Blank Utah Tc 51 Form

Understanding the intricacies of the Utah TC-51 form is crucial for businesses operating within the state or those planning to start business activities in Utah. As a document issued by the Utah State Tax Commission, the TC-51 form, also known as the Nexus Questionnaire, plays a pivotal role in determining a company's tax obligations to the state. It encompasses a comprehensive range of questions designed to ascertain whether a business has a sufficient physical presence or nexus in Utah, thereby requiring it to comply with state tax laws. This form asks for detailed information about the business, including the exact business name, principal office address, federal ID number, and contact information. It inquires about the type of business, the nature of business activities, and detailed descriptions of the property and/or services sold. Additionally, the TC-51 form delves into the company's sales within Utah, the number of transactions with Utah customers, and total sales to all customers over the last three years. The questionnaire also explores various dimensions of business operations that might establish a tax nexus in Utah, such as the sale of tangible personal property, maintenance of offices or warehouses, employee activities, and leasing or renting of property within the state. It even touches upon compliance with the Streamlined Sales Tax Agreement for voluntary sellers. By accurately completing and submitting this form, businesses can ensure they meet their tax obligations and avoid potential penalties, making it an indispensable step for any company engaged in business activities in Utah.

Form Preview Example

Utah State Tax Commission

210 N 1950 W • SLC, UT 84134 • tax.utah.gov

Nexus Questionnaire

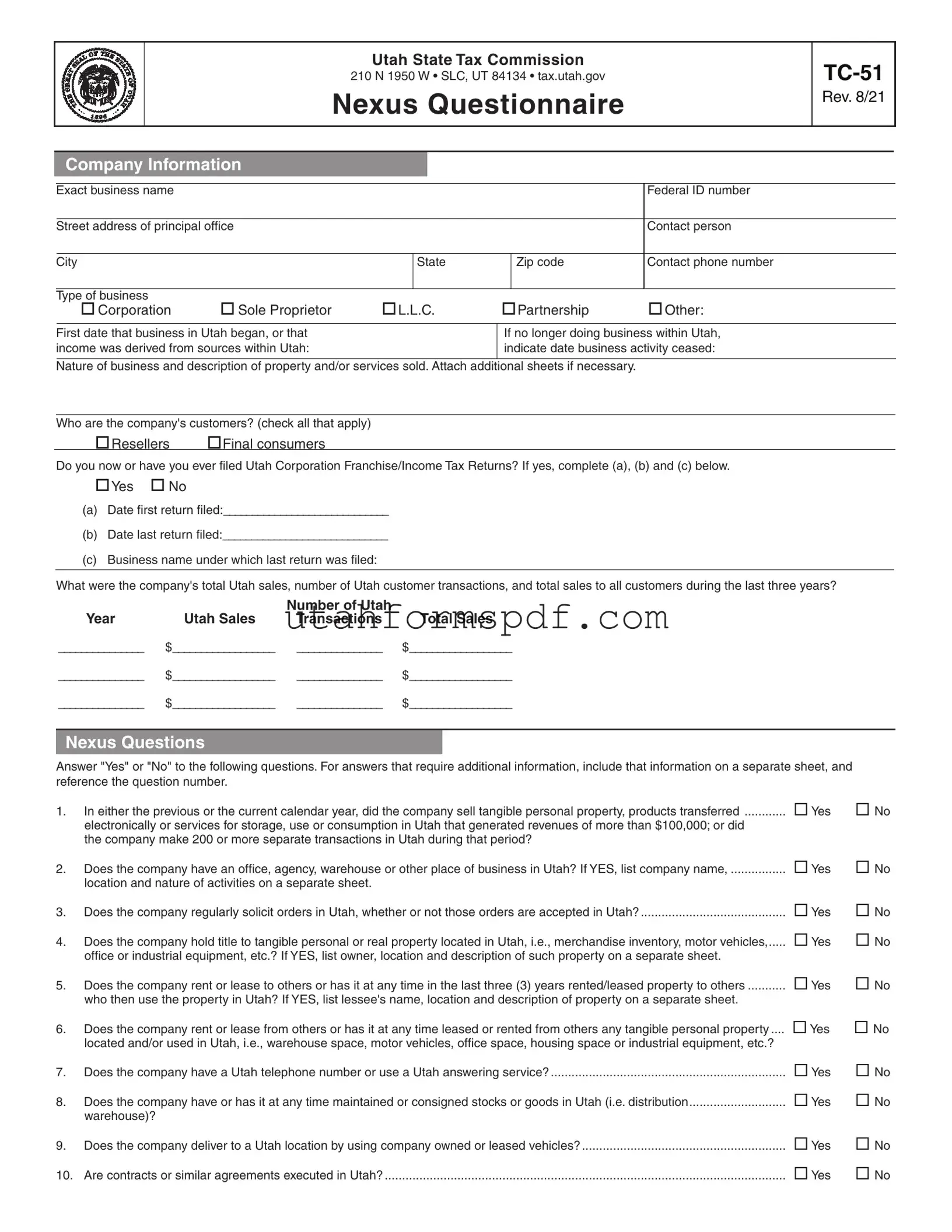

Company Information

Rev. 8/21

Exact business name

Street address of principal office

Federal ID number

Contact person

City

State

Zip code

Contact phone number

Type of business |

|

|

|

|

Corporation |

Sole Proprietor |

L.L.C. |

Partnership |

Other: |

First date that business in Utah began, or that income was derived from sources within Utah:

If no longer doing business within Utah, indicate date business activity ceased:

Nature of business and description of property and/or services sold. Attach additional sheets if necessary.

Who are the company's customers? (check all that apply)

Resellers Final consumers

Do you now or have you ever filed Utah Corporation Franchise/Income Tax Returns? If yes, complete (a), (b) and (c) below.

Yes No

(a)Date first return filed:_____________________________

(b)Date last return filed:_____________________________

(c)Business name under which last return was filed:

