Blank Utah Tc 41 Form

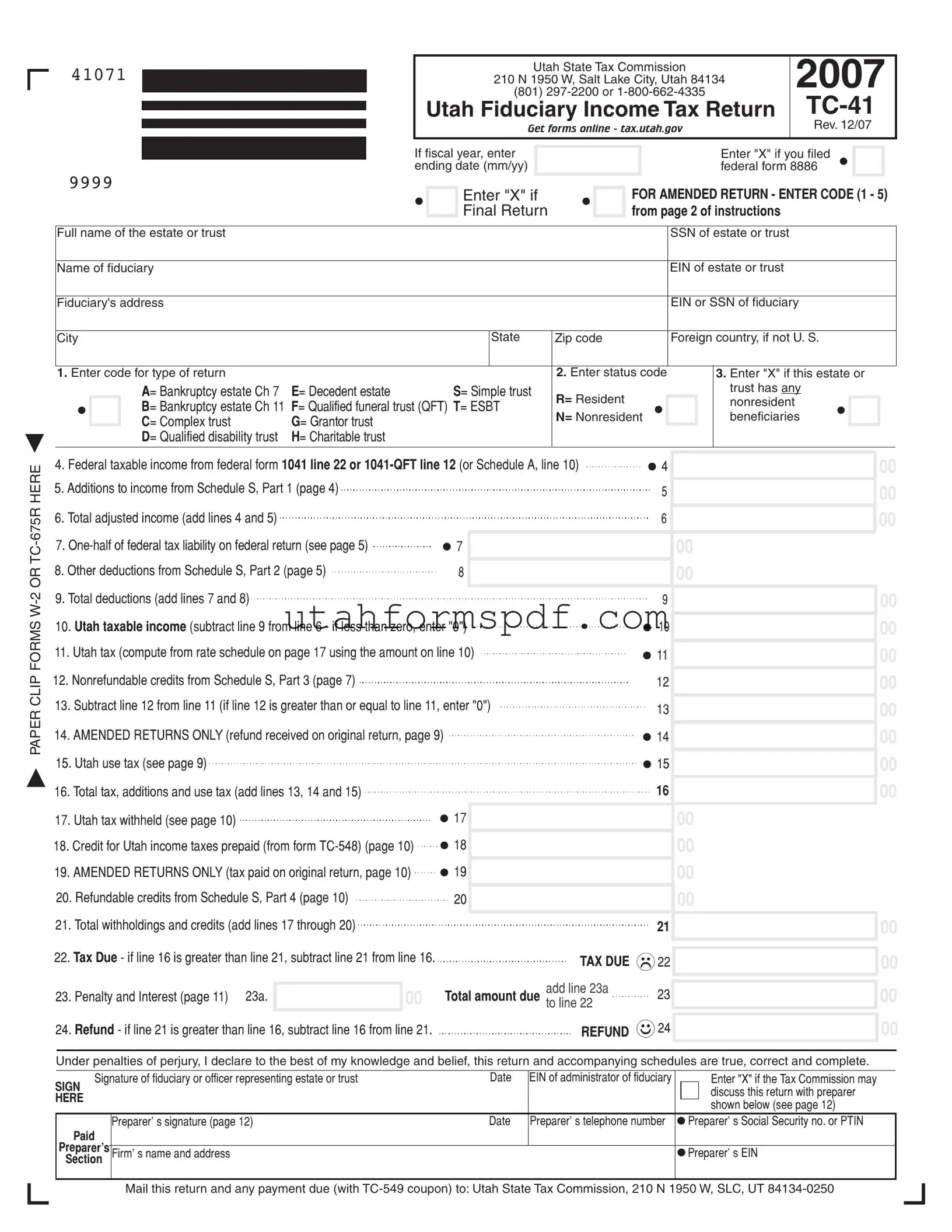

The Utah TC-41 form, a cornerstone for fiduciaries managing estate or trust tax affairs within the state, serves as a comprehensive filing tool structured by the Utah State Tax Commission. Located in Salt Lake City, the commission oversees the intricate process of fiduciary income tax return submission, offering guidance through their accessibility via both phone and their website. The form, meticulously revised in December 2007, caters to various fiduciary entities including estates, trusts, and bankruptcy estates, among others, by facilitating the reporting of income, adjustments, and credits. Fiduciaries are required to signify their federal filing status, detail their income adjustments, and calculate their tax liabilities and potential refunds. Additionally, for nonresident entities, the form demands an outline of income sourced within Utah. Completing the TC-41 is critical for accurately establishing the tax obligations of estates and trusts, encompassing details such as federal taxable income, adjustments specific to Utah, nonrefundable and refundable credits, and direct allocations for nonresident entities. This meticulous process ensures fiduciaries are able to comply with state tax mandates, avoid potential penalties for inaccuracies, and, where applicable, secure refunds, thereby emphasizing the importance of the TC-41 form in managing the fiscal responsibilities of trusts and estates in Utah.

