Blank Utah Tc 116 Form

The Utah TC-116 form serves a vital role for entities eligible for fuel tax refunds within the state. Designed by the Utah State Tax Commission, this form allows various entities, including government departments, non-profit agricultural organizations, and Native American tribes, among others, to apply for a refund on fuel taxes they've paid. The comprehensive nature of the TC-116 form captures information on tax-paid gallons of varied fuel types such as motor, undyed diesel, aviation fuel, and compressed natural gas. Entities can claim refunds for fuel used in specific conditions that include fuel exported out of Utah, gallons lost due to accidents or other calamities, and substantial single transactions discharged due to bankruptcy. Additionally, the form outlines the process for calculating the total refund amount, taking into account both the Utah excise tax and the Utah Environmental Assurance Fee. It also includes provisions for fuels delivered to the non-Utah portion of the Navajo Nation, ensuring a broad spectrum of purposes and entities are covered. Through meticulous documentation, such as purchase invoices and the amount of fuel bought or lost, applicants are guided through a structured process to claim their respective refunds, underlining the TC-116’s crucial role in the state’s tax refund system.

Form Preview Example

11601

9998

Utah State Tax Commission

Utah Application for

Fuel Tax Refund

Rev. 9/10

|

|

Name |

|

|

|

Mark “X” if this is |

|

|

|

|

|

a new address: |

|

|

|

|

|

|

|

Address |

|

|

|

_____ |

Physical |

|

|

|

|

|

address |

City |

State |

ZIP code |

|

|

|

||||

_____ |

Mailing |

|

|

|

|

|

address |

Foreign country (if not U.S.) |

Telephone number |

||

|

|

||||

Utah Excise Tax |

|

A - Motor fuel |

B - Undyed diesel |

||

1.Utah

2.Utah

3.Utah

FEIN/SSN

FEIN/SSN

_____ Mark "X" if this is a SSN

Tax period (mmddyyyy) |

|

From |

To |

C - Aviation fuel |

D - CNG |

4.Utah

5.Total eligible gallons of fuel lost or destroyed by

fire, flood, crime & accident (from Schedule type 1E)

6.Total eligible gallons for each single transaction of 4,500 or more discharged in bankruptcy (from Schedule type 1F)

7.Gallons returned to refinery for

8.Total

9.Total

10.Tax per gallons of aviation fuel at 2.5 cents

(multiply line 9 column C by .025)

11.Total

12.Tax per gallons of aviation fuel at 4 cents (multiply line 11 column C by .04)

13.Total

14.Tax per gallons of aviation fuel at 9 cents (multiply line 13 column C by .09)