What were the company's total Utah sales, number of Utah customer transactions, and total sales to all customers during the last three years?

|

|

Number of Utah |

|

Year |

Utah Sales |

Transactions |

Total Sales |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

Nexus Questions

Answer "Yes" or "No" to the following questions. For answers that require additional information, include that information on a separate sheet, and reference the question number.

1. |

In either the previous or the current calendar year, did the company sell tangible personal property, products transferred |

Yes |

No |

|

electronically or services for storage, use or consumption in Utah that generated revenues of more than $100,000; or did |

|

|

|

the company make 200 or more separate transactions in Utah during that period? |

|

|

2. |

Does the company have an office, agency, warehouse or other place of business in Utah? If YES, list company name, ................ Yes |

No |

|

|

location and nature of activities on a separate sheet. |

|

|

3. |

Does the company regularly solicit orders in Utah, whether or not those orders are accepted in Utah? |

Yes |

No |

4. |

Does the company hold title to tangible personal or real property located in Utah, i.e., merchandise inventory, motor vehicles,..... Yes |

No |

|

|

office or industrial equipment, etc.? If YES, list owner, location and description of such property on a separate sheet. |

|

|

5. |

Does the company rent or lease to others or has it at any time in the last three (3) years rented/leased property to others |

Yes |

No |

|

who then use the property in Utah? If YES, list lessee's name, location and description of property on a separate sheet. |

|

|

6. |

Does the company rent or lease from others or has it at any time leased or rented from others any tangible personal property .... |

Yes |

No |

|

located and/or used in Utah, i.e., warehouse space, motor vehicles, office space, housing space or industrial equipment, etc.? |

|

|

7. |

Does the company have a Utah telephone number or use a Utah answering service? |

Yes |

No |

8. |

Does the company have or has it at any time maintained or consigned stocks or goods in Utah (i.e. distribution |

Yes |

No |

|

warehouse)? |

|

|

9. |

Does the company deliver to a Utah location by using company owned or leased vehicles? |

Yes |

No |

10. |

Are contracts or similar agreements executed in Utah? |

Yes |

No |

|

Yes |

No |

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

17.List names and addresses of employees or representatives, the territory they cover, and designate whether they are employees or independent contractors. Use additional sheets if necessary.