Form Preview Example

|

|

|

|

|

|

|

|

|

(801) |

|

|

2007 |

||||||||||

41071 |

|

|

|

|

|

|

Utah State Tax Commission |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

210 N 1950 W, Salt Lake City, Utah 84134 |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

Utah Fiduciary Income Tax Return |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

Get forms online - tax.utah.gov |

|

|

|

Rev. 12/07 |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

If fiscal year, enter |

|

|

|

|

|

|

|

Enter "X" if you filed |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

ending date (mm/yy) |

|

|

|

|

|

|

|

federal form 8886 |

|

|

||||||

9999 |

|

|

|

|

|

|

Enter "X" if |

|

|

FOR AMENDED RETURN - ENTER CODE (1 - 5) |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

Final Return |

|

|

from page 2 of instructions |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Full name of the estate or trust |

|

|

|

|

|

|

|

|

|

|

|

SSN of estate or trust |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Name of fiduciary |

|

|

|

|

|

|

|

|

|

|

|

EIN of estate or trust |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Fiduciary's address |

|

|

|

|

|

|

|

|

|

|

|

EIN or SSN of fiduciary |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

City |

|

|

|

|

|

State |

Zip code |

|

|

Foreign country, if not U. S. |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1. Enter code for type of return |

|

|

|

|

|

|

|

2. Enter status code |

3. Enter "X" if this estate or |

|||||||||||||

|

|

A= Bankruptcy estate Ch 7 |

E= Decedent estate |

|

S= Simple trust |

R= Resident |

|

|

|

|

trust has any |

|

|

|

||||||||

|

|

B= Bankruptcy estate Ch 11 |

F= Qualified funeral trust (QFT) T= ESBT |

|

|

|

|

nonresident |

|

|

|

|

||||||||||

|

|

N= Nonresident |

|

|

beneficiaries |

|

|

|

||||||||||||||

|

|

C= Complex trust |

G= Grantor trust |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

D= Qualified disability trust |

H= Charitable trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PAPER CLIP FORMS

