Blank Utah Tc 20 Form

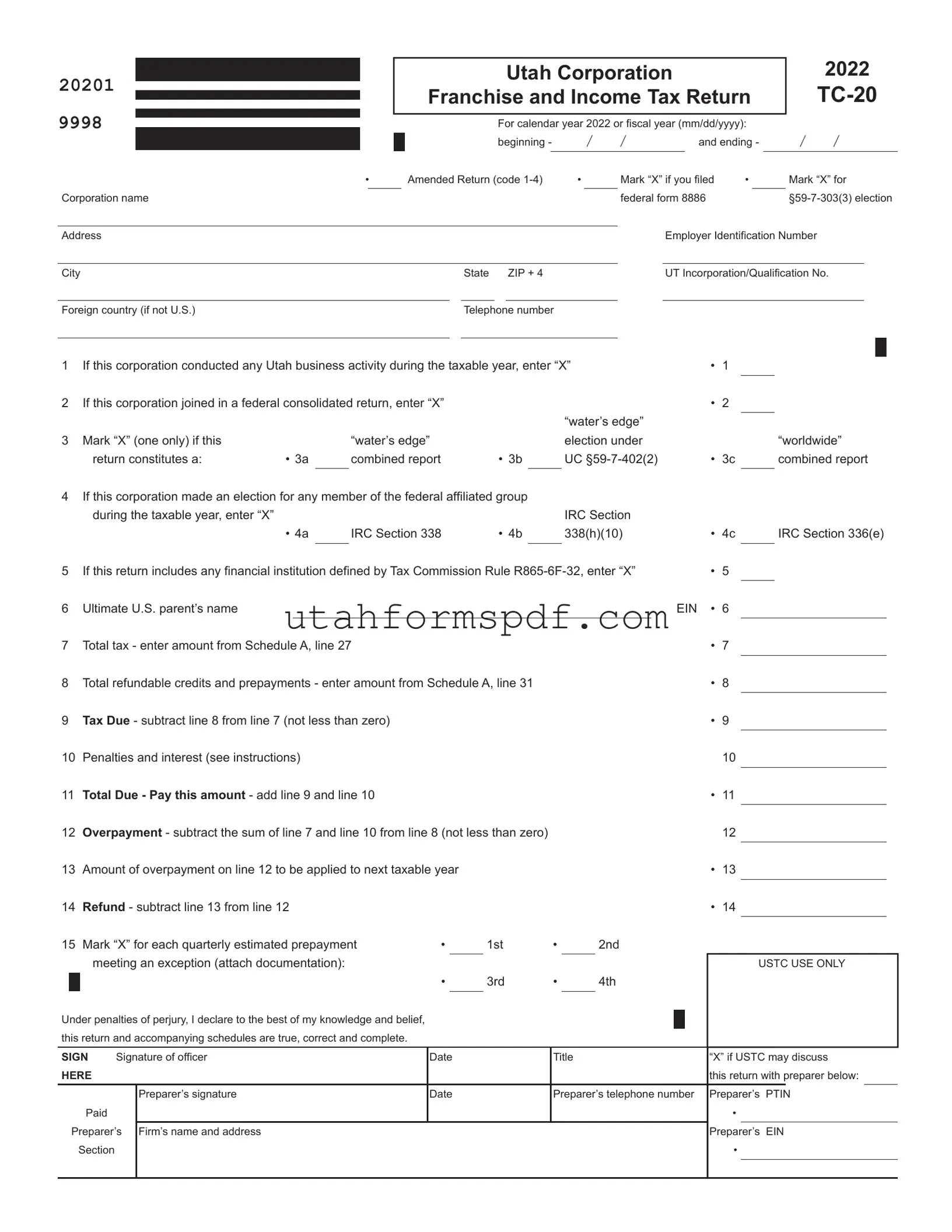

Understanding the Utah TC-20 form is crucial for corporations operating within the state. This comprehensive return, designated for the 2020 tax year, outlines the requisite details for filing both franchise and income taxes. It adapts to a range of fiscal situations, from standard calendar year filings to specific fiscal year periods, and even accommodates amended returns with distinct codes for clarification. Essential for every corporation, the form requests detailed information, such as the corporation name, address, Employer Identification Number (EIN), and the specific Incorporation/Qualification Number for Utah-based operations. Additionally, it addresses the participation in federal consolidated returns and elections that might affect the corporation's tax obligations. The document meticulously guides through deductions, additions to income, and specifics regarding the tax calculation itself. It includes sections for reporting ultimate parent information and financial institutions defined by respective rules, ensuring a thorough disclosure of financial activities within the state. The provision for estimated tax payments highlights the form's preemptive approach to fiscal responsibility. Importantly, the TC-20 form encapsulates the need for transparency, accuracy, and timely submission, underlined by a declaration that all provided information is truthful and complete to the best of the submitting officer's knowledge. Hence, the TC-20 form is not just a tax document but a critical element of a corporation's compliance and financial reporting in Utah.