18. Do any of the sales agents in Utah represent your corporation only? |

Yes |

No |

Other Information

19. List the company's three (3) major Utah customers:

20. Are there other types of activities in Utah? Please explain:

SST Voluntary Seller

You are a voluntary seller in Utah under the Streamlined Sales Tax Agreement (see Article IV of SSUTA) if you have met ALL of the following conditions for at least 12 MONTHS PRIOR to registering with Utah:

1.You have had no fixed place of business in Utah for more than 30 days.

2.Less than $50,000 of your property* in located in Utah.

3.Less than $50,000 of your payroll occurs in Utah.

4.Less than 25 percent of your total property* or total payroll*are in Utah.

5.You do not collect sales or use tax in Utah as a condition for you or an affiliate to qualify as a supplier of goods or services to Utah.

6.You are not required to register and collect sales or use tax in Utah as a statutory requirement for yourself or an affiliate to be able to sell, ship or deliver a particular type of product into Utah.

*As defined in the contract between Streamlined Sales Tax Governing Board, Inc and the contractor.

21. Based on the criteria above, are you a voluntary Streamlined Sales Tax seller? |

Yes |

No |

Signatures

Under penalties of perjury, I declare that the information furnished in this questionnaire is, to the best of my knowledge and belief, true, correct and complete. If prepared by a person other than an officer of this corporation, this declaration is based on all information of which you have knowledge.

Name of officer

Title of officer

Signature of officer

Date

Officer's mailing address

City

State

Zip code

Officer's phone number

Name of preparer

Signature of preparer

Date

Preparer's mailing address

City

State

Zip code

Preparer's phone number

Form Breakdown

| Fact | Detail |

|---|---|

| Form Title | Utah State Tax Commission Nexus Questionnaire |

| Form Number | TC-51 |

| Revision Date | August 2021 |

| Purpose | To determine a company's nexus with Utah for tax purposes |

| Sections Included | Company Information, Nexus Questions, Employee and Contract Agent Information, Other Information |

| Governing Law | Utah State Tax Laws | >

| Submission Requirement | Must be completed by companies to assess their Utah tax obligations |

| Key Information Needed | Business name, principal office address, type of business, nature of business, sales information, activities conducted in Utah |

| Nexus Determination Criteria | Sales threshold, number of transactions, physical presence, employee activities within Utah |

| Voluntary Streamlined Sales Tax Seller Criteria | Criteria include not having a fixed place of business, specific property and payroll amounts, and certain activity thresholds within Utah |

Detailed Steps for Writing Utah Tc 51

Filling out the Utah TC-51 form is an important step towards ensuring compliance with the state's tax laws. This form is designed to gather detailed information about a company's activities within Utah to determine its tax obligations. The process is straightforward, but attention to detail is crucial to provide accurate and complete information. The following steps are designed to guide you through the process of filling out the form without hassle.

- Begin with the Company Information section. Fill in your exact business name, the street address of your principal office, your Federal ID number, and the contact information for a person the Utah State Tax Commission can reach out to if they have any questions.

- Select your type of business by checking the appropriate box: Corporation, Sole Proprietor, L.L.C., Partnership, or Other.

- Enter the first date your business began in Utah or derived income from sources within Utah. If your business has ceased operations in Utah, provide the date when business activity stopped.

- In the space provided, describe the nature of your business and the types of property and/or services sold. If you need more space, attach additional sheets and clearly indicate they are a continuation.

- Identify who your customers are by checking either "Resellers" or "Final consumers."

- If you have filed Utah Corporation Franchise/Income Tax Returns, check "Yes" and provide the date of the first return filed, date of the last return filed, and the business name under which the last return was filed.

- List your company's total sales in Utah, the number of Utah customer transactions, and total sales to all customers for the last three years.