4. Federal taxable income from federal form 1041 line 22 or |

4 |

|

||||

5. Additions to income from Schedule S, Part 1 (page 4) |

|

|

|

5 |

|

|

|

|

|

|

|

|

|

6. Total adjusted income (add lines 4 and 5) |

|

|

|

6 |

|

|

|

|

|

|

|||

|

|

|

|

|||

7. |

|

7 |

|

|

|

|

|

|

|

|

|||

8. Other deductions from Schedule S, Part 2 (page 5) |

|

8 |

|

|

|

|

|

|

|

|

|||

9. Total deductions (add lines 7 and 8) |

|

|

|

|

|

|

|

|

|

9 |

|

||

|

|

|

|

|||

10. Utah taxable income (subtract line 9 from line 6 - if less than zero, enter "0") |

10 |

|

||||

|

||||||

11. Utah tax (compute from rate schedule on page 17 using the amount on line 10) |

11 |

|

||||

12. Nonrefundable credits from Schedule S, Part 3 (page 7) |

|

|

|

12 |

|

|

13. Subtract line 12 from line 11 (if line 12 is greater than or equal to line 11, enter "0") |

13 |

|

||||

|

|

|

|

|

|

|

14. AMENDED RETURNS ONLY (refund received on original return, page 9) |

|

|

14 |

|

||

15. Utah use tax (see page 9) |

|

|

|

15 |

|

|

16. Total tax, additions and use tax (add lines 13, 14 and 15) |

|

|

|

16 |

|

|

|

|

|

|

|||

17. Utah tax withheld (see page 10) |

|

17 |

|

|

|

|

18. Credit for Utah income taxes prepaid (from form |

18 |

|

|

|

||

19. AMENDED RETURNS ONLY (tax paid on original return, page 10) |

19 |

|

|

|

||

|

|

|

||||

20. Refundable credits from Schedule S, Part 4 (page 10) |

|

20 |

|

|

|

|

|

|

|

|

|||

21. Total withholdings and credits (add lines 17 through 20) |

|

|

|

|

|

|

|

|

|

21 |

|

||

22. Tax Due - if line 16 is greater than line 21, subtract line 21 from line 16. |

|

TAX DUE |

22 |

|

||

|

|

|||||

|

|

|

|

|

||

|

|

00 |

|

add line 23a |

23 |

|

|

|

|

|

|||

23. Penalty and Interest (page 11) 23a. |

|

Total amount due to line 22 |

|

|||

|

|

|

||||

24. Refund - if line 21 is greater than line 16, subtract line 16 from line 21. |

|

REFUND |

24 |

|

||

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Under penalties of perjury, I declare to the best of my knowledge and belief, this return and accompanying schedules are true, correct and complete.

SIGN |

Signature of fiduciary or officer representing estate or trust |

Date |

EIN of administrator of fiduciary |

|

|

Enter "X" if the Tax Commission may |

||

|

|

|

|

|

|

|

discuss this return with preparer |

|

HERE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

shown below (see page 12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer' s signature (page 12) |

Date |

Preparer' s telephone number |

|

Preparer' s Social Security no. or PTIN |

|

Paid |

|

|

|

|

|

|

||

Preparer’s |

|

|

|

|

|

|

|

|

|

Firm' s name and address |

|

|

|

Preparer' s EIN |

|||

Section |

|

|

|

|||||

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

Mail this return and any payment due (with

41072

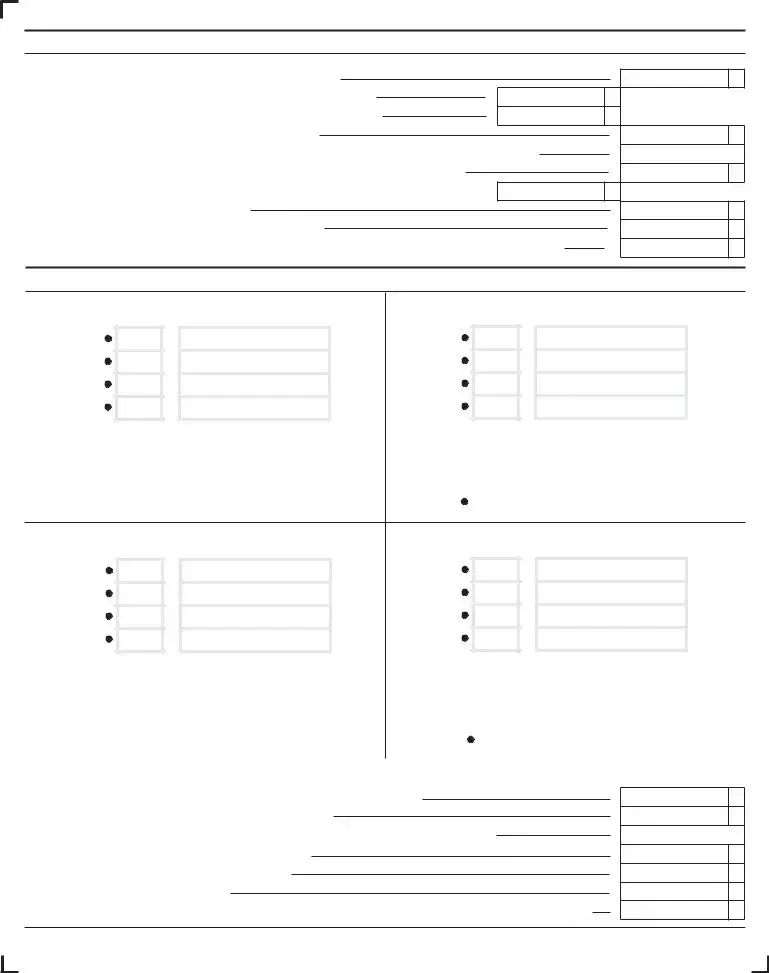

Schedule A – Nonresident Estate or Trust (computation of federal taxable income)

To be completed by all nonresident estates or trusts. |

|

1. Total income from federal form 1041 line 9 or |

|

2. Ordinary income derived from Utah sources (attach schedule - page 13) |

2 |

3. Utah capital gain or (loss) from Utah sources (attach schedule – page 13) |

3 |

4.Total income derived from Utah sources (add lines 2 and 3)