Form Preview Example

20201 |

|

|

|

|

Utah Corporation |

|

|

||||

|

|

|

|

Franchise and Income Tax Return |

|||||||

9998 |

|

|

|

|

|||||||

|

|

|

|

||||||||

|

|

|

|

For calendar year 2022 or fiscal year (mm/dd/yyyy): |

|||||||

|

|

|

|

||||||||

|

|

|

|

|

beginning - |

/ |

/ |

and ending - |

|||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

||||

|

|

• |

|

Amended Return (code |

• |

Mark “X” if you filed • |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Corporation name |

|

|

|

|

|

federal form 8886 |

|||||

2022

/ /

Mark “X” for

Address |

|

|

|

|

Employer Identification Number |

|

|

|

|

|

|

|

|

City |

State |

|

ZIP + 4 |

|

UT Incorporation/Qualification No. |

|

|

|

|

|

|

|

|

Foreign country (if not U.S.) |

Telephone number |

|

|

|||

1 |

If this corporation conducted any Utah business activity during the taxable year, enter “X” |

• |

1 |

|

|

||||||

2 |

If this corporation joined in a federal consolidated return, enter “X” |

|

|

|

• |

2 |

|

|

|||

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

“water’s edge” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Mark “X” (one only) if this |

|

|

“water’s edge” |

|

|

election under |

|

|

|

“worldwide” |

|

return constitutes a: |

• 3a |

|

combined report |

• 3b |

|

UC |

• |

3c |

|

combined report |

|

|

|

|

|

|

|

|

|

|

|

|

4If this corporation made an election for any member of the federal affiliated group

|

during the taxable year, enter “X” |

|

|

|

|

IRC Section |

|

|

|

|

|

|

• 4a |

|

IRC Section 338 |

• 4b |

338(h)(10) |

• |

4c |

|

IRC Section 336(e) |

||

|

|

|

|

|

|

|

|

|

|

||

5 |

If this return includes any financial institution defined by Tax Commission Rule |

• |

5 |

|

|

||||||

6 |

Ultimate U.S. parent’s name |

|

|

|

|

|

EIN • |

6 |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Total tax - enter amount from Schedule A, line 27 |

|

|

|

• |

7 |

|

|

|||

8 |

Total refundable credits and prepayments - enter amount from Schedule A, line 31 |

|

• |

8 |

|

|

|||||

|

|

|

|||||||||

9 |

Tax Due - subtract line 8 from line 7 (not less than zero) |

|

|

|

• |

9 |

|

|

|||

|

|

|

|

|

|||||||

10 |

Penalties and interest (see instructions) |

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

|

||||

11 |

Total Due - Pay this amount - add line 9 and line 10 |

|

|

|

• |

11 |

|

|

|||

|

|

|

|

|

|||||||

12 |

Overpayment - subtract the sum of line 7 and line 10 from line 8 (not less than zero) |

|

|

12 |

|

|

|||||

|

|

|

|

||||||||

13 |

Amount of overpayment on line 12 to be applied to next taxable year |

|

|

|

• |

13 |

|

|

|||

|

|

|

|

|

|||||||

14 |

Refund - subtract line 13 from line 12 |

|

|

|

|

|

• |

14 |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

15 Mark “X” for each quarterly estimated prepayment |

• |

1st |

• |

2nd |

|

|

|

||||||||||

|

|

meeting an exception (attach documentation): |

|

|

|

|

|

|

|

|

|

USTC USE ONLY |

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

• |

3rd |

• |

4th |

|

|

|

||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare to the best of my knowledge and belief, |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

this return and accompanying schedules are true, correct and complete. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

SIGN |

Signature of officer |

Date |

|

Title |

|

|

|

“X” if USTC may discuss |

|||||||||

HERE |

|

|

|

|

|

|

|

|

|

|

this return with preparer below: |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

Preparer’s signature |

Date |

|

Preparer’s telephone number |

Preparer’s |

PTIN |

||||||||

|

|

Paid |

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Preparer’s |

Firm’s name and address |

|

|

|

|

|

|

|

|

Preparer’s |

EIN |

|||||

|

Section |

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental information to be Supplied by All Corporations |

Pg. 2 |

||||||||

20202 EIN |

|

|

|

|

|

2022 |

|

|

|

|

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

||

|

1 Date of incorporation: |

/ / |

|

State or country in which incorporated: |

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

mm/dd/yyyy

2If this corporation is dissolved or withdrawn, see Dissolution or Withdrawal in the General Instructions.

3If this corporation at any time during its tax year owned more than 50 percent of the voting stock of another corporation(s), provide the following for each corporation so owned. Attach additional pages if needed.

Name of corporation:

Address:

City, State, ZIP Code:

Percent of stock owned: |

% |

Date stock acquired: |

/ |

/ |

|

|

|

|

|

|

|

mm/dd/yyyy

4If more than 50 percent of the voting stock of this corporation is owned by another corporation, provide the following information about the other corporation.

Name of corporation:

Address:

City, State, ZIP Code:

Percent of stock owned: |

% |

|

|

|

|

5Check here if this corporation or its subsidiary(ies) had a change in control or ownership or acquired control or ownership of any other legal entity this year.

6Enter the location where the corporate books and records are maintained:

7Enter the state or country of commercial domicile:

• 8 Enter the |

/ |

/ |

|

|

|

mm/dd/yyyy

Under separate cover, send a summary and supporting schedules for all federal adjustments and the federal tax liability for each year for which federal audit adjustments have not been reported to the Tax Commission. Include the date of final determination. Send the information to:

Auditing Division, Utah State Tax Commission, 210 North 1950 West, Salt Lake City, UT

•9 Enter the

/ / |

/ / |

/ / |

/ / |

|||

|

|

|

|

|

|

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

•10 Enter the

/ / |

/ / |

/ / |

/ / |

|||

|

|

|

|

|

|

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

Note: Utah Code

|

|

Schedule A - Utah Net Taxable Income and Tax Calculation |

Pg. 1 |

||||||||||

20203 |

EIN |

|

|

|

|

|

|

2022 |

|

|

|

||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

|

||||

1 |

Unadjusted income/loss before NOL and special deductions from federal form 1120, line 28 |

• 1 |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

2 |

Additions to unadjusted income from Schedule B, line 19 |

|

|

• 2 |

|

|

|

||||||

3 |

Add line 1 and line 2 |

|

|

3 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

4 |

Subtractions from unadjusted income from Schedule C, line 21 |

|

|

• 4 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

5 |

Adjusted income/loss - subtract line 4 from line 3 |

|

|

• 5 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

6 |

Utah net nonbusiness income from Schedule H, line 14 |

|

|

• 6 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

7 |

|

|

• 7 |

|

|

|

|||||||

8 |

Total nonbusiness income net of expenses - add line 6 and line 7 |

|

|

8 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

||||||

9 |

Apportionable income/loss before contributions deduction - subtract line 8 from line 5 |