15.Tax rates

16.Calculated

00

00

.245

00

00

00

00

.245

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

.085

00

00

11602

17. Total Utah exise tax (add line 16, columns A, B, C, and D) |

17 |

00 |

|

||

Utah Environmental Assurance Fee |

|

|

18. Utah Environmental Assurance Fee paid gallons |

18 |

|

exported from Utah (from Schedule type 2A) |

|

|

|

|

|

19. Utah Environmental Assurance Fee paid gallons placed |

19 |

|

in nonparticipating tanks (from Schedule type 2B) |

|

|

|

|

|

20. Utah Environmental Assurance Fee paid gallons for |

20 |

|

repackaged oil (from Schedule type 2C) |

|

|

|

21 |

|

21. Total Utah Environmental Assurance Fee paid gallons (add lines 18 through 20)

22.005

22. Tax rate

|

|

|

|

23 |

00 |

23. Calculated Environmental Assurance Fee (multiply line 21 by line 22) |

|

|

|||

|

|

A - Motor fuel |

|

B - Undyed diesel fuel |

|

|

|

65 |

|

160 |

|

Navajo Nation Refund |

|

|

|

|

|

24. Total taxable gallons reported to the Navajo Nation |

24 |

|

|

|

|

|

|

|

|

|

|

25. Gallons delivered to |

25 |

|

|

|

|

|

|

|

|

|

|

26. Total gallons subject to Utah fuel tax |

26 |

|

|

|

|

(subtract line 25 from line 24) |

|

|

|

|

|

27. Navajo 0.5% credit, if taken on Navajo Distributor |

27 |

|

|

|

|

Tax Return (multiply line 26 by .005) |

|

|

|

|

|

28. Net taxable gallons available for Utah fuel refund |

28 |

|

|

|

|

(subtract line 27 from line 26) |

|

|

|

|

|

29. Tax rate |

29 |

.18 |

|

.245 |

|

|

|

|

|

|

|

30. Navajo Nation fuel tax refund |

30 |

|

00 |

|

00 |

(multiply line 28 by line 29) |

|

|

|

||

|

|

|

|

31 |

00 |

31 Total Navajo Nation (add line 30, columns A and B) |

|

|

|

|

|

|

|

|

|

32 |

00 |

32. Total refund (add lines 17, 23, and 31) |

|

|

|

|

|

I certify that I meet all the conditions to qualify for this refund, I have examined this refund application, including any accompanying schedules, and certify that to the best of my knowledge it is true, correct and complete.

Print name of applicant

Applicant’s signature

|

|

|

11603 |

|

Utah Refund Application General Schedule |

|

|

|

|

|

|

|

||||||||||||||

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Company name |

|

|

|

|

|

|

|

|

FEIN/SSN |

Schedule type |

Product type |

Month/Year |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

From |

|

|

To |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule type |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Product type |

|

|

|

||||||

1A |

- Utah |

|

1H |

- Gallons of aviation fuel collected at 2.5 cent tax rate |

|

065 |

- Motor fuel |

228 - Diesel fuel (dyed) |

||||||||||||||||||

1B |

- Utah |

|

1I - |

Gallons of aviation fuel collected at 4 cent tax rate |

|

130 |

- Aviation fuel |

260 - Repackaged lube oil |

||||||||||||||||||

1C |

- Utah |

|

1J - Gallons of aviation fuel collected at 9 cent tax rate |

|

160 |

- Diesel fuel (undyed) |

|

|

|

|||||||||||||||||

1D |

- Utah |

2A |

- Utah Environmental Assurance Fee paid gallons exported from Utah |

224 |

- Compressed natural gas |

|

|

|

||||||||||||||||||

1E - Eligible gallons of fuel lost or destroyed by fire, flood, crime or accident |

2B |

- Utah Environmental Assurance Fee paid gallons placed in nonparticipating tanks |

|

|

|

|

|

|

|

|||||||||||||||||

1F - Eligible gallons for each single transaction discharged by bankruptcy |

2C |

- Utah Environmental Assurance Fee for repackaged |

|

|

|

|

|

|

|

|

||||||||||||||||

1G - Gallons returned to refinery for |

|

3A - Gallons of fuel delivered to Utah portion of Navajo Nation |

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

1 |

2 |

|

|

|

3 |

|

|

4 |

5 |

6 |

|

7 |

|

|

8 |

9 |

||||||||

|

|

Purchase date |

|

Invoice |

Manifest |

|

|

|

|

|

|

Facility/Terminal number |

Airport code |

|

|

Supplier’s |

|

|

||||||||

|

|

|

(mmddyyyy) |

|

number |

number |

|

|

Origin |

|

Destination |

|

(only for Sch. type 2A, 2B, 2C) |

(for prod. type 130) |

name |

|

|

gallons |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total

Form Breakdown

| Fact | Detail |

|---|---|

| Form Identification | The form used for applying for a fuel tax refund in Utah is identified as TC-116. |

| Revision Date | The TC-116 form was last revised in September 2010. |

| Purpose | It is designed to facilitate the process for entities to claim refunds for Utah tax-paid gallons of fuel in various categories, including motor fuel, undyed diesel, and aviation fuel. |

| Eligible Claimants | Government entities, the Ute Indian Tribe, non-profit agricultural entities, entities experiencing losses due to fire, flood, crime, or accident, and transactions discharged in bankruptcy are among those eligible to apply for refunds. |

| Governing Laws | The refunds and the application process are governed by Utah state laws pertaining to excise tax and environmental assurance fees. |

