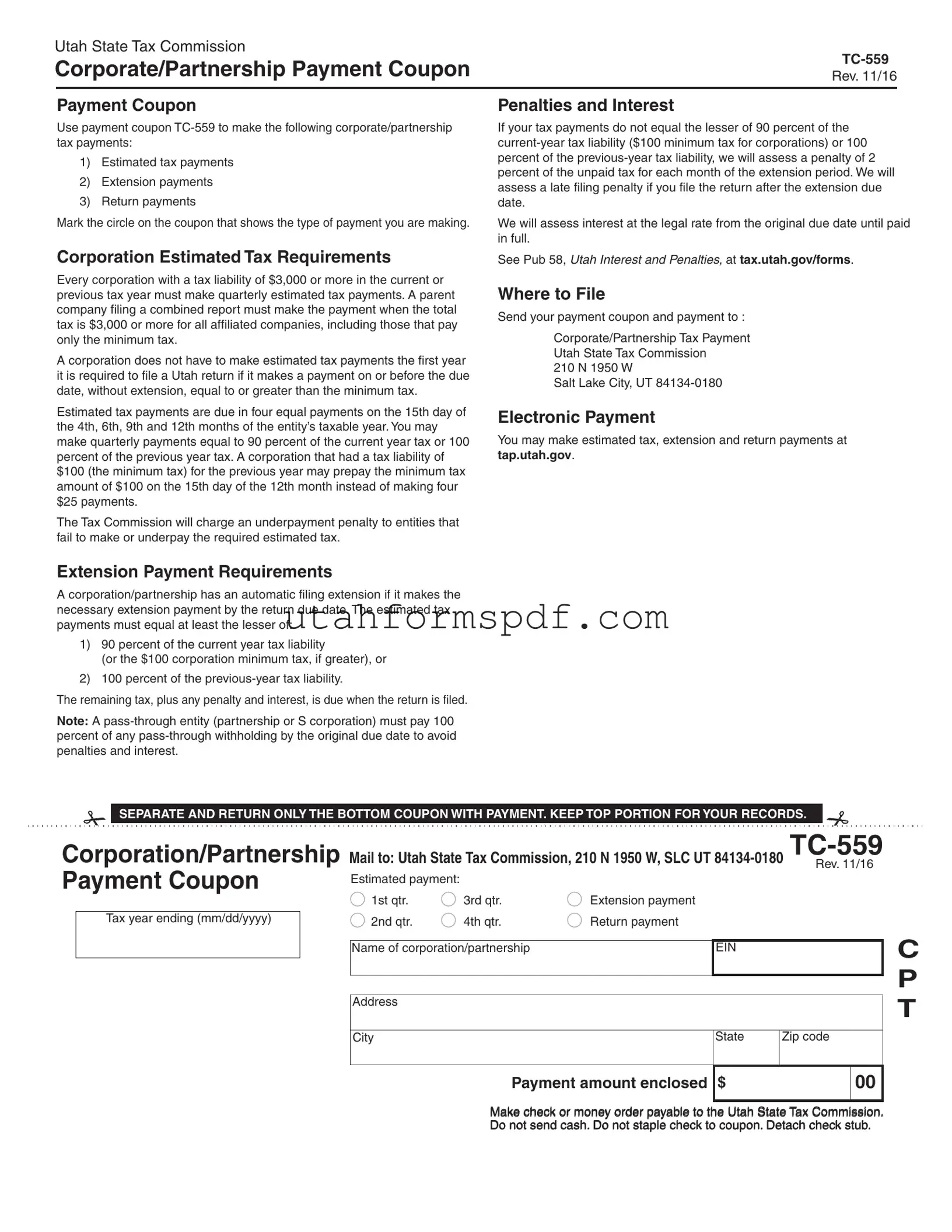

Blank Utah Tc 559 Form

The Utah TC-559 form plays a pivotal role in how corporations and partnerships manage their state tax obligations, offering a streamlined method for these entities to make various tax payments to the Utah State Tax Commission. Designed to accommodate estimated tax payments, extension payments, and return payments, the form simplifies the tax payment process by allowing businesses to indicate the purpose of their payment clearly. It's critical for corporations to meet specific tax payment thresholds to avoid penalties, with the form outlining that payments must at least equal the lesser of 90 percent of the current year's tax liability or 100 percent of the previous year's liability, highlighting the seriousness of accurate on-time payments to avoid additional charges. For corporations, estimated tax requirements come into play if their tax liability is $3,000 or more, necessitating quarterly payments that, if not met, can lead to underpayment penalties. Furthermore, this form is instrumental for businesses in making extension payments to receive an automatic filing extension, underlining its significance in tax planning and management strategies. The mention of a separate section for pass-through entities highlights the form's inclusion of various business structures in its tax payment processes. Evidently, the TC-559 form not only serves as a means to fulfill tax obligations but also as a crucial document for maintaining compliance and avoiding financial penalties, illustrating its integral role in the financial operations of corporations and partnerships within Utah.