• 9 |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

10 |

Utah contributions deduction from Schedule D, line 6 |

|

|

• 10 |

|

|

|

||||||

11 |

Apportionable income/loss - subtract line 10 from line 9 |

|

|

11 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

12 |

Apportionment fraction - enter 1.000000, or Schedule J, line 9 or 10, if applicable |

12 |

|

|

|

|

|||||||

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|||||

13 |

Apportioned income/loss - multiply line 11 by line 12 |

|

|

• 13 |

|

|

|

||||||

14 |

Utah net nonbusiness income (from line 6 above) |

|

|

14 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

15 |

Utah income/loss before Utah net loss deduction - add line 13 and line 14 |

|

|

• 15 |

|

|

|

||||||

|

|

|

|

|

|

|

|

||||||

16 |

Utah net loss carried forward from prior years (see instructions and attach documentation) |

• 16 |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

17 |

Net Utah taxable income/loss - subtract line 16 from line 15 |

|

|

• 17 |

|

|

|

||||||

18 |

Calculation of tax (see instructions): |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||||||

|

a Multiply line 17 by 4.85% (.0485) (not less than zero) |

18a |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

|

b Minimum tax - enter $100 or amount from Schedule M, line b |

• 18b |

|

|

|

|

|

||||||

|

Tax amount - enter the greater of line 18a or line 18b |

|

|

• 18 |

|

|

|

||||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

19 |

Interest on installment sales |

|

|

• 19 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

20 |

IRC 965(a) deferred foreign income installment amount |

|

|

• 20 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

21 |

Recapture of |

|

|

• 21 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

22 |

Total tax - add lines 18 through 21 |

|

|

• 22 |

|

|

|

||||||

|

Carry to Schedule A, page 2, line 23 |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||

|

Schedule A - Utah Net Taxable Income and Tax Calculation |

Pg. 2 |

|||||||||||||||

20204 EIN |

|

|

|

|

|

|

|

|

|

|

2022 |

|

|

||||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

23 |

Enter tax from Schedule A, page 1, line 22 |

|

|

|

|

|

23 |

|

|

|

|||||||

24 |

Nonrefundable credits (see instructions or incometax.utah.gov/credits for codes) |

|

|

|

|

||||||||||||

|

|

|

|

||||||||||||||

|

|

|

Code |

Amount |

|

Code |

Amount |

|

|

|

|

||||||

|

• 24a |

|

|

|

|

• 24b |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• 24c |

|

|

|

|

• 24d |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• 24e |

|

|

|

|

• 24f |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Total nonrefundable credits - add lines 24a through 24f |

|

|

|

|

|

• 24 |

|

|

||||||||

|

|

|

|

|

|

||||||||||||

25 |

Net tax - subtract line 24 from line 23 (cannot be less than line 18b or less than zero) |

• 25 |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

26 |

Utah use tax |

|

|

|

|

|

|

|

|

|

• 26 |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

27 |

Total tax - add line 25 and line 26 |

|

|

|

|

|

• 27 |

|

|

||||||||

|

Enter here and on |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||||||||

28 |

Refundable credits (see instructions or incometax.utah.gov/credits for codes) |

|

|

|

|

|

|||||||||||

|

|

|

Code |

Amount |

|

Code |

Amount |

|

|

|

|

||||||

|

• 28a |

|

|

|

|

• 28b |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• 28c |

|

|

|

|

• 28d |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Total refundable credits - add lines 28a through 28d |

|

|

|

|

|

• 28 |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

29 |

Prepayments from Schedule E, line 4 |

|

|

|

|

|

• 29 |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

30 |

Amended return only (see instructions) |

|

|

|

|

|

• 30 |

|

|

||||||||

|

|

|

|

|

|

|

|||||||||||

31 |

Total refundable credits and prepayments - add lines 28 through 30 |

|

• 31 |

|

|

||||||||||||

|

Enter here and on |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

Schedule B - Additions to Unadjusted Income |

|||||||

20205 |

EIN |

|

|

2022 |

|

||||

USTC ORIGINAL FORM |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

1 |

Interest from state obligations |

• 1 |

|||||||

|

|

|

|

|

|

|

|||

2 |

a Income taxes paid to any state |

• 2a |

|||||||

|

|

|

|

|

|||||

|

b Franchise or privilege taxes paid to any state |

• 2b |

|||||||

|

|

|

|

|

|||||

|

c Corporate stock taxes paid to any state |

• 2c |

|||||||

|

|

|

|

|

|||||

|

d Any income, franchise or capital stock taxes imposed by a foreign country |

• 2d |

|||||||

|

|

|

|

|

|||||

|

e Business and occupation taxes paid to any state |

• 2e |

|||||||

|

|

|

|

|

|||||

3 |

Safe harbor lease adjustments |

• 3 |

|||||||

|

|

|

|

|

|||||

4 |

Capital loss carryover |

• 4 |

|||||||

|

|

|

|

|

|||||

5 |

Federal deductions taken previously on a Utah return |

• 5 |

|||||||

|

|

|

|

|

|||||

6 |

Federal charitable contributions from federal form 1120, line 19 |

• 6 |

|||||||

|

|

|

|

|

|||||

7 |

Gain/loss on IRC Sections 338(h)(10) or 336(e) |

• 7 |

|||||||

|

|

|

|

|

|||||

8 |

Adjustments due to basis difference |

• 8 |

|||||||

|

|

|

|

|

|||||

9 |

Expenses attributable to 50 percent unitary foreign dividend exclusion |

• 9 |

|||||||

|

|

|

|

|

|||||

10 |

Installment sales income previously reported for federal but not Utah purposes |

• 10 |

|||||||

|

|

|

|

|

|||||

11 |

Nonqualified withdrawal from my529 |

• 11 |

|||||||

|

|

|

|

|

|||||

12 |

Income/loss from IRC Section 936 corporations |

• 12 |

|||||||

|

|

|

|

|

|||||

13 |

Foreign income/loss for worldwide combined filers |

• 13 |

|||||||

|

|

|

|

|

|||||

14 |

Income/loss of unitary corporations not included in federal consolidated return |