5.Percent of total federal income derived from Utah sources (line 4 divided by line 1 - not greater than 100%)

6.Deductions from federal form 1041or

7. Deductions from federal form 1041 or

8.Allocable amount (line 7 multiplied by line 5)

9.Total deductions allocable to Utah income (add lines 6 and 8)

10. Federal taxable income derived from Utah sources (line 4 less line 9). Enter here and on line 4 on front of form

1

00

00

4

5

6

00

8

9

10

00

00

%

00

00

00

00

Schedule S - Supplemental Schedule

PART 1: ADDITIONS TO INCOME (see codes and descriptions on page 4) |

PART 2: OTHER DEDUCTIONS (see codes and descriptions on page 5) |

Code |

Amount |

Code |

Amount |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

Total additions to income |

|

00 |

Total other deductions |

|

|

00 |

|

|

(enter total on page 1, line 5) |

|

(enter total on page 1, line 8) |

|

|

|

|||

|

|

|

If deducting Native American Income (code 77), write the |

|

|

|

||

|

|

|

enrollment number and tribe code. |

Tribe code |

||||

|

|

|

|

|

|

|||

|

|

|

Enrollment |

|

|

|

|

|

|

|

|

number |

|

|

|

|

|

PART 3: NONREFUNDABLE CREDITS (see codes and descriptions on page 7) |

PART 4: REFUNDABLE CREDITS (see codes and descriptions on page 10) |

||

Code |

Amount |

Code |

Amount |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

Total nonrefundable credits |

|

00 |

|

Total refundable credits |

|

|

00 |

||

(enter total on page 1, line12) |

|

|

(enter total on page 1, line 20) |

|

|

||||

|

|

|

|

|

|

||||

If claiming the Qualified Sheltered Workshop cash contribution |

If claiming the Nonresident Shareholder' s WithholdingTax |

||||||||

credit (code 02), write the Qualified Sheltered Workshop name. |

Credit (code 43), write the S corporation federal ID number. |

||||||||

Name |

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART 5: Credit for fiduciary income tax paid to another state (page 8). Enter code 17 and amount from line 7 below on Part 3, Nonrefundable Credits above. Complete a separate Part 5 for each state for which you are claiming a credit.

1. Total income taxed in state of: |

|

|

1 |

|

|||

2. Total income from federal form 1041 line 9 or |

2 |

||

3. Percent other state income bears to total income (line 1 divided by line 2 - not greater than 100%) |

3 |

||

4. Utah fiduciary tax as computed on line 11 on front of form |

4 |

||

5. Credit limitation (line 4 multiplied by percent on line 3) |

5 |

||

6. Fiduciary tax paid to state listed on line 1 |

6 |

||

7. Credit for fiduciary taxes paid to other state (line 5 or 6, whichever is less) Enter code 17 and credit on Sch. S, Part 3 above. |

7 |

||

00

00

%

00

00

00

00

Form Breakdown

| Fact Name | Description |

|---|---|

| Form Purpose | The Utah TC-41 form is used for filing Fiduciary Income Tax Returns for estates and trusts in the state of Utah. |

| Relevant Contacts | Contact information for assistance includes a phone number (801) 297-2200 or toll-free 1-800-662-4335, and the form can be sent to the Utah State Tax Commission at 210 N 1950 W, Salt Lake City, Utah 84134. |

| Form Availability | Forms and instructions for the Utah TC-41 can be obtained online via the Utah State Tax Commission's website at tax.utah.gov. |

| Governing Laws | The form is governed by Utah state tax laws and regulations related specifically to the filing of fiduciary income tax. |

Detailed Steps for Writing Utah Tc 41

Filing out the Utah TC-41 form is an essential step for trustees and fiduciaries in reporting income tax for estates or trusts. This guide will help simplify the process, ensuring all necessary information is accurately included for a successful submission. It's important to gather all relevant financial documents and understand the estate or trust's income and deductions before beginning. Follow these steps to ensure the form is completed correctly.

- Begin by entering the full name of the estate or trust and the SSN or EIN associated with it in the designated fields.

- Fill in the name of the fiduciary and their contact information, including the fiduciary's address, city, state, and zip code. If the address is not in the U.S., specify the foreign country.