Form Preview Example

Utah State Tax Commission

Corporate/Partnership Payment Coupon |

|

Rev. 11/16 |

|

|

|

Payment Coupon |

Penalties and Interest |

Use payment coupon

1)Estimated tax payments

2)Extension payments

3)Return payments

Mark the circle on the coupon that shows the type of payment you are making.

If your tax payments do not equal the lesser of 90 percent of the

We will assess interest at the legal rate from the original due date until paid in full.

Corporation Estimated Tax Requirements

Every corporation with a tax liability of $3,000 or more in the current or previous tax year must make quarterly estimated tax payments. A parent company filing a combined report must make the payment when the total tax is $3,000 or more for all affiliated companies, including those that pay only the minimum tax.

A corporation does not have to make estimated tax payments the first year it is required to file a Utah return if it makes a payment on or before the due date, without extension, equal to or greater than the minimum tax.

Estimated tax payments are due in four equal payments on the 15th day of the 4th, 6th, 9th and 12th months of the entity’s taxable year. You may make quarterly payments equal to 90 percent of the current year tax or 100 percent of the previous year tax. A corporation that had a tax liability of $100 (the minimum tax) for the previous year may prepay the minimum tax amount of $100 on the 15th day of the 12th month instead of making four $25 payments.

The Tax Commission will charge an underpayment penalty to entities that fail to make or underpay the required estimated tax.

Extension Payment Requirements

A corporation/partnership has an automatic filing extension if it makes the necessary extension payment by the return due date. The estimated tax payments must equal at least the lesser of:

1)90 percent of the current year tax liability

(or the $100 corporation minimum tax, if greater), or

2)100 percent of the

The remaining tax, plus any penalty and interest, is due when the return is filed.

Note: A

See Pub 58, UTAH INTEREST AND PENALTIES, at tax.utah.gov/forms.

Where to File

Send your payment coupon and payment to :

Corporate/Partnership Tax Payment

Utah State Tax Commission

210 N 1950 W

Salt Lake City, UT

Electronic Payment

You may make estimated tax, extension and return payments at tap.utah.gov.

SEPARATE AND RETURN ONLY THE BOTTOM COUPON WITH PAYMENT. KEEP TOP PORTION FOR YOUR RECORDS.

Corporation/Partnership Mail to: Utah State Tax Commission, 210 N 1950 W, SLC UT |

||||||||

Rev. 11/16 |

||||||||

Payment Coupon |

|

Estimated payment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1st qtr. |

3rd qtr. |

Extension payment |

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax year ending (mm/dd/yyyy) |

|

2nd qtr. |

4th qtr. |

Return payment |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

Name of corporation/partnership |

|

EIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

State |

Zip code |

|

|

|

|

|

|

|

|

|

|

C P T

Payment amount enclosed

$

00

Make check or money order payable to the Utah State Tax Commission. Do not send cash. Do not staple check to coupon. Detach check stub.

Form Breakdown

| Fact Number | Fact Description |

|---|---|

| 1 | The Utah TC-559 form is used for corporate/partnership tax payments. |

| 2 | It facilitates several types of payments: estimated tax payments, extension payments, and return payments. |

| 3 | Payers must mark the specific type of payment they are making on the coupon. |

| 4 | A penalty is assessed if tax payments are less than 90% of the current year's liability or 100% of the previous year's, with a minimum $100 tax for corporations. |

| 5 | Corporations with a tax liability of $3,000 or more must make quarterly estimated tax payments. |

| 6 | Estimated tax payments are due in four equal parts on specific dates throughout the entity's taxable year. |

| 7 | An underpayment penalty is charged for failing to make the necessary estimated payments. |

| 8 | Corporations/partnerships can receive an automatic filing extension by making the necessary payment by the due date. |

| 9 | Payments can be made electronically via tap.utah.gov. |

| 10 | The mailing address for the payment coupon is: Corporate/Partnership Tax Payment Utah State Tax Commission, 210 N 1950 W, Salt Lake City, UT 84134-0180. |