• 14 |

|||||||

|

|

|

|

|

|||||

15 |

Deductions for a royalty or other expense paid to an entity related by common ownership (see instructions) |

• 15 |

|||||||

|

|

|

|

|

|||||

16 |

Payroll Protection Program grant or loan addback (see instructions) |

• 16 |

|||||||

|

|

|

|

|

|||||

17 |

(Reserved, see instructions) |

• 17 |

|||||||

|

|

|

|

|

|||||

18 |

(Reserved, see instructions) |

• 18 |

|||||||

|

|

|

|

|

|||||

19 |

Total additions - add lines 1 through 18 |

• 19 |

|||||||

|

Enter here and on Schedule A, line 2 |

|

|

|

|||||

|

|

|

|

||||||

Schedule C - Subtractions from Unadjusted Income

20206 EIN

USTC ORIGINAL FORM

1Intercompany dividend elimination (see instructions)

2 Foreign dividend

3 Net capital loss

4a Federal jobs credit salary reduction

b Federal research and development credit expense reduction

c Federal orphan drug credit clinical testing expense reduction

d Expense reduction for other federal credits (attach schedule)

e.Federal qualified tax credit bond credit, income increase

f.Federal qualified zone academy bond credit, income increase

5 Safe harbor lease adjustments

6 Federal income previously taxed by Utah

7 Fifty percent exclusion for dividends from unitary foreign subsidiaries

8 Fifty percent exclusion for foreign operating company income/loss

9Gain/loss on stock sale not recognized for federal purposes (but included in taxable income) when IRC Section 338(h)(10) or 336(e) has been elected

10Basis adjustments

11Interest expense not deducted on federal return under IRC Section 265(b) or 291(e)

12Dividends received from admitted insurance company subsidiaries exempt under UC

13Contributions to my529 account(s)

14(Reserved, see instructions)

15Dividends received or deemed received by a member of the unitary group from a captive REIT

16IRC Section 857(b)(2)(E) deduction from a captive REIT

17FDIC Premiums disallowed as a deduction for federal income tax purposes

18

19(Reserved, see instructions)

20(Reserved, see instructions)

21Total subtractions - add lines 1 through 20

Enter here and on Schedule A, line 4

•1

•2

•3

•4a

•4b

•4c

•4d

•4e

•4f

•5

•6

•7

•8

•9

•10

•11

•12

•13

•14

•15

•16

•17

•18

•19

•20

•21

|

Schedule D - Utah Contributions Deduction |

|

|

||||||

20207 EIN |

|

|

2022 |

|

|

||||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|||

1 |

Apportionable income before contributions deduction from Schedule A, line 9 |

|

|

• 1 |

|||||

|

If a loss, no contribution deduction is allowed |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

2 |

Utah contribution limitation - multiply line 1 by 10% (.10) (not less than zero) |

2 |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

3 |

Current year contributions |

|

|

• 3 |

|||||

|

|

|

|

|

|

|

|

||

4 |

Utah contributions carryforward (attach schedule) |

|

|

• 4 |

|||||

5 |

Total contributions available - add line 3 and line 4 |

5 |

|

|

|

||||

|

|

|

|||||||

|

|

|

|

|

|

|

|

||

6 |

Utah contributions deduction - lesser of line 2 or line 5 |

|

|

• 6 |

|||||

|

Enter here and on Schedule A, line 10 |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

7 |

Contribution carryover to next year - subtract line 6 from line 5 |

• 7 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

Schedule E - Prepayments of Any Type |

|

||||

1 |

Overpayment applied from prior year |

|

|

1 |

|

|

2 |

Extension prepayment |

Date: |

/ / |

Check no.: |

2 |

|

|

||||||

Enter the date and amount of any extension prepayment. If paid by check, enter the check number.

3Other prepayments (attach additional pages if necessary)

Enter the date and amount of any prepayment for the filing period. If paid by check, enter the check number.

a Date: |

/ |

/ |

Check no.: |

|

3a |

|

|

|

|

|

|

b Date: |

/ |

/ |

Check no.: |

|

3b |

|

|

|

|

|

|

c Date: |

/ |

/ |

Check no.: |

|

3c |

|

|

|

|

|

|

d Date: |

/ |

/ |

Check no.: |

|

3d |

|

|

|

|

|

|

Total of all prepayments - add lines 3a through 3d |

3 |

4 Total prepayments - add lines 1 through 3 |

4 |

Enter here and on Schedule A, line 29 |

|

Schedule H - Utah Nonbusiness Income Net of Expenses |

Pg. 1 |

|||||

20261 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Failure to complete this form may result in disallowance of the nonbusiness income. |

|

|

|

|

|||||||

Part 1 - Utah Nonbusiness Income (nonbusiness income allocated to Utah) |

|

|

|

|

|||||||

|

|

|

|

||||||||

|

|

|

|

||||||||

|

A |

B |

|

|

C |

D |

|

E |

|||

|

Type of Utah |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

Utah Nonbusiness Income |

||||

|

Nonbusiness Income |

Utah Nonbusiness |

|

Used to Produce Utah |

Used to Produce Utah |

|

|

|

|||

|

|

|

Asset(s) |

|

|

Nonbusiness Income |

Nonbusiness Income |

|

|

|

|

1a |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1b |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1c |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1d |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1e |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

