes manageable. The aim is to ensure that your entity provides all required information accurately to avoid any issues with state tax filings. Once the form is completed and submitted, the next steps involve waiting for any communication from the Utah State Tax Commission, which may include confirmation of receipt, requests for additional information, or the assessment of taxes due.

- Start with filling out the basic information about your partnership or LLC at the top of the form, including the partnership name, address, city, state, ZIP code, and if applicable, the foreign country.

- Indicate whether this is an original or amended return by marking the appropriate box.

- Check the box that best describes the entity type: General partnership, Limited partnership, Limited liability partnership, or Limited liability company. If "Other" is selected, describe the entity type.

- Enter the Employer Identification Number (EIN).

- Provide the entity's telephone number.

- Specify the tax year or fiscal year that the return covers by filling in the beginning and ending dates.

- If applicable, mark "X" if you filed federal form 8886.

- Under "Entity Type," check the appropriate box for your organization's entity type.

- Enter the date the entity was registered in Utah.

- If the entity has been dissolved, enter the date of dissolution.

- On line 3, enter the total pass-through withholding tax amount from Schedule N, column I.

- Fill in the Utah use tax on line 4, if applicable.

- Calculate and enter the total tax on line 5 by adding lines 3 and 4.

- On line 6, list any prepayments made for the year.

- For an amended return, fill in the relevant information on line 7 as per instructions.

- Add lines 6 and 7 to calculate the total payments, and enter this on line 8.

- Determine the tax due by subtracting line 8 from line 5 and enter this on line 9.

- Calculate and list any penalties and interest on line 10.

- Add line 9 and line 10 to determine the total amount due and enter this on line 11.

- To calculate the overpayment, subtract the sum of lines 5 and 10 from line 8 and enter this on line 12.

- Enter the amount of overpayment you wish to apply to next year on line 13.

- Calculate the refund amount by subtracting line 13 from line 12 and enter this on line 14.

- Complete the signature section at the bottom of the form, including the signature of the general partner or member manager, title, and date. If applicable, authorize the Utah State Tax Commission (USTC) to discuss this return with the preparer by marking "X" in the designated box.

- Ensure the preparer, if applicable, signs and dates the return, and fills in their telephone number, Preparer Tax Identification Number (PTIN), EIN, and the firm's name and address.

After the form is completed, make sure to review all the information for accuracy. Attach all required schedules and documentation. Finally, submit the form to the Utah State Tax Commission by the specified deadline to ensure compliance and avoid any penalties.

Common Questions

FAQs about the Utah TC-65 Form

What is the Utah TC-65 Form?

The Utah TC-65 Form is a return document specifically for partnerships, limited liability partnerships (LLPs), and limited liability companies (LLCs) that are required to report their income, deductions, and taxes to the state of Utah. It is primarily utilized to calculate the tax responsibilities that pass through from the entity to the individual partners or members, based on the entity’s financial activities during the fiscal year.

Who needs to file the Utah TC-65 Form?

Any entity operating as a general partnership, limited partnership, limited liability partnership, or limited liability company that conducts business in Utah or receives income from Utah sources is mandated to file the TC-65 Form. This requirement applies regardless of whether the entity is formally registered in Utah or operates in multiple states.

What are the key sections of the TC-65 Form?

Entity Information: This section collects basic information about the entity including the entity type, registration date in Utah, and the fiscal period for the reported tax year.

Income and Deductions: Details of the entity’s income, deductions, and related tax information are reported here.

Apportionment Schedules: For entities operating both in and outside of Utah, these schedules help determine what portion of income is attributable to Utah operations.

Signatory Section: A certification that the information provided is accurate, signed by a representative of the entity.

What are the deadlines for filing the TC-65 Form?

The TC-65 Form is typically due on the 15th day of the fourth month following the close of the fiscal year for the reporting entity. For most businesses operating on a calendar year basis, this date falls on April 15. If the entity needs more time to file, it can request an extension, which may grant additional time to submit the form without incurring penalties for late filing.

How can amendments be made to a previously filed TC-65 Form?