- Mark an "X" in the corresponding box if you are filing an amended return, and enter the code (1-5) as instructed in the form's instructions. If this is a final return, also mark the appropriate box.

- Select the code for the type of return you are filing from the options listed (A-H) based on the nature of the estate or trust.

- Enter the federal taxable income from federal form 1041 line 22 or 1041-QFT line 12, or Schedule A line 10 if applicable.

- Compute any additions to income from Schedule S, Part 1, and list the total in the provided field.

- Calculate the total adjusted income by adding lines 4 and 5.

- List one-half of the federal tax liability from the federal return as indicated on the form instructions.

- Add any other deductions from Schedule S, Part 2, tallying up the total deductions.

- Determine the Utah taxable income by subtracting the total deductions from the total adjusted income; enter "0" if the result is less than zero.

- Calculate the Utah tax due using the rate schedule provided in the form instructions based on the amount on line 10.

- Identify and list any nonrefundable credits from Schedule S, Part 3.

- Subtract the nonrefundable credits from the Utah tax to calculate the tax after credits; enter "0" if line 12 is greater than or equal to line 11.

- For amended returns only, enter any refund received or tax paid on the original return as specified.

- Add any Utah use tax due as instructed on the form.

- Sum the total tax, additions, and use tax for the complete tax responsibility.

- Report any Utah tax withheld and credit for Utah income taxes prepaid, including any payments made with form TC-548.

- Add any refundable credits from Schedule S, Part 4.

- Calculate the total withholdings and credits by adding lines 17 through 20.

- Determine the tax due or refund amount based on whether line 16 is greater than line 21. Compute any penalty and interest if applicable.

- Have the fiduciary sign and date the form, providing their EIN if the fiduciary is an administrator. Paper clip any required forms such as W-2 or TC-675R to the front.

- If prepared by someone other than the fidiciary, the preparer must also sign and date the form, including their telephone number, SSN or PTIN, and their firm's information.

- Review the form for completeness and accuracy, then mail it with any payment due (and TC-549 coupon if applicable) to the address provided by the Utah State Tax Commission.

By carefully following these steps, you’ll ensure the Utah TC-41 form is correctly completed and submitted, helping to avoid any complications or delays in processing.

Common Questions

-

What is the Utah TC-41 form?

The Utah TC-41 form is a Fiduciary Income Tax Return used by estates and trusts to report income, deductions, gains, losses, and taxes due to the state of Utah. It is similar to the federal form 1041 but specifically designed for filing state taxes in Utah.

-

Who needs to file the TC-41 form?

Estate and trust entities with taxable income generated in Utah or responsible for managing income on behalf of others in Utah must file the TC-41 form. This includes bankruptcy estates, decedent estates, simple trusts, complex trusts, grantor trusts, and nonresident trusts with income from Utah sources.

-

How do you know if you need to amend a previously filed TC-41?

If there are corrections to be made to any information or amounts reported on a previously filed TC-41 form, such as income, deductions, or credits, an amended return must be filed. The form includes a specific section for marking it as an amended return and entering the correct code (1-5) based on the amendment's reason.

-

How is taxable income on the TC-41 calculated?

Taxable income on the TC-41 form is calculated by adjusting the federal taxable income, which is reported on federal form 1041 line 22 or 1041-QFT line 12, with additions and deductions specific to Utah state tax laws as outlined in Schedule S of the TC-41 form.

-

What are nonrefundable and refundable credits on the TC-41?

Nonrefundable credits, listed in Schedule S Part 3, directly reduce the tax liability but not below zero. Refundable credits, detailed in Schedule S Part 4, can reduce the tax liability to below zero, potentially resulting in a refund. These credits include taxes paid to other states or specific contributions eligible for credits in Utah.

-

How does an estate or trust file for a tax refund using the TC-41?

If the total withholdings and credits, line 21, exceed the total tax, additions, and use tax, line 16, the estate or trust can report this overpayment on the TC-41 form. The difference, if approved by the Utah State Tax Commission, will be refunded to the fiduciary or directly to the estate or trust.

-

What if the estate or trust incurs a tax due?

If the total tax, additions, and use tax, line 16, is greater than the total withholdings and credits, line 21, the resulting amount is the tax due to the state of Utah. This amount should be calculated and reported on line 22 of the TC-41 form, and payment should be submitted to the Utah State Tax Commission by the filing deadline to avoid penalties and interest.

-

Where should the completed TC-41 form be sent?