2Total of column C and column D

3Total Utah nonbusiness income - add column E for lines 1a through 1e

|

Description of direct expenses related to: |

Amount of Direct Expense |

||

4a |

Line 1a above |

|

||

|

|

|

|

|

4b |

Line 1b above |

|

||

|

|

|

|

|

4c |

Line 1c above |

|

||

|

|

|

|

|

4d |

Line 1d above |

|

||

|

|

|

|

|

4e |

Line 1e above |

|

||

|

|

|

|

|

5Total direct related expenses - add lines 4a through 4e

6 |

Utah nonbusiness income net of direct related expenses - subtract line 5 from line 3 |

|

• |

||

|

|

Column A |

Column B |

||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

||

|

Utah Nonbusiness Income |

Utah Nonbusiness Income |

|

|

|

7 |

|

|

|

|

|

|

(enter in Column A the amount from line 2, col. C) |

|

|

|

|

|

|

|

|

|

|

8

(enter in Column A the amount from line 2, col. D)

9Sum of beginning and ending asset values (add line 7 and line 8)

10Average asset value - divide line 9 by 2

11Utah nonbusiness assets ratio - line 10, Column A, divided by line 10, Column B (to four decimal places)

12Interest expense deducted in computing Utah taxable income (see instructions)

13Indirect related expenses for Utah nonbusiness income - multiply line 11 by line 12

14 Total Utah nonbusiness income net of expenses - subtract line 13 from line 6 |

|

• |

|

Enter on: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule H - |

Pg. 2 |

|||||

20262 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Part 2 -

|

A |

B |

|

|

C |

D |

|

E |

||

|

Type of |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

||||

|

Nonbusiness Income |

|

|

Used to Produce |

Used to Produce |

|

Income |

|||

|

|

|

Nonbusiness Asset(s) |

|

Nonbusiness Income |

Nonbusiness Income |

|

|

||

15a |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15b |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15c |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15d |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15e |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

16Total of column C and column D

17Total

|

Description of direct expenses related to: |

|

|

|

|

|

Amount of Direct Expense |

|

18a |

Line 15a above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18b |

Line 15b above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18c |

Line 15c above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18d |

Line 15d above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18e |

Line 15e above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 |

Total direct related expenses - add lines 18a through 18e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

20 |

• |

|||||||

|

|

|

Column A |

Column B |

|

|

||

|

|

|

|

|

||||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

|

|

|||

|

|

|

|

|

||||

21 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. C) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

22 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. D) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

23Sum of beginning and ending asset values (add line 21 and line 22)

24Average asset value - divide line 23 by 2

25

26Interest expense deducted in computing

27Indirect related expenses for

28 Total |

• |

|

Enter on: |

|

|

|

|

|

|

|

|

Schedule J - Apportionment Schedule |

Pg. 1 |

|||||

20263 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Use this schedule only if the entity does business in Utah and one or more other states and income must be apportioned to Utah.

Briefly describe the nature and location(s) of your Utah business activities:

Apportionable Income Factors

|

|

|

|

|

Column A |

|

Column B |

|||

1 |

Property Factor |

|

|

Inside Utah |

|

Inside and Outside Utah |

||||

|

a |

Land |

• 1a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

b |

Depreciable assets |

• 1b |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Inventory and supplies |

• 1c |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Rented property |

• 1d |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Other allowable property (see instructions) |

• 1e |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

f |

Total tangible property - add lines 1a through 1e |

• 1f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

2 |

Property factor - divide line 1f, Column A, by line 1f, Column B (to six decimal places) |

• |

2 |

|

|

|

||||

3 |

Payroll Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total wages, salaries, commissions and other compensation |

• 3a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

4 |

Payroll factor - divide line 3a, Column A, by line 3a, Column B (to six decimal places) |

• |

4 |

|

|

|

||||

5 |

Sales Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total sales (gross receipts less returns and allowances) |

|

|

|

• |

5a |

|||

|

b |

Sales delivered or shipped to Utah buyers from outside Utah |

• 5b |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Sales delivered or shipped to Utah buyers from within Utah |

• 5c |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Sales shipped from Utah to the United States government |

• 5d |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Sales shipped from Utah to buyers in states where the corp. |

• 5e |

|

|

|

|

|

||

|

|

has no nexus (corporation not taxable in buyer’s state) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f |

Rent and royalty income |

• 5f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

g |

Services and other allowable sales (see instructions) |

• 5g |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

h |

Total sales (add lines 5a through 5g) |

• 5h |

• |

|

|

|

|

||

|

|

|

|

|

|

|

||||

6 Sales factor - line 5h, Column A, divided by line 5h, Column B (to six decimals) |

• |

6 |

|

|

|

|||||

|

|

Continued on page 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form Breakdown

| Fact Name | Description |

|---|---|

| Type of Form | Utah Corporation 2020 Franchise and Income Tax Return TC-20 |

| Applicable Year | For calendar year 2020 or fiscal year starting and ending on specified dates |

| Amended Return Option | Provides option to mark the return as amended with a code 1-4 |

| Important Sections | Includes sections for incorporation details, federal consolidations, water’s edge election, financial institutions, ultimate U.S. parent information, and tax calculations |

| Governing Law | Adheres to various sections of the Utah Code, including UC §59-7-402(2) for water’s edge election and related to specific income tax rules |

| Special Features | Allows marking for specific situations like filing federal form 8886, making elections under IRC Sections, and adjustments for financial institutions |

Detailed Steps for Writing Utah Tc 20

Filling out the Utah TC-20 form is a necessary step for Utah corporations to comply with state tax requirements. This process, while detailed, can be simplified by following a systematic approach. Here, you will find instructions broken down into manageable steps. This guide aims to help you accurately complete the form, ensuring all relevant information is properly reported. Let's proceed with these steps to make sure the Utah TC-20 form is filled out correctly.