Detailed Steps for Writing Utah Tc 559

Filling out the Utah TC-559 form is a step that ensures your business complies with its tax obligations accurately and timely. This process involves specifying the nature of the payment you are making, whether it is an estimated tax payment, an extension payment, or a return payment. Accuracy in completing this form helps in avoiding unnecessary penalties and interest due to underpayment or late payment of taxes. Here is a detailed guide on how to complete the form:

- First, identify the type of tax payment you are making: estimated tax payment, extension payment, or return payment. Mark the appropriate circle on the coupon to indicate your choice.

- If the payment is an estimated tax payment, select the specific quarter for which you are making the payment: 1st quarter, 2nd quarter, 3rd quarter, or 4th quarter.

- Fill in the "Tax year ending" box by entering the end date of the tax year for your corporation or partnership in the format mm/dd/yyyy.

- Enter the full name of your corporation or partnership in the space provided.

- Provide the Employer Identification Number (EIN) of your corporation or partnership.

- Write down the full address of your entity, including the city, state, and zip code.

- Indicate your point of contact by marking either "C" for corporation or "P" for partnership in the designated box.

- In the "Payment amount enclosed" box, write down the total amount of the payment you are submitting.

- Prepare a check or money order payable to the Utah State Tax Commission for the total payment amount. Remember, sending cash is not advisable, and you should not staple your check to the coupon.

- Detach the payment coupon from the top portion, which you should keep for your records, and mail it along with your payment to the Utah State Tax Commission at the address provided: 210 N 1950 W, Salt Lake City, UT 84134-0180.

Once you have submitted the payment along with the correctly filled-out TC-559 form, your next steps depend on the nature of your payment. For estimated payments, ensure you prepare for the next quarterly payment to maintain compliance. If you've submitted an extension or return payment, monitor any communications from the Utah State Tax Commission for confirmation or further instructions. Remember, timely and accurate payments help avoid penalties and ensure smooth operations for your business.

Common Questions

- What is the Utah TC-559 form used for?

- How do penalties and interest apply to payments made using the TC-559 form?

- Who must make estimated tax payments, and what are the requirements?

- What are the extension payment requirements for a corporation or partnership?

- How can penalties and interest be avoided for pass-through entities?

- Where should the TC-559 payment coupon be sent?

- Is there an option to make these payments electronically?

- What should be done with the top portion of the TC-559 form?

- How should payments be made when using the TC-559 form?

- Are there any specific formatting requirements for the check associated with the TC-559 form?

The Utah TC-559 form is a payment coupon designed for making specific tax payments related to corporations and partnerships. These payments include estimated tax payments, extension payments, and return payments. The form allows you to specify the type of payment you are making by marking the appropriate circle on the coupon.

If tax payments made are less than 90 percent of the current year’s tax liability or less than 100 percent of the previous year's liability, a penalty of 2 percent of the unpaid tax for each month of the extension period is assessed. Additionally, late filing penalties are imposed for returns filed after the extension due date. Interest is also charged at the legal rate from the original due date until the tax is paid in full.

Every corporation that has a tax liability of $3,000 or more in the current or previous tax year must make quarterly estimated tax payments. This also applies to parent companies filing a combined report for all affiliated companies. Payments are due in four equal parts on specific dates throughout the entity’s taxable year. Corporations can choose to make these payments based on 90 percent of the current year’s tax liability or 100 percent of the previous year's liability. For corporations with a minimal tax liability of $100 the previous year, a singular payment of $100 can be made by the 15th day of the 12th month instead of quarterly payments.

A corporation or partnership can obtain an automatic filing extension by making the necessary extension payment by the return’s due date. The payment must be at least the lesser of 90 percent of the current year’s tax liability or 100 percent of the prior year's liability. Any remaining tax, along with potential penalties and interest, is due when the return is filed.

Pass-through entities, like partnerships or S corporations, must pay 100 percent of any pass-through withholding by the original due date to avoid penalties and interest.

Payments and the TC-559 payment coupon should be sent to the Corporate/Partnership Tax Payment address at the Utah State Tax Commission, located at 210 N 1950 W, Salt Lake City, UT 84134-0180.