- Answer Nexus Questions. Respond "Yes" or "No" to each question. For those requiring additional information, provide the details on a separate sheet, making sure to reference the question number.

- For questions regarding activities, use, or leasing of property in Utah, answer accordingly and give detailed information on a separate sheet if you answered "Yes." This includes information about any office, warehouse, solicitation activities, owned or leased property, etc.

- If applicable, list names and addresses of employees or representatives working in Utah, specify the territory they cover, and designate whether they are employees or independent contractors. Use additional sheets if necessary.

- Indicate if any of the sales agents represent only your corporation in Utah by marking "Yes" or "No."

- Provide the names of the company's three major Utah customers.

- Describe other types of activities your company might be engaged in within Utah.

- Determine if you are a voluntary seller under the Streamlined Sales Tax Agreement by answering "Yes" or "No" based on the listed criteria.

- Review the declaration carefully. The named officer of the corporation should sign and date the form, providing their title, mailing address, and phone number. If the form is prepared by another person, their name, signature, date, mailing address, and phone number should also be included.

After completing the form, double-check for accuracy and completeness before submission. This ensures your company's tax obligations in Utah are assessed correctly and helps avoid potential issues with the state tax commission.

Common Questions

FAQs about the Utah TC-51 Form

- What is the Utah TC-51 form used for?

The Utah TC-51 form, also known as the Nexus Questionnaire, is used by the Utah State Tax Commission to determine if a company has a "nexus" or sufficient physical presence in Utah. This determination affects whether the company must collect and remit sales tax for transactions within the state.

- Who needs to fill out a TC-51 form?

Any business that conducts operations within Utah, sells products or services in Utah, or engages in activities that might establish a taxable presence in the state should complete the TC-51 form. This includes both in-state and out-of-state businesses.

- What information do I need to provide on the TC-51 form?

Businesses must provide comprehensive information including the business name, contact details, Federal ID number, type of business, nature of business activities in Utah, and detailed answers to specific nexus questions to assess their connection to the state.

- What does "nexus" mean in the context of this form?

In the context of the TC-51 form, "nexus" refers to the business's connection or presence within Utah that obligates it to collect and remit sales tax. This can be due to physical locations, employees, or business conducted within the state.

- How do I know if I have nexus in Utah?

If your business meets any of the conditions listed in the Nexus Questions section of the form, such as making more than $100,000 in sales or engaging in more than 200 transactions in Utah within a year, you likely have a nexus. The form details various activities that establish nexus.

- What happens after I submit the TC-51 form?

After submission, the Utah State Tax Commission will review your responses and inform you whether your business has a nexus in Utah and the consequent tax obligations, including registration and collection of sales tax.

- Can I be considered a voluntary seller under the Streamlined Sales Tax Agreement in Utah?

Yes, if your business meets certain criteria outlined in the form, such as having no fixed place of business in Utah for more than 30 days and engaging in limited sales and payroll activities in the state, you might qualify as a voluntary seller under the Streamlined Sales Tax Agreement.

- Where do I submit the completed TC-51 form?

The completed TC-51 form should be sent to the Utah State Tax Commission at the address provided on the form. Ensure all required signatures and attachments are included with your submission.

Common mistakes

Filling out forms for state tax purposes can often be a tricky and detailed process. The Utah TC-51 form, used for updating the Utah State Tax Commission about a business's nexus within the state, is no exception. Here are five common mistakes people make when completing this document:

- Incorrect or Incomplete Business Information: One of the most critical sections of the Utah TC-51 form involves providing accurate company information. This includes the exact business name, the principal office address, and the Federal ID number. A common mistake is providing outdated information or leaving fields blank. Ensuring that the state has the most current and correct information about your business is essential for proper tax handling.

- Failure to Specify Nexus Conditions: The form requires clear responses to questions designed to determine if the business has a tax nexus in Utah. Nexus refers to the connection between the state and a business that requires the latter to collect and remit tax. Often, businesses inadvertently overlook or incorrectly answer these questions, failing to include detailed attachments when more information is necessary. This can lead to an incorrect assessment of tax obligations.