If an entity discovers errors or omissions on a previously filed TC-65 Form, it can file an amended return. The form includes a box to mark indicating that it is an amended return, along with specific schedules to report the corrected information. Amended returns should provide a clear explanation of the changes and include any necessary documentation to support the amendments.

Common mistakes

Filling out the Utah TC-65 form, a crucial document for Partnerships and Limited Liability Companies (LLCs) operating in Utah, requires careful attention to detail to avoid common mistakes. These errors can delay processing, affect the financial outcomes for the business, and potentially lead to penalties. Understanding what these mistakes are can assist entities in ensuring their submissions are accurate and compliant.

- Failing to check the correct entity type at the beginning of the form can cause confusion and incorrect processing of the form. Entities must accurately identify themselves as either a General Partnership, Limited Partnership, Limited Liability Partnership, Limited Liability Company, or specify another type if those listed do not apply.

- Incorrect or incomplete reporting of the Employer Identification Number (EIN) can significantly delay processing. This number is crucial for the Utah State Tax Commission to identify the entity correctly.

- Omitting the signature of a general partner or member manager at the end of the form. This oversight can invalidate the submission as the form requires this authentication to verify the accuracy and completeness of the information provided.

- Not marking whether the return is an amended one and failing to provide necessary codes. Amended returns require careful handling, and the appropriate checkbox and codes help ensure the form is processed correctly.

- Miscalculations in the tax due sections, including pass-through withholding tax and Utah use tax totals. Accurate calculations in these areas are vital for determining the correct tax liability or refund due.

- Overlooking the requirement to report total prepayments made for the year outside of pass-through withholding tax or credits. This oversight can lead to inaccuracies in the calculation of the total payments and the determination of whether there is tax due or an overpayment.

- Forgetting to complete or inaccurately filling in the sections related to Utah taxable income, non-Utah nonbusiness income, and apportionment schedules. A careful review of Schedules A, H, and J, where applicable, is critical to correctly reporting income and deductions.

- Misunderstanding how to apply overpayments to the next year or request a refund. The choices made in these sections affect the financial planning and tax strategies of the entity.

To avoid these pitfalls, entities are encouraged to meticulously review instructions provided with the TC-65 form, double-check their calculations, and ensure that all required sections are completed fully and accurately. In cases of uncertainty, consulting with a tax professional can provide additional assurance that the form is filled out properly, thereby minimizing potential issues with the Utah State Tax Commission.

In conclusion, while the process of completing the Utah TC-65 form may seem straightforward, attention to detail is essential. By being mindful of the common errors as outlined, entities can navigate the complexities of tax filing more smoothly, ensuring compliance and maximizing their financial outcomes.

Documents used along the form

When dealing with the intricacies of filing partnership or limited liability company (LLC) returns in Utah, particularly the TC-65 form, there are several additional forms and documents that entities might need to complete the submission process effectively. This not only ensures compliance with state tax laws but can also help in maximizing potential tax benefits. Here’s a rundown of some of these essential documents.

- Schedule A - Utah Taxable Income for Pass-through Entity Taxpayers: This schedule is used to report the entity's net income (loss), adjustments, and the total taxable income for Utah. It highlights adjustments specific to Utah state tax law, like certain state-specific deductions or income exclusions, that might not appear on the federal return.

- Schedule H - Utah Nonbusiness Income Net of Expenses: Schedule H is vital for differentiating between business and nonbusiness income, ensuring that only Utah-related nonbusiness income is taxed. This form helps detail the nonbusiness income earned, related expenses, and the net nonbusiness income that should be considered for Utah state taxes.

- Schedule J - Apportionment Schedule: For businesses that operate both in and out of Utah, Schedule J is crucial. It determines the portion of total income that is attributable to Utah based on the property, payroll, and sales factors. This apportionment calculation directly impacts the amount of income subject to Utah state tax.

- Federal Form 1065, U.S. Return of Partnership Income: While technically a federal form, the 1065 is essential for entities filing the TC-65 as it provides the foundational income and deduction information needed for state-level returns. This includes the partnership’s income, gains, losses, deductions, and credits, and serves as a basis for state adjustments.