- Start by entering the corporation name and the Utah Corporation 2020 Franchise and Income Tax Return TC-20 at the top of the form.

- Enter the choice of calendar year 2020 or the applicable fiscal year dates.

- If filing an amended return, mark the appropriate “X” box and select the correct code (1-4).

- Mark “X” if the federal form 8886 was filed.

- Provide the corporation’s address, Employer Identification Number (EIN), city, state, ZIP + 4, and if applicable, the foreign country.

- Enter the Utah Incorporation/Qualification No. and the corporation’s telephone number.

- For corporations that conducted any Utah business activity during the taxable year, enter “X” in box 1.

- If the corporation joined in a federal consolidated return, enter “X” in box 2.

- Mark “X” to indicate if the return constitutes a “water’s edge” election under “worldwide return”, and select the appropriate option (3a, 3b, or 3c).

- If an election was made for any member of the federal affiliated group during the taxable year, enter “X” and specify the IRC Section (4a, 4b, or 4c).

- If the return includes any financial institution as defined by Tax Commission Rule R865-6F-32, enter “X” in box 5.

- Enter the Ultimate U.S. parent’s name and EIN in box 6.

- Calculate and enter the Total tax on line 7.

- Enter the Total refundable credits and prepayments on line 8.

- Subtract line 8 from line 7 to figure out the Tax Due and enter that amount on line 9.

- Calculate any penalties and interest and enter the total on line 10.

- Add lines 9 and 10 to calculate the Total Due and enter this on line 11.

- For overpayments, subtract the sum of line 7 and line 10 from line 8 and enter the result on line 12.

- Specify the amount of overpayment to be applied to the next taxable year on line 13.

- To determine the refund, subtract line 13 from line 12 and enter the result on line 14.

- Mark “X” for each quarterly estimated prepayment made.

- Under penalties of perjury, an officer of the corporation must sign and date the return.

- Provide the preparer’s information, including signature, date, telephone number, PTIN, firm’s name, and address.

After the form is completed and all information is reviewed for accuracy, it should be filed with the Utah State Tax Commission by the due date. Ensure to attach any required documentation, such as schedules or proof of payment for estimated taxes. Timely submission will help avoid potential penalties and interest due to late filing.

Common Questions

- What is the Utah TC-20 form?

The Utah TC-20 form is a document that corporations must complete for their Franchise and Income Tax Return in Utah. It is used for the calendar year 2020 or for a fiscal year that begins and ends on specified dates. It captures various details regarding the corporation’s activities, tax calculations, and any payments or refunds related to state income tax for corporations.

- Who needs to file the Utah TC-20 form?

Any corporation that has conducted business activity in Utah during the taxable year is required to file the Utah TC-20 form. This includes corporations that are incorporated in Utah, conduct business or earn income in Utah, or are registered to do business in Utah.

- How does a corporation indicate if it has filed a federal consolidated return on the TC-20 form?

Corporations that have joined in a federal consolidated return should mark the designated box on the TC-20 form. This information is important as it affects how the corporation’s income and deductions are reported for Utah tax purposes.

- What is the “water's edge” election, and how is it indicated on the form?

The “water's edge” election is a filing option that limits the income and apportionment calculation to the United States boundaries for certain corporations. Corporations making this election or involved in a combined report under these specifications should mark the appropriate box on the TC-20 form. The election affects how income is calculated and taxed by the State of Utah.

- Are there specific sections for financial institutions on the TC-20 form?

Yes, financial institutions defined by Tax Commission Rule R865-6F-32 have a specific section on the TC-20 form. These institutions must mark the indicated box if their return includes any financial institution as defined by Utah law.

- How is the total tax calculated on the TC-20 form?

Total tax is calculated by entering the amount from Schedule A, line 27. This involves calculating Utah net taxable income, applying the appropriate tax rate, and then adding any additional taxes owed or subtracting any applicable credits to arrive at the total tax due.

- What information is required about the ultimate U.S. parent on the TC-20 form?

Corporations must provide the name and Employer Identification Number (EIN) of their ultimate U.S. parent company. This information helps the state tax authorities understand the corporate structure and its tax implications.

- How are penalties and interest handled on the TC-20 form?

Corporations should calculate and enter any penalties and interest due to late filing or payment on line 10. Detailed instructions for calculating these amounts are provided in the form's instructions to ensure accuracy.

- What if a corporation needs to amend a previously filed TC-20 form?

To amend a previously filed TC-20 form, corporations should mark the “Amended Return” box at the top of the form and enter the correct information. Specific codes (1-4) are provided to indicate the nature of the amendment. The form then guides the corporation through adjusting previously reported figures to reflect the correct information.

Common mistakes

One of the first mistakes to avoid involves incorrect or incomplete identification information. Each corporation must accurately provide its name, address, Employer Identification Number (EIN), Utah Incorporation/Qualification Number, and other basic information as requested on the form. The importance of this step cannot be overstated, as it ensures the company's return is accurately attributed to its tax account. Accurate identification helps prevent miscommunication and processing delays that could arise from incorrect or missing information.

Another area where errors commonly occur is in the section dealing with the tax calculation, specifically Schedule A. Corporations often make mistakes by improperly calculating additions and subtractions from income, which are critical to determining the adjusted income. To accurately complete this section, it's necessary to attentively go through Schedules B and C, ensuring that all required adjustments to the unadjusted income are correctly accounted for and transferred to Schedule A. This involves a careful assessment of interest from state obligations, income taxes paid to any state, and adjustments due to differences in basis among various other considerations.

Electing consolidated or combined reporting options without understanding their implications is another mistake. The TC-20 form allows for different types of reporting, including "water's edge" election under "worldwide," "combined report," and others. Making these elections affects how income and tax responsibilities are calculated. It's important for corporations to fully understand each option's impact and make informed decisions to ensure compliance and optimize tax obligations. This requires meticulous review of the corporation's structure, operations, and relevant tax laws.