- Overlooking Additional Sheets for Detailed Information: The Utah TC-51 Form allows—or in certain situations, requires—the inclusion of additional sheets for more detailed explanations, especially regarding the nature of the business, descriptions of property or services sold, and specifics on nexus-related activities. Neglecting to attach these additional sheets, if needed, may result in incomplete disclosures and potential compliance issues.

- Misunderstanding the Type of Business Structure: The form asks for the type of business (e.g., Corporation, Sole Proprietor, L.L.C., Partnership, etc.). A common mistake is misidentifying the type of business structure, which can affect how taxes are calculated and assessed. Each structure has different tax implications, so selecting the correct one is crucial for accurate tax reporting and compliance.

- Inaccurately Reporting Sales and Transactions: The section requesting details on Utah sales, the number of Utah customer transactions, and total sales to all customers requires careful attention. Businesses sometimes inaccurately report these figures due to misunderstandings about what qualifies as a Utah sale or transaction. This information plays a pivotal role in determining tax obligations, so precision here is non-negotiable.

In summary, while filling out the Utah TC-51 form might seem straightforward, these common mistakes can lead to significant issues with tax compliance. Careful attention to detail, ensuring complete and accurate responses, and providing supplementary information as needed can help businesses avoid these pitfalls. As always, consulting with a tax professional can further ensure compliance and prevent potential errors on critical tax documents.

Documents used along the form

When a business engages with the Utah State Tax Commission by submitting the TC-51 form, a range of other documents and forms might be needed to ensure thorough and accurate reporting. These documents are essential for various situations, including providing detailed business information, establishing tax obligations, and maintaining compliance with Utah state tax laws.

- TC-20 or TC-20S: Corporate Franchise or Income Tax Return. This form is used by corporations or S corporations operating in Utah to report their income tax obligations.

- Schedule K-1: Shareholder's Share of Income, Deductions, Credits, etc. This form accompanies the TC-20 or TC-20S and details the individual share of income or loss for shareholders of S corporations or partners in a partnership.

- Form TC-40: Individual Income Tax Return. This document is for individuals, including sole proprietors, to file their personal income taxes, which may include income derived from business activities within Utah.

- Form 1099: Miscellaneous Income. Businesses may need to submit this form for any payments made to independent contractors, freelancers, or others who provide services to the company.

- Form W-9: Request for Taxpayer Identification Number and Certification. Companies often collect this form from vendors, contractors, and other payees to accurately report on their taxes and ensure compliance.

- TC-69: Utah State Business and Tax Registration. Businesses starting, expanding, or finding that their activities create a tax nexus within Utah will use this form to register with the Utah State Tax Commission and other state agencies.

- TC-160: Credit for Income Tax Paid to Another State. This form is relevant for businesses and individuals who owe taxes in another state as well as Utah, allowing them to avoid double taxation on the same income.

- Form TC-941: Employer's Quarterly Withholding Return. Employers use this form to report income taxes withheld from their employees' wages.

Together with the Utah TC-51 form, these documents facilitate a comprehensive approach to tax compliance. They help clarify the financial and operational standings of a business, ensuring that all tax obligations are met and accurately reported in alignment with Utah's tax codes and regulations.

Similar forms

The Uniform Business Office Questionnaire mirrors the Utah TC-51 form in its structure and intention. Both documents collect comprehensive information about a business's operations, including company identity, business nature, and financial activities within a specific jurisdiction. They aim to establish a company's nexus or connection to a location for tax purposes, requiring details about physical presence, sales activities, and interactions with local customers. This groundwork helps tax authorities determine tax obligations and ensures businesses comply with local tax statutes.