Understanding and correctly using these forms in conjunction with the TC-65 can be a challenging task, but it’s vital for ensuring that your partnership or LLC is in full compliance with Utah tax laws. It’s important to consult with a tax professional who can provide guidance specific to your business situation, helping to navigate the complexities of state tax filing. This approach not only minimizes errors but can also uncover opportunities to optimize your tax obligations.

Similar forms

The Utah TC-65 form closely resembles the IRS form 1065, U.S. Return of Partnership Income. Both are used by partnerships and other non-corporate entities to report their income, deductions, and gains or losses. The 1065 form serves as the federal counterpart to the state-focused TC-65, requiring similar information about the partnership’s financial activities over the fiscal year. Each form collects details on the entity's profit distribution among partners and ensures tax obligations are met according to the respective tax jurisdiction's laws.

The TC-20 form, otherwise known as the Utah Corporation Franchise or Income Tax Return, shares common ground with the Utah TC-65 in that both are designed for entities to report income to the Utah State Tax Commission. While the TC-20 caters specifically to corporations operating in Utah, both forms help entities calculate their tax liability based on earned income within the state. Furthermore, they both facilitate adjustments relevant to their entity types, promoting compliance with Utah tax laws.

The Schedule K-1 (Form 1065) is another document that mirrors aspects of the Utah TC-65, particularly in its role in reporting income, deductions, and credits of each partner in a partnership. Like parts of the TC-65, the Schedule K-1 ensures transparent disclosure of each partner's share of the entity’s financial activity. This setup allows partners to accurately report their share of the income on their personal tax returns, aligning with both federal and state tax reporting requirements.

The TC-20S, the Utah S Corporation Tax Return, although specifically tailored for S corporations, aligns with the Utah TC-65 in function and purpose. Both serve as state tax reporting documents that cater to specific business structures, ensuring they meet their tax obligations in Utah. Entities use these forms to detail their income, losses, and deductions, allowing for accurate tax liability calculations in accordance with Utah’s tax regulations. Despite the difference in business entity focus, each form plays a crucial role in the tax submission process for Utah-based businesses.

Lastly, the TC-65 form shares similarities with the TC-20MC, the Utah Multiple Corporation Schedule. This form is used when multiple corporations are reporting their income tax as a single group under Utah’s consolidated income tax provisions. Like the TC-65, the TC-20MC deals with complex arrangements of business entities and their tax responsibilities to the state. Both documents allow for the aggregation of financial information, albeit from different perspectives, to streamline the reporting and ensure accuracy in tax calculations and submissions.

Dos and Don'ts

When filling out the Utah TC-65 form, it's essential to do it accurately to avoid any issues with the state tax authority. Following a set of guidelines can help ensure that the process goes smoothly. Here are seven things you should and shouldn't do:

- Do:

- Make sure you have all the necessary information and documents, such as federal form 1065 and any other schedules or forms referenced, before you start filling out the form.

- Check the correct box for your entity type (e.g., general partnership, limited liability company) to accurately represent your business structure.

- Clearly report your Utah taxable income for pass-through entity taxpayers as indicated in Schedule A of the TC-65 instruction.

- Accurately calculate and enter the total pass-through withholding tax and Utah use tax on the form.

- Double-check the math for all calculated fields, such as total tax, total payments, and overpayment or amount due, to avoid errors.

- Sign and date the form. If you're the preparer, also provide your information as required.

- Remember to mark whether the return is amended and provide the correct code if applicable.

- Don't:

- Do not leave any required fields blank. If a section does not apply, enter "N/A" or "0," as appropriate, to indicate it was not overlooked.

- Avoid guessing or estimating figures. Use exact numbers from your records and supporting documentation.

- Do not use pencil or erasable ink. Fill out the form in blue or black ink to ensure that it is legible and permanent.

- Resist the urge to file the form late. Submit it by the due date to avoid penalties and interest for late filing.

- Do not forget to attach any required schedules or supporting documents that are referenced in the form.