The completed TC-41 form, along with any payment due, should be mailed to the Utah State Tax Commission at the address provided on the form: 210 N 1950 W, SLC, UT 84134-0250. It is important to include the correct forms and schedules to ensure the return is processed correctly.

Common mistakes

Filling out the Utah TC-41 form correctly is crucial for ensuring an accurate fiduciary income tax return. However, errors are common, leading to unnecessary complications. Here are eight common mistakes:

- Not indicating the correct type of return by entering the appropriate code in item 1. This mistake can lead to incorrect processing of the return.

- Forgetting to enter the "X" in the box if the return is amended or if the filer has included federal form 8886. This causes confusion and might lead to delays.

- Incorrectly entering the Social Security Number (SSN) or Employer Identification Number (EIN) for both the estate or trust and the fiduciary. Accurate identification numbers are critical for proper tax record maintenance.

- Omitting or inaccurately reporting federal taxable income from federal form 1041 line 22 or 1041-QFT line 12. This information is essential for determining the correct Utah taxable income.

- Failing to attach necessary documents, such as Forms W-2 or TC-675R, when required can lead to an incomplete return.

- Not properly calculating Utah taxable income by incorrectly adding or subtracting income and deductions. This directly affects the tax calculation.

- Misunderstanding the sections for additions to income, deductions, and credits. These sections require careful attention to ensure that all financial information is correctly accounted for and valid credits are claimed.

- Inaccurate calculation of penalty and interest or failing to include these amounts when due. This error can result in the underpayment of the total amount owed to the Utah State Tax Commission.

Each of these mistakes can be avoided by carefully reviewing the instructions provided by the tax.utah.gov website and double-checking all entries before submission. It’s also beneficial to consult with a tax professional if there are any uncertainties.

To avoid these common pitfalls, it's recommended to:

- Take your time: Rushing through tax forms increases the likelihood of errors. Allocate sufficient time to accurately complete the TC-41.

- Review twice: Double-check your entries against the source documents for accuracy.

- Consult the instructions: The Utah State Tax Commission provides detailed instructions that can clarify how to correctly fill out each section of the form.

- Seek professional help: When in doubt, consulting with a tax expert can save time and prevent costly mistakes.

Attention to detail can significantly streamline the process of filing the Utah TC-41 form, ensuring accuracy and compliance with Utah tax laws.

Documents used along the form

When filing the Utah TC-41 form, it's essential for estates or trusts to have all necessary documentation prepared for a complete and accurate tax return. This includes various forms and documents that supplement the information on the TC-41 or are required for special circumstances. The following list outlines seven key documents and forms that are commonly used in conjunction with the Utah TC-41 form.

- Schedule A – Nonresident Estate or Trust: This schedule is necessary for all nonresident estates or trusts, detailing federal taxable income allocations from Utah sources.

- Schedule S – Supplemental Schedule: Comprises various parts including additions to income, other deductions, nonrefundable credits, and refundable credits, providing a detailed breakdown of adjustments to the income and taxes due.

- Form TC-548 – Prepayment of Tax: This form is used to document any Utah income taxes prepaid by the estate or trust, which could affect the balance of taxes owed or refunded.

- Form TC-675R – Statement of Withholding on Utah Source Income for Nonresident Individual: This form is critical for estates or trusts with nonresident beneficiaries, detailing Utah tax withheld from distributions.

- TC-549 – Payment Coupon: If the estate or trust owes taxes, this coupon accompanies the payment to ensure correct processing.

- Federal Form 1041: The U.S. Income Tax Return for Estates and Trusts, which shows federal taxable income that will be necessary for completing the TC-41 form.

- Federal Schedule K-1 (1041): Provides the beneficiary's share of the estate's or trust's income, deductions, and credits. It's crucial for both the fiduciary's and the beneficiaries' tax filings.

The proper completion and submission of these accompanying documents, as applicable, ensure compliance with Utah's tax laws and help avoid potential errors or delays in processing. Always verify the current requirements and forms needed for the specific tax year, as these can change over time.

Similar forms

The Utah Fiduciary Income Tax Return, TC-41, shares similarities with the Federal Form 1041, U.S. Income Tax Return for Estates and Trusts. Both forms are designed to report income, deductions, and taxes payable by estates and trusts. The TC-41 form mirrors the structure of Form 1041 by requiring information on the entity's taxable income, adjustments, and credits, demonstrating a consistent approach to taxation for these entities at both the state and federal levels. This alignment ensures fiduciaries can navigate their tax responsibilities with a degree of familiarity across jurisdictions.