Yes, estimated tax payments, extension payments, and return payments can all be made electronically via the Taxpayer Access Point (TAP) at tap.utah.gov.

The top portion of the TC-559 form should be kept for your records, while only the bottom coupon part should be detached and returned with payment.

Payments should be made by check or money order payable to the Utah State Tax Commission. It's important not to send cash and to avoid stapling the check to the coupon.

Yes, when submitting a check with the TC-559 form, ensure that the check is made out correctly to the Utah State Tax Conmission and that you do not staple the check to the coupon. Also, remember to detach the check stub before mailing.

Common mistakes

Filling out tax forms can be complex and is often a source of mistakes that could be costly. The Utah TC-559 form, used for making corporate and partnership tax payments, is no exception. Understanding the common errors can help filers avoid unnecessary complications.

One common mistake is not selecting the correct type of payment. The form requires the filer to mark specifically if the payment is an estimated tax, an extension, or a return payment. Overlooking or wrongly marking this section can lead to misinterpretation by the Utah State Tax Commission, potentially causing issues with your tax account.

A significant and equally common error involves miscalculating the tax payments. The penalties for underpayment are explicit: a 2 percent penalty per month on the unpaid tax during the extension period. Taxpayers must ensure that their payments either meet or exceed the lesser of 90 percent of the current year's tax liability or 100 percent of the previous year's liability to avoid these penalties.

Thirdly, many forget the importance of the due dates for quarterly estimated tax payments. Corporations with a liability of $3,000 or more are required to make these payments, and missing these deadlines can result in penalties. Ensuring payments are made by the 15th day of the 4th, 6th, 9th, and 12th months of the taxable year is crucial for compliance.

Another common mistake is not making the necessary extension payment by the due date, which can automatically lead to an extension. The lack of understanding around this requirement can lead to unexpected late filing penalties, adding to the tax burden for corporations.

Many filers also overlook the electronic payment option available at tap.utah.gov. By ignoring this convenient and secure payment method, they miss out on a streamlined filing process that could save time and reduce the risk of mailing errors or delays.

- Not marking the correct payment type on the form.

- Miscalculating the payment amount, leading to underpayment penalties.

- Missing the quarterly estimated tax payment deadlines.

- Failing to make the necessary extension payment on time.

- Overlooking the availability of making payments electronically.

Finally, an often overlooked detail is ensuring that the check or money order is made payable to the Utah State Tax Commission and is not stapled to the coupon. This might seem minor, but ensuring the check is correctly prepared and submitted can prevent processing delays or issues.

By being mindful of these common pitfalls, filers can ensure a smoother and more efficient tax payment process, avoiding unnecessary fees and complications with the Utah State Tax Commission.

Documents used along the form

When handling tax matters for a corporation or partnership in Utah, particularly with the Utah Tc 559 form, it's important to have all necessary documents and forms ready to ensure compliance and accurate reporting. Among these, there are several significant forms and documents that you might need to use alongside the TC-559.

- TC-20: The Corporation Franchise or Income Tax Return form is essential for reporting your corporation’s income, gains, losses, deductions, credits, and to calculate the entity's income tax liability.

- TC-20S: This form is specifically for S Corporations operating in Utah. It's used to file their state income tax return, similar to the TC-20 form but tailored for the unique status of S Corporations.

- TC-65: The Partnership Return of Income form is necessary for partnerships to report income, losses, deductions, and credits to the State of Utah, aligning with federal reports but adhering to state-specific adjustments.

- Pub 58: UTAODYAHADING N.JUSTRIcest and Penaltyaxesormation is crucial for understanding the implications of late or underpaid taxes, detailing the interest rates, penalty assessments, and guidelines for avoiding common financial pitfalls related to tax payments and filings.

- Form TC-40: Utah Individual Income Tax Return is not directly related to corporate or partnership taxes but may be necessary for individual members of a partnership or S Corporation to include specific income aspects from the entity on their personal state tax returns.

These documents complement the TC-559 form allowing for a comprehensive approach to managing tax responsibilities in Utah. By being familiar with and utilizing these forms, corporations and partnerships can more effectively navigate the complexities of state tax compliance, potentially avoiding penalties and optimizing tax obligations.