- Avoid rounding numbers in a way that significantly deviates from the actual figures. While minor rounding to the nearest dollar is accepted, large inaccuracies can cause issues.

- Do not ignore the declaration statement at the end of the form. Your signature attests to the accuracy and completeness of the information provided.

By following these dos and don'ts, you can help ensure that your Utah TC-65 form is completed properly, which can help to avoid processing delays or inquiries from the tax authority.

Misconceptions

Understanding the Utah TC-65 form, which is integral for partnerships, limited liability partnerships, and limited liability companies reporting their income in Utah, can often lead to confusion due to common misconceptions. It is important to correct these misunderstandings to ensure accurate and compliant financial reporting. Here are five common misconceptions and their clarifications:

- The TC-65 form is only for limited liability companies (LLCs). This is not accurate. The TC-65 form is used not just by LLCs but also by general partnerships, limited partnerships, and limited liability partnerships to file their return in Utah. It covers a range of entity types, each with their specific reporting requirements.

- If you file a federal form 8886, you shouldn't mark the box on the TC-65 form. On the contrary, the TC-65 form requires entities that have filed a federal form 8886 to indicate this by marking an “X” in the provided box. This is to ensure that the Utah State Tax Commission is aware of any reportable transactions the entity has disclosed federally.

- No tax is due with the TC-65 form as it is an informational return. This misconception can lead to non-compliance. While the TC-65 form reports the income and distributes the tax responsibility to its members or partners, it may also require the payment of certain taxes directly with the return, such as pass-through withholding tax and Utah use tax.

- Amendments to the form are not possible after initial filing. Entities can indeed file an amended TC-65 return if necessary. If adjustments are required after the original filing, entities should complete the form again, marking it as an amended return and detailing the corrections. This process allows for the rectification of previously reported information.

- The preparer’s information is optional. While the partnership or LLC may complete the form themselves, if a professional preparer is used, their information—including signature, telephone number, and Preparer Tax Identification Number (PTIN)—must be included. This ensures accountability and the ability for the Utah State Tax Commission to contact the preparer if there are questions about the return.

By understanding these crucial aspects of the TC-65 form, partnerships and similar entities can better navigate their tax obligations in Utah, ensuring compliance and avoiding potential pitfalls associated with these common misconceptions.

Key takeaways

Understanding how to accurately fill out and utilize the Utah TC-65 form is crucial for partnerships, limited liability partnerships, and limited liability companies within the state. Here are five key takeaways for these entities when dealing with the TC-65 form:

- The TC-65 form is explicitly designed for partnerships and limited liability entities in Utah to file their annual returns. These organizations should ensure they're using the correct form for their entity type to comply with state filing requirements.

- Entities must indicate the filing year at the top of the form, specifying whether it is for the calendar year 2020 or a fiscal year. The precise beginning and ending dates of the fiscal year should be clearly noted.

- If filing an amended return, entities must mark the appropriate box and include the amendment code. This is critical for the Utah State Tax Commission to distinguish the submission from the original return and process it correctly.

- The form requires detailed financial information, including the total tax, which combines pass-through withholding tax and Utah use tax, as well as total payments made throughout the year. It's essential for entities to calculate these figures accurately to avoid discrepancies.

- Finally, the signature of a general partner or member manager is mandatory, certifying under penalties of perjury that the information provided is true, correct, and complete. It’s imperative for authorized individuals to review all entries on the form meticulously before signing to affirm the return’s accuracy.

By adhering to these key points, partnerships, and limited liability entities in Utah can navigate the complexities of the TC-65 form more efficiently, ensuring compliance with state tax obligations and minimizing the risk of errors in their filings.

Common PDF Templates

Rental Agreement Utah - Includes owner disclosures about current utility service termination notices or existing uncorrected building or health code violations, keeping tenants informed.

Dws-esd 631 - Enables precise reporting of wage information to the Utah Department of Workforce Services, facilitating accurate unemployment benefit determinations.

Utah State Tax Form for Employees - The document emphasizes the need for corporate accountability and up-to-date tax affairs in maintaining good standing.