Last but not least, inaccuracies in reporting tax credits, prepayments, and estimated tax payments can significantly affect the tax due or refund owed. Schedule A and the related sections require detailed information about refundable and nonrefundable credits, prepayments, and any amendments. Corporations sometimes overlook applicable credits or inaccurately report prepayments, leading to incorrect calculation of the total tax liability. Attention to detail in these areas can result in substantial savings and prevent the underpayment or overpayment of taxes.

- Ensure accurate and complete reporting of identification information.

- Accurately calculate adjustments to income using Schedules B and C to determine adjusted income on Schedule A.

- Make informed decisions regarding consolidated or combined reporting options, understanding their implications.

- Report tax credits, prepayments, and estimated tax payments accurately to avoid errors in tax calculation.

By avoiding these common mistakes, corporations can improve the accuracy of their TC-20 form submissions, helping to facilitate a smoother tax filing process and potentially saving time and resources by reducing the likelihood of complications with the Utah State Tax Commission.

Documents used along the form

Filing taxes can often feel like assembling a puzzle, with the Utah TC-20 form serving as a central piece for corporations. This form, specifically designed for 2020, plays a crucial role in reporting franchise and income tax returns for entities operating within the state. However, just like any major tax filing, the TC-20 doesn't stand alone. To ensure a comprehensive and compliant submission, several additional documents and forms often accompany it. Let's shed some light on these vital pieces of the tax filing puzzle.

- Schedule A (Utah Net Taxable Income and Tax Calculation): This schedule directly complements the TC-20 by detailing the calculation of a corporation's taxable income and the tax due, highlighting adjustments to income, deductions, and credits.

- Schedule B (Additions to Unadjusted Income): Offers a breakdown of certain incomes or expenses that need to be added back to the unadjusted gross income. This could include state tax payments or certain federal deductions that Utah doesn't recognize for state tax purposes.

- Schedule H (Nonbusiness and Apportionable Income): Schedule H differentiates between nonbusiness income that should be taxed solely to Utah versus income that should be apportioned across multiple states based on a formula that accounts for the corporation's business activities in Utah.

- Form TC-559 (Corporation/Partnership Payment Coupon): This form is used when making payments for the corporation tax due. It ensures that payments are correctly credited to the company's account.

- Federal Form 1120 (U.S. Corporation Income Tax Return): Although not a state form, the Federal Form 1120 is critical as it provides the foundation for several numbers and calculations on the TC-20. Details like total income, deductions, and credits start here and are adjusted per Utah's tax law to determine state tax liabilities.

Navigating the tax landscape requires a careful approach, particularly when dealing with corporate taxes. Each form, from TC-20 to its accompanying schedules and documents, plays an integral role in painting a complete picture of a corporation's fiscal responsibilities. Leveraging these documents effectively ensures compliance, maximizes deductions and credits, and ultimately positions a business for financial success in the state of Utah. Whether you're a tax professional or a business owner, understanding these components is the first step towards a smooth and successful filing process.

Similar forms

The Utah TC-20 form, designed for corporate franchise and income tax returns, shares characteristics with several other documents across various jurisdictions and purposes. Notably, its parallels extend to procedures, informational requirements, and purposes with documents such as the Internal Revenue Service (IRS) Form 1120. Form 1120 is the U.S. Corporation Income Tax Return, where corporations report their income, gains, losses, deductions, and credits to the federal government. Like the TC-20, Form 1120 requires detailed financial information and calculations to determine the tax liability, including adjustments, deductions, and credits relevant to corporate entities.

Similarly, the California Form 100, the Corporation Franchise or Income Tax Return, mirrors the TC-20 in its purpose to report income, deductions, and credits for corporations operating within the state. Both forms demand comprehensive financial data to accurately assess state tax obligations based on business activities, and they provide spaces for adjustments specific to respective state tax codes.

Another analogous document is the New York State Corporation Tax Return (Form CT-3), which also requires corporations to provide detailed information about income, deductions, and tax liability. The structure and informational requirements of Form CT-3 closely resemble those of the Utah TC-20, reflecting the universal need among states to collect comprehensive tax data from corporate entities.

The Texas Franchise Tax Report shares a similar objective with the Utah TC-20, albeit with notable differences due to Texas’s unique tax structure. While Texas does not impose a traditional income tax on corporations, its franchise tax report requires detailed revenue reporting and calculation of the tax based on margins or revenue, paralleling the requirement on the TC-20 for comprehensive financial reporting.

On a more specific note, the Utah TC-20 shares similarities with Schedule D of the IRS Form 1120, which is used for reporting capital gains and losses. Both documents require detailed transactional information and offer a mechanism to adjust taxable income based on gains or losses, demonstrating their role in refining corporate tax liability.

The IRS Form 8886, Reportable Transaction Disclosure Statement, also bears resemblance to an aspect of the Utah TC-20 concerning the disclosure of certain transactions. Corporations filing the TC-20 must indicate if they’ve filed Form 8886, underlining the interconnectedness of federal and state reporting requirements for transactions that could affect tax calculations.

Another state-specific document, the Illinois Form IL-1120, Illinois Corporation Income and Replacement Tax Return, similarly requires corporations to report income, losses, and deductions to calculate state tax liability, mirroring the TC-20’s objectives to ensure accurate state tax contributions from corporate entities.

The Arizona Form 120, the corporate income tax return, requires detailed reporting of income, deductions, and tax liability calculations, akin to the TC-20. Both forms serve as a critical tool for states to assess and collect the appropriate corporate taxes, ensuring compliance with state-specific tax laws and regulations.