Similar forms

The IRS Form 1040-ES, "Estimated Tax for Individuals," is similar to the Utah TC-559 form as it is used for making estimated tax payments. Like the TC-559, taxpayers use the 1040-ES to pay taxes on income that is not subject to withholding. This includes earnings from self-employment, interest, dividends, and rent. Both forms allow taxpayers to avoid underpayment penalties by calculating and paying estimated taxes quarterly. The significant similarity lies in the structure of these payments, designed to help taxpayers manage their tax liabilities throughout the year.

The IRS Form 7004, "Application for Automatic Extension of Time To File Certain Business Income Tax, Information, and Other Returns," parallels the extension payment feature of the Utah TC-559 form. Form 7004 is used by corporations, partnerships, and certain other entities to request an extension of time to file their tax returns. Similarly, the TC-559 form includes a section for extension payments, implying that by making a payment, the entity automatically qualifies for an extension to file their return without facing late-filing penalties.

Form 4868, "Application for Automatic Extension of Time to File U.S. Individual Income Tax Return," is another document related to the extension payment aspect of the TC-559. While Form 4868 serves individuals seeking an extension to file their income tax returns, the TC-559 caters to corporate and partnership entities. Both forms emphasize the necessity of making an appropriate payment toward the entity’s or individual’s estimated tax liability to secure the extension, thus avoiding penalties for late filing.

The IRS Form 1120-W, "Estimated Tax for Corporations," is closely related to the estimated tax payments portion of the Utah TC-559 form. Form 1120-W is designed for corporations to calculate and pay their estimated tax on a quarterly basis. This form is essential for corporations to comply with the IRS requirement to pay taxes as income is earned or received throughout the year. Both the 1120-W and the TC-559 assist corporations in determining the amount of estimated tax they should pay to avoid underpayment penalties.

The Schedule K-1 (Form 1065), "Partner's Share of Income, Deductions, Credits, etc.," is similar to sections of the TC-559 that deal with partnership tax obligations. While the Schedule K-1 is more about reporting each partner's share of the partnership's earnings and losses, it indirectly relates to making appropriate payments for those earnings. Partnerships, through using the TC-559, ensure they meet tax payment obligations on behalf of their partners, similar to how individual partners use K-1 information to meet their tax liabilities.

The IRS Form 8804, "Annual Return for Partnership Withholding Tax (Section 1446)," bears resemblance to the TC-559 form in the context of partnerships making payments. Form 8804 is used to report and pay withholding tax on income effectively connected to the United States that is allocable to foreign partners. The TC-559's functionality allows partnerships to handle their tax payment obligations, including estimated taxes and extension payments, showcasing the parallels in facilitating tax payments for partnerships.

Form 941, "Employer's Quarterly Federal Tax Return," while primarily for reporting payroll taxes, shares a quarterly payment structure with the Utah TC-559 form's estimated tax payment option. Businesses use Form 941 to report income taxes, Social Security tax, or Medicare tax withheld from employees' paychecks and pay the employer's portion of Social Security or Medicare tax. The similarity with the TC-659 lies in the periodic payment obligation, underscoring the importance of regular tax payments to avoid penalties and interest.

Dos and Don'ts

When preparing to fill out the Utah TC-559 form, a careful approach is required to ensure accurate and timely tax payments are made for corporations and partnerships. Below are a series of dos and don’ts that can serve as a guideline during this process.

Do:- Review the entire form before starting: Ensure you understand each section to provide accurate information.

- Mark the correct circle: Indicate the type of payment you are making, whether it is for estimated tax, extension, or return payments.

- Use the correct Tax Year Ending (TYE) date: Fill in the TYE date in the format mm/dd/yyyy to avoid any misunderstandings.

- Include the correct payment amount: Verify the amount against your tax calculations to ensure you're paying the right amount.

- Keep the top portion for your records: After detaching the bottom coupon for submission, retain the top portion for future reference or in case of queries from the Tax Commission.

- Wait until the last minute: Procrastination can lead to rushed errors or missing the due date, resulting in penalties and interest charges.

- Send cash: For security reasons and to ensure there's a record of your payment, avoid sending cash. Instead, use a check or money order payable to the Utah State Tax Commission.

By following these guidelines, filers can navigate the process more smoothly and help ensure their tax obligations are met accurately and on time. It's also recommended to consult with a tax professional or refer to the Tax Commission's resources for any specific questions regarding your situation.