Similar to the Utah TC-51 form, the Nexus Determination Questionnaire for Sales and Use Tax purposes seeks detailed information to ascertain whether a business has a significant enough connection to a state, warranting sales and use tax collection and remittance responsibilities. It inquires about physical presence, such as offices or warehouses, and economic activity thresholds, such as the amount of sales or the number of transactions in the state. These elements are critical for states to apply the correct tax laws based on the Supreme Court's Wayfair decision, which expanded states' abilities to impose tax collection duties on out-of-state sellers.

The State Franchise or Business Privilege Tax Nexus Questionnaire is another document resembling the Utah TC-51 form. This questionnaire examines whether a business's activities within a state subject it to franchise or business privilege taxes, which are taxes levied for the privilege of doing business in a state. It delves into areas like physical presence, employee activities, and the nature of intrastate and interstate transactions, similar to how the TC-51 assesses a business’s engagement within Utah for tax compliance purposes.

The Multi-State Jurisdictional Business Activity Questionnaire shares similarities with the Utah TC-51 form by probing the extent of a business's operations across multiple states to discern its tax obligations. This document typically requests information on physical locations, employee presence, sales figures, and property holdings in various jurisdictions. The objective is to clarify in which states a business must register and report taxes, paralleling the TC-51's focus on identifying nexus within Utah.

Lastly, the Voluntary Disclosure Agreement (VDA) Application resembles the Utah TC-51 form as it is utilized by businesses seeking to proactively disclose unreported tax liabilities in exchange for potential forgiveness of penalties and a limitation on the look-back period. While the VDA application process involves revealing past business activities, sales data, and nexus-establishing behaviors similar to the TC-51, it is specifically targeted towards resolving prior tax compliance oversights and establishing a go-forward compliance basis.

Dos and Don'ts

When completing the Utah TC-51 form, ensure accuracy and compliance by considering the following dos and don'ts:

Do:

- Provide accurate information : Ensure all data, including company name, address, Federal ID number, and contact details, are current and match official records.

- Check the appropriate boxes that accurately represent your business type (Corporation, Sole Proprietor, L.L.C., Partnership, or Other).

- Attach additional sheets if necessary , especially when detailing the nature of your business and the description of property and/or services sold, to provide comprehensive information.

- Answer all Nexus Questions truthfully , indicating "Yes" or "No," and provide additional information on a separate sheet when required, referencing the question number for clarity.

- Sign and date the form under the Signatures section, ensuring that an officer of the corporation or the authorized preparer completes this part to certify the accuracy of the information provided.

Don't:

- Leave sections blank : Incomplete forms may result in processing delays or requests for additional information, potentially hindering your business operations.

- Guess on dates or numbers : When providing dates for when business began or ended in Utah or reporting Utah sales and transactions, ensure the information is exact to avoid discrepancies or potential legal issues.

- Omit contact details : Failing to include a way for the Utah State Tax Commission to reach you could lead to unresolved queries or issues regarding your Nexus status or tax obligations.

- Forget to check for special conditions under which your business operates in Utah, such as acting as a voluntary seller under the Streamlined Sales Tax Agreement. Review these conditions carefully and answer accordingly.

- Use outdated or incorrect forms : Always download the latest version of the TC-51 form from the official Utah State Tax Commission website to ensure compliance with current regulations and requirements.

Misconceptions

There are several misconceptions about the Utah TC-51 form that people might have. Here’s a closer look at some of these misconceptions and the facts surrounding them.

Only Utah-based businesses need to fill it out: This is incorrect. Any business, regardless of where it is based, must complete the form if it conducts business activities in Utah that establish a nexus, or connection, sufficient to require tax reporting and payment.

It's only for large corporations: The TC-51 form applies to businesses of all sizes and structures, including sole proprietorships, partnerships, LLCs, and corporations, as long as they have a nexus with Utah.

Completing this form automatically registers the business for tax: Submitting the TC-51 is part of the process of determining a business’s tax obligations in Utah. It does not, by itself, register the business for tax purposes. Additional steps may be required.

It’s a one-time requirement: Depending on a company’s activities and changes in its business, it might need to submit this form more than once. Changes in business operations or expansion of services could necessitate a new submission.