The Pennsylvania Corporate Tax Report (RCT-101) is yet another example of a state-level corporate tax return form that shares a purpose with the Utah TC-20. This document requires similar comprehensive financial disclosures to ascertain tax obligations under Pennsylvania laws, reflecting a widespread requirement for detailed corporate tax reporting across the states.

Finally, the Multistate Tax Commission (MTC) Form, used for combined or consolidated reporting by corporations operating in multiple jurisdictions, resonates with the Utah TC-20's provisions for water’s edge or worldwide combined reporting. These forms facilitate a standardized approach to reporting and calculating corporate taxes when business operations span beyond a single state boundary, ensuring equitable tax obligations across multiple jurisdictions.

Dos and Don'ts

When it comes to navigating through the intricacies of the Utah TC-20 form, understanding what to do and what not to do is crucial for ensuring the process is both accurate and efficient. Below are some insights to guide you through this process:

Do's:

- Review the entire form before you start: Ensure you understand each section. This preliminary step can minimize errors and save time in the long run.

- Gather all necessary documents: Before beginning to fill out the form, make sure you have all the relevant financial statements, tax documents, and any federally filed forms at hand. This includes keeping a record of any state obligations interest or income and taxes paid to other states or foreign countries.

- Be meticulously accurate: Double-check all the data you enter, especially numbers and financial information. Even a minor mistake can lead to discrepancies that may result in penalties or delays.

- Sign and date the form: The TC-20 form requires a signature and date from an authorized officer of the corporation and the tax preparer, if applicable. This action certifies that the information provided is accurate and complete to the best of their knowledge.

Don'ts:

- Don’t overlook the “Amended Return” box: If you are filing an amendment to a previously filed return, it’s critical to mark the “Amended Return” box and to specify the code related to your amendment reason.

- Avoid guessing on financial information: Estimates can lead to inaccuracies in your tax calculation and may trigger an audit. If exact numbers aren’t immediately available, take the time to obtain the accurate figures before submitting.

- Don’t forget to include attachments: Certain sections of the form require additional documentation, such as details on federal adjustments, basis differences, and any income subject to non-Utah taxation. Failing to include these attachments can result in an incomplete return.

- Do not ignore deadlines: Timeliness is key in avoiding penalties and interest. Be sure to submit the TC-20 form and any owed taxes by the due date, keeping in mind that extensions for filing may not extend the period for paying taxes due.

Accurately completing and submitting the Utah TC-20 form is not just a legal requirement but also a testament to the responsible management of corporate obligations. By adhering to these guidelines, businesses can ensure compliance and contribute to their ongoing success.

Misconceptions

When it comes to understanding the Utah TC-20 form, it's clear that there's a lot of confusion out there. Let's clear up some common misconceptions:

Only Utah-based corporations need to file a TC-20 form. This isn't quite right. Any corporation that conducts business in Utah during the taxable year, regardless of where it is based, needs to file this form. It's about business activity in Utah, not just about being located there.

If you file a federal consolidated return, you cannot file a TC-20 form. This is another misunderstanding. Indeed, corporations that are part of a federal consolidated tax return are still required to file a TC-20 if they conducted business in Utah.

A “water's edge” election is the default filing status. Actually, the “water’s edge” election is just one option available to corporations, and it must be actively chosen. This method is not automatically applied.

Marking an “X” for quarterly estimated payments is optional. This overlooks the requirement for companies that meet certain criteria to make quarterly estimated tax payments. If these payments apply to you, marking “X” for each relevant quarter is mandatory.

The section on ultimate U.S. parent’s information is only for multinational corporations. Not quite. Any corporation that has a parent company needs to fill this out, regardless of whether the parent company or the filing corporation itself operates globally or solely within the United States.

Penalties and interest apply only if you owe taxes. This misconception could lead you to ignore potential penalties and interest. These fees can also apply for filing late or failing to pay estimated taxes on time, among other reasons, even if you do not owe additional taxes at year's end.

Understanding these truths can demystify the process and obligations related to the TC-20 form. Keep in mind, when in doubt, seeking guidance from a professional or the Utah State Tax Commission directly can provide clarity specific to your situation.

Key takeaways

Understanding the Utah TC-20 form is crucial for corporations to accurately report their income and franchise taxes. Here are key takeaways to help navigate through the filing process:

- The TC-20 form is intended for corporations operating within Utah, requiring them to report their franchise and income tax returns for a specific calendar year or fiscal year.

- If a corporation has conducted any business activity in Utah during the taxable year, it must be clearly indicated on the form.

- Corporations that are part of a federal consolidated return must disclose this by marking the appropriate section on the TC-20.

- Electing the "water’s edge" election affects how income and apportionment are reported and should be selected accordingly if applicable.

- Including financial institutions as defined by the Tax Commission Rule R865-6F-32 in the return requires indication, due to different tax considerations.

- Details such as the ultimate U.S. parent’s name and Employer Identification Number (EIN) are essential for completing the TC-20 accurately.

- Calculating tax involves specific schedules, such as Schedule A for Utah Net Taxable Income and Tax Calculation, which must be filled out comprehensively.

- Understanding and properly applying for credits and deductions, including safe harbor adjustments and federal charitable contributions, can impact the total tax due significantly.

Completing the Utah TC-20 form carefully can help ensure compliance with state tax regulations and possibly optimize a corporation’s tax liabilities. Particular attention should be given to sections that require detailed financial information, election choices, or that pertain to specific types of corporations, such as financial institutions.

Common PDF Templates

Utah Estimated Tax Payments - TC-559’s design for easy detachment and submission makes it user-friendly for Utah businesses managing tax payments.

Utah Cpe Requirements - Avoid penalties or license lapses by using this form to confirm your compliance with CPE requirements in an orderly manner.

Utah Car Sales Tax - Utah’s tax credit for clean fuel vehicles is an opportunity for eco-conscious taxpayers.