Similar to the Utah TC-41, the Schedule K-1 (Form 1041) for the IRS is a document that details the distribution of income and deductions from an estate or trust to its beneficiaries. While TC-41 focuses on the estate or trust's overall income tax liability, Schedule K-1 breaks down how much of this income and related deductions are attributable to each beneficiary. This common purpose of delineating the flow of taxable income and deductions from the entity to the individual highlights the complementary relationship between these forms in the broader tax reporting landscape.

The TC-41 form also parallels the IRS's Form 1041-QFT, U.S. Income Tax Return for Qualified Funeral Trusts, in its specialized approach to handling the unique considerations of a specific type of trust. The TC-41 makes provisions for reporting income from Qualified Funeral Trusts (QFTs) among other types, reflecting an understanding that different trusts operate under varying tax rules and structures. Both forms accommodate these nuances, ensuring that such trusts are taxed appropriately while minimizing the compliance burden on trustees.

The Utah Nonresident Trustee Tax Schedule, a component of the broader TC-41 filing process for nonresident estates or trusts, bears resemblance to the Multi-state Fiduciary Income Tax forms used by various states. These forms calculate the fiduciary income tax for entities with income sources or beneficiaries in multiple states, requiring an apportionment of income. By incorporating a similar requirement, the TC-41 ensures that income attributable to Utah sources is accurately reported and taxed, facilitating fair and equitable tax administration across state lines.

Another document related to TC-41 is the Utah Taxpayer Advocate Service Form, a utility form for disputes or issues with the tax filing. While this form is not used for reporting income or tax directly, it serves as a crucial support document for entities that might encounter difficulties or discrepancies when filing returns like the TC-41. It exemplifies the broader ecosystem of tax documentation, where reporting forms and support mechanisms work in tandem to ensure a smooth tax administration process.

The TC-41’s references to the use of Federal Form 8886, Reportable Transaction Disclosure Statement, showcase its similarity to federal tax compliance mechanisms for disclosing specific transactions that could affect tax liabilities. By requiring an acknowledgment of filing Form 8896 for relevant entities, TC-41 aligns with the IRS's broader objectives to maintain transparency and oversight over complex transactions potentially impacting the tax landscape. This harmonization between state and federal requirements underscores a joint effort in combating tax evasion and ensuring compliance.

Lastly, akin to the TC-41 form, the Amendatory Schedules used to correct or update previously filed tax returns serve a parallel purpose. Whether adjusting a federal Form 1040 for individuals or a state-specific TC-41 for estates and trusts, these amendatory documents are vital for maintaining accuracy and compliance in tax records. They embody the tax system's adaptability, allowing taxpayers to rectify errors or omissions and align their tax liabilities with their actual income and deductions.

Dos and Don'ts

Filling out the Utah TC-41 form, the Utah Fiduciary Income Tax Return, requires precision and attention to detail. Whether you're handling it for the first time or you're somewhat familiar with the process, it's essential to know the dos and don'ts to ensure accuracy and compliance with Utah tax laws. Below, we've outlined some key points to assist you on this journey.

Do:- Double-check the Social Security Number (SSN) or Employer Identification Number (EIN) of the estate or trust, as well as the fiduciary's information. Accuracy here is vital for proper tax reporting and identification.

- Use the correct codes for the type of return and status code, which can be found in the instructions. These codes are crucial for categorizing the return correctly.

- Include all necessary attachments and schedules, such as W-2 or TC-675R forms, if applicable. This ensures that your return is processed without unnecessary delays.

- Accurately enter the federal taxable income and any additions or deductions as required. This forms the basis of the Utah taxable income calculation.

- Ensure that the tax computed from the rate schedule correctly reflects the taxable income reported. Miscomputing can lead to understated or overstated tax liabilities.

- Sign and date the return. An unsigned return is like an unsigned check – it's not valid.

- Forget to check the box if you filed federal form 8886 or if you're filing an amended return. These checkboxes provide vital information for processing your return.

- Neglect to include the fiduciary’s address or to indicate if a trust has any nonresident beneficiaries. Both pieces of information are necessary for complete and accurate processing.

- Omit any part of the tax calculation sections, including federal tax liability, other deductions, and nonrefundable credits. Each section plays a role in determining the correct tax owed or refund due.