Misconceptions

Understanding the Utah TC-559 form is crucial for corporations and partnerships when it comes to tax payments. However, there are common misconceptions about this form. Let's address some of them:

Misconception 1: The TC-559 form is only for corporations. While it's true that corporations use this form, it's also for partnerships. The form serves both entities for making estimated tax payments, extension payments, and return payments.

Misconception 2: You can't use the TC-559 for different types of payments. Actually, the TC-559 form is quite versatile. Taxpayers can indicate on the form whether they are making an estimated tax payment, an extension payment, or a return payment, by marking the appropriate circle on the coupon.

Misconception 3: If you pay late, interest is the only consequence. Late payments not only accrue interest at the legal rate from the original due date until paid in full but also incur a late filing penalty if the return is filed after the extension due date.

Misconception 4: Only annual payments are allowed. Corporations with a tax liability of $3,000 or more must make quarterly estimated tax payments. This requirement ensures entities spread their tax liability throughout the year, making payments more manageable.

Misconception 5: First-year corporations must make estimated tax payments immediately. Corporations do not have to make estimated tax payments in their first tax year as long as they make a payment on or before the due date, without an extension, that is either equal to or greater than the minimum tax.

Misconception 6: Overpayment penalties are automatic. The Tax Commission charges an underpayment penalty for entities that fail to make, or underpay, the required estimated tax. However, penalties are not applied for overpayment or timely payment.

Misconception 7: Extensions for filing automatically extend the payment due date. While an extension may give more time to file, the estimated tax payments must still be made timely. An automatic extension requires necessary extension payments by the return due date to avoid penalties and interest.

Misconception 8: Electronic payments are not allowed. Taxpayers have the option to make their payments electronically via the Utah Taxpayer Access Point (TAP) website, providing a convenient alternative to mailing payments.

Misconception 9: The TC-559 form should always be attached to the check. The instructions clearly request taxpayers not to staple the check to the coupon, ensuring that the payment process is handled efficiently and securely by the Tax Commission.

Overall, it's important for corporations and partnerships to fully understand the correct use of the Utah TC-559 form and its requirements to avoid penalties and ensure compliance with Utah's tax laws.

Key takeaways

The Utah TC-559 form serves as a vital tool for corporations and partnerships to ensure compliance with tax payment requirements in Utah. Understanding its correct use is crucial for avoiding penalties and interest charges.

- Identification of Payment Type: Taxpayers must clearly mark the intended payment type on the TC-559 coupon, choosing from estimated tax payments, extension payments, or return payments. This ensures that the payment is applied correctly by the Utah State Tax Commission.

- Meeting Tax Payment Thresholds: Corporations and partnerships are required to pay at least 90% of their current year's tax liability or 100% of the previous year's liability to avoid penalties. For corporations, a minimum tax of $100 is applicable if it exceeds 90% of the current year's liability.

- Penalties and Interest for Underpayment: If tax payments fall short of the required threshold, the commission imposes a 2% penalty for each month of the extension period on the unpaid tax amount. Additionally, interest accumulates at the legal rate from the due date until the tax is paid in full.

- Quarterly Estimated Tax Payments: Corporations with tax liabilities of $3,000 or more must make quarterly payments. These payments are due on the 15th day of the 4th, 6th, 9th, and 12th months of the fiscal year, with options to pay based on the current or previous year's tax liability.

- Automatic Extension Through Estimated Tax Payment: An automatic filing extension is granted to corporations and partnerships that make necessary extension payments by the due date. The extension payment must meet specified requirements based on tax liability assessments.

- Methods of Payment: Tax payments can be made by sending the completed TC-559 coupon with payment to the mentioned address or through electronic payment options available on the Utah Tax Commission's website. It's important to follow instructions carefully, such as not stapling checks to the coupon, to ensure proper processing.

Accurate and timely completion and submission of the Utah TC-559 form is essential for corporations and partnerships to fulfill their tax obligations and avoid unnecessary penalties and interest. Taxpayers should always keep the upper portion of the form for their records and review the latest tax information and guidelines provided by the Utah State Tax Commission.

Common PDF Templates

Tc 661 Utah - Designed to facilitate a straightforward process for verifying the legitimacy of a vehicle's identification number.

Utah Driver's Permit - Choose to register or preregister to vote, contributing to civic engagement and community participation.

Utah Tax Forms - Applicants must sign the TC-142 form, verifying their role as owner, partner, or corporate officer of the business.