Detailed Steps for Writing Utah Tc 116

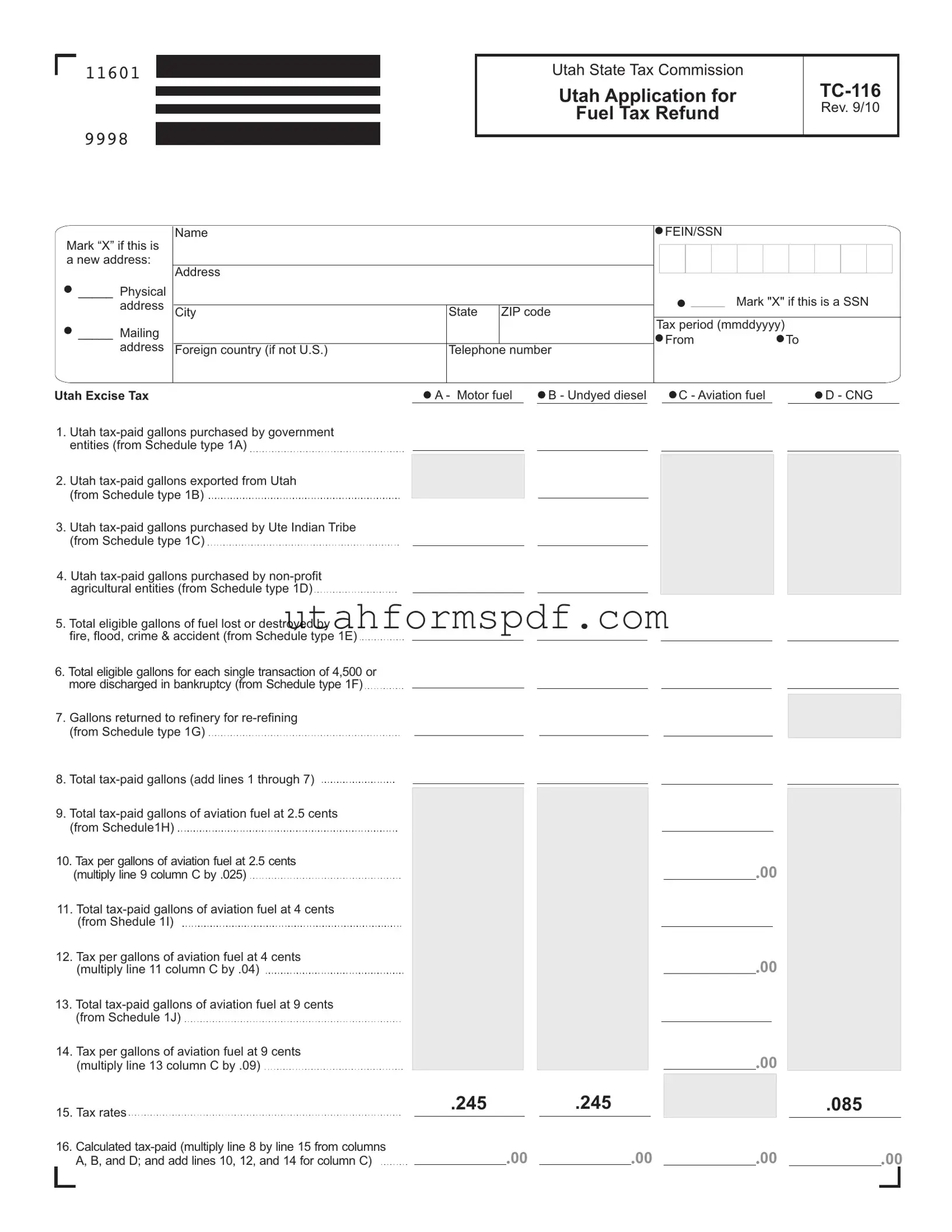

The Utah TC 116 form is a comprehensive document used for the application of fuel tax refunds in Utah. It covers various categories, including motor fuel, undyed diesel, aviation fuel, and CNG, among others. To ensure accuracy and compliance, individuals or entities seeking a refund must carefully provide specifics related to tax-paid gallons under different scenarios and tax rates applied. After completing the form, the applicant asserts their eligibility for the refund through a statement of truth and completeness signed at the end of the document.