Only for those with a physical presence in Utah: While physical presence is a clear nexus indicator, having economic activities such as sales that exceed certain thresholds can also require a business to fill out the form, even without a physical presence.

The form is complicated and requires legal expertise: While the form does ask for detailed information about a business's activities in Utah, it is designed to be completed by the business or its representatives without necessarily needing legal help.

You need to know your exact sales to complete it: While having accurate sales figures is helpful, the form is primarily concerned with whether your business activities meet the nexus criteria that would necessitate tax collection and reporting in Utah.

Filing this form means you will owe taxes in Utah: Not necessarily. The form helps determine if your business has a tax obligation. Depending on your activities and the nature of your transactions, you may or may not owe taxes.

It’s only concerning sales tax: The TC-51 form is used to assess not just sales tax but also any corporation franchise or income tax obligations a business may have in Utah.

Understanding these facts can help ensure that businesses comply with Utah’s tax laws correctly and avoid misconceptions that can lead to errors or oversights in tax reporting and payment obligations.

Key takeaways

Understanding the nuances of the Utah TC-51 form is crucial for businesses operating or planning to operate within the state. This form, specifically designed by the Utah State Tax Commission, plays a significant role in determining a company's tax obligations based on its economic and physical presence in Utah. Here are some key takeaways to guide you through filling out and using the Utah TC-51 form:

- Company Information: The form begins by requesting basic but essential details about your business such as the exact business name, principal office address, federal ID number, and a contact person. Accurately providing this information ensures that the Tax Commission can correctly identify and communicate with your entity.

- Business Operations: You must specify the type of business (e.g., Corporation, Sole Proprietor, LLC, Partnership, or Other), and outline the first date your business began operations or income was derived from sources within Utah. If applicable, the date business activities ceased should also be recorded.

- Nexus Questionnaire: The core of the form is dedicated to understanding your business's nexus within Utah through a series of detailed questions. Nexus refers to the connection between a taxing jurisdiction and a taxpayer. If a business has nexus in Utah, it is obligated to pay and collect taxes on sales within the state.

- Sales and Transactions: Information regarding your company's Utah sales, number of transactions with Utah customers, and total sales to all customers over the last three years is requested. This data helps assess your tax liability and compliance with state tax laws.

- Nature of Business Operations: The form requires a clear description of the nature of your business and the type of property or services sold. Understanding whether your enterprise deals with resellers, final consumers, or both, affects tax considerations.

- Physical Presence: Questions related to the physical presence, such as having an office, warehouse, or conducting solicitations in Utah, are pivotal. These factors significantly contribute to establishing nexus and subsequent tax obligations.

Employee and Contractor Activities: The activities performed by your employees, agents, or contractors within Utah can establish nexus for tax purposes. Clarification on whether your agents represent your corporation exclusively in Utah is sought to determine the extent of your business activities and responsibilities in the state. - Voluntary Seller under the Streamlined Sales Tax Agreement: For businesses that do not have a significant physical presence in Utah, the form inquires if you qualify as a voluntary seller under the Streamlined Sales Tax Agreement. This section reflects compliance with broader multi-state sales tax systems.

- Certification: The declaration by an officer of the corporation at the end of the questionnaire certifies under penalty of perjury that the information provided is true, correct, and complete. This underscores the seriousness of the document and the importance of accurate representation of your business activities within Utah.

Filling out the Utah TC-51 form with accuracy and care is not merely a bureaucratic necessity; it's a step towards ensuring your business operates in compliance with Utah's tax laws. The information provided helps the Utah State Tax Commission to accurately assess tax liabilities, ensuring that businesses contribute their fair share towards the state's economy and public services.

Common PDF Templates

Medical Power of Attorney Utah - Revoke or amend your Utah Advance Health Care Directive easily with provisions that respect your changing wishes and circumstances over time.

Utah Tax Forms - Filing a TC-941D form is a step towards resolving withholding tax conflicts arising from business entity changes or mergers in Utah.