- Leave out the Utah use tax if applicable. Many filers overlook this, but it's an essential part of the state's tax collection efforts.

- Fail to include payment if you owe tax. Delaying payment can result in penalties and interest.

- Ignore the preparer's section if someone else prepared the return. This includes the preparer's signature, telephone number, and identification numbers, ensuring accountability and providing a point of contact for any questions.

By following these guidelines, you can fill out the Utah TC-41 form more accurately and efficiently, helping to avoid common pitfalls and ensuring compliance with state tax laws.

Misconceptions

Many people have misconceptions about the Utah TC-41 form, which can lead to confusion and potential mistakes when filing. Let's clear up some of the most common misunderstandings:

- Only for traditional trusts: People often think the TC-41 form is only for traditional trusts. However, it's also required for estates, bankruptcy estates under chapters 7 or 11, qualified funeral trusts, grantor trusts, and more. This variety means a broad range of fiduciaries might need to file it.

- Residents only: Another common belief is that the TC-41 is only for resident trusts or estates. Both resident and nonresident entities must use this form to report income derived from Utah sources or if they have any nonresident beneficiaries.

- Federal form replacements: Some assume that if they've filed the federal form 1041 or any related forms, they don't need to file a state return. The TC-41 is still necessary for Utah, as it accounts for state-specific income and deductions.

- No schedules needed: It's often misunderstood that the main form is enough. Depending on the trust or estate's income sources and deductions, supplemental schedules like Schedule S or Schedule A for nonresident entities are crucial for accurate reporting.

- Amended returns are seldom: There's a notion that amending a TC-41 form is rare. In reality, fiduciaries may need to file an amended return due to errors, overlooked deductions, or income adjustments, similar to personal tax returns.

- No penalty and interest for late filing: People sometimes believe that penalties and interest don't apply to this form. Late filings or payments can indeed incur penalties and interest, emphasizing the importance of timely compliance.

- Electronic filing isn't an option: Many are under the impression that the TC-41 must be mailed in paper form. While the Utah State Tax Commission does accept paper returns, electronic filing is often available and encouraged for its convenience and efficiency.

- Use tax doesn't apply: A common misconception is that use tax is irrelevant to trusts and estates. If the entity purchases goods without paying sales tax, such as online purchases, use tax might be due and reportable on the TC-41.

Clarifying these misconceptions helps in understanding the breadth of the TC-41 form’s application, ensuring that fiduciaries comply properly with Utah tax laws.

Key takeaways

When preparing the Utah TC-41, Utah Fiduciary Income Tax Return, understanding the key aspects of the form is crucial to ensure accuracy and compliance. Below are eight key takeaways to help guide you through the process:

- Ensure to mark the correct type of fiduciary return you are filing by selecting the appropriate code for the estate or trust, such as bankruptcy estate (Chapter 7 or 11), decedent estate, simple trust, complex trust, etc.

- Indicate if the form is for an amended return by entering the relevant code (1 - 5), which can be found on page 2 of the instructions.

- Accurately report the estate or trust's federal taxable income by referencing the correct line from the federal form 1041 or 1041-QFT.

- Add or subtract income adjustments as outlined on Schedule S, ensuring that all additions and deductions to income that are specific to Utah tax law are correctly calculated and reported.

- If filing for a nonresident estate or trust, provide details of income derived from Utah sources and calculate the taxable income accordingly, utilizing Schedule A for the computation.

- Utilize nonrefundable and refundable credits by accurately filling out the relevant sections on Schedule S, including any credits for taxes paid to other states.

- Be mindful of Utah-specific deductions and credits, such as deductions for Native American income or credits for qualified Sheltered Workshop contributions, and ensure they are properly documented and claimed.

- For amended returns, accurately report any refund received or tax paid on the original return, and don't forget to include details of any Utah use tax due.

Remember, accuracy is key when completing the TC-41 form. Double-check all entries, calculate carefully, and ensure that all necessary schedules and documentation are attached. Additionally, if you have any doubts or questions, consulting with a tax professional or the Utah State Tax Commission directly can provide clarification and prevent potential errors.

Common PDF Templates

Utah Tax Forms - The TC-142 form stipulates a total fee calculation for all requested special plates and decals, including handling fees.

Utah Dws Sds 305 - Structured to cover a broad spectrum of employment-related information, from personal details to specific job skills.