- Start by entering the applicant's name in the designated field at the top of the form.

- If the address has changed since a previous application, mark the “X” box. Otherwise, proceed to fill in the current address, including physical and mailing addresses if they are different. Indicate the city, state, ZIP code, and if applicable, the foreign country.

- Provide the telephone number in the field provided.

- Enter the Federal Employer Identification Number (FEIN) or Social Security Number (SSN) in the appropriate field. Mark the “X” box if using a SSN.

- Specify the tax period by entering the start and end dates (mmddyyyy format).

- For each type of fuel, enter the Utah tax-paid gallons purchased in the applicable sections (lines 1-7) as guided by the form. This includes gallons purchased by various entities, exported from Utah, lost, destroyed, or returned for re-refining.

- Calculate the total tax-paid gallons by adding lines 1 through 7 and enter the sum on line 8.

- For aviation fuel, determine the applicable tax per gallons as specified in the instructions for lines 9 through 14 and enter the amounts accordingly.

- Calculate the calculated tax-paid amount by multiplying the total tax-paid gallons by the tax rate provided for each fuel type (line 16).

- Add the calculated tax-paid amounts across all fuel types and enter this total on line 17 as the total Utah excise tax.

- Complete the Utah Environmental Assurance Fee section, including the gallons exported, placed in nonparticipating tanks, and repackaged (lines 18 through 21).

- Enter the tax rate and calculate the Environmental Assurance Fee (line 23).

- For applicants eligible for the Navajo Nation refund, fill in the required information regarding taxable gallons and calculate the refund amount (lines 24 through 30).

- Add all refunds to determine the total refund amount (line 32).

- Conclude the application by certifying the information. Print the applicant's name, provide the applicant’s signature, and date the form to affirm the accuracy and completeness of the application.

Upon completion, it is imperative that all relevant schedules and supporting documentation are attached to the TC 116 form. This ensures a thorough review process by the Utah State Tax Commission, fostering a favorable outcome for the applicant. Verifying the details and ensuring the precision of all entered information cannot be overstressed, as this directly impacts the refund process.

Common Questions

What is the purpose of the Utah TC-116 Form?

The Utah Application for Fuel Tax Refund, known as TC-116 Form, serves to request a refund of fuel taxes paid in Utah under specific conditions. This includes fuel purchased by government entities, exported from Utah, bought by the Ute Indian Tribe, by non-profit agricultural entities, fuel lost or destroyed by fire, flood, crime, or accident, among others. It's designed to ensure eligible applicants can recover taxes for fuel not used as intended or accounted for within the state's regulatory framework.

Who is eligible to file the TC-116 Form?

Eligibility to file the TC-116 Form includes government entities, the Ute Indian Tribe, non-profit agricultural entities, and other parties who have purchased fuel for specific uses that entitle them to a tax refund. Additionally, individuals or entities that have experienced losses due to disaster or crime, or those who have had significant fuel discharged in bankruptcy, may also qualify.

How is the refund calculated on the TC-116 Form?

The refund is calculated by identifying the total tax-paid gallons of various fuels, including motor fuel, undyed diesel, aviation fuel, and compressed natural gas (CNG), among others. The form requires applicants to add up eligible gallons from different schedules and categories, then multiply these by the specific tax rate applicable to each fuel type. This calculation includes deductions for losses and credits, such as the Navajo Nation credit. The total refund amounts from these calculations give the final refund claimed.

What supporting documents are required when submitting the Utah TC-116 Form?

When submitting the TC-116 Form, you must include supporting documentation that verifies the claims made. This includes purchase invoices, export documentation, proof of loss or destruction, evidence of eligibility for government entities, the Ute Indian Tribe, and non-profit agricultural entities, among others. Accurate and complete documentation is crucial for the application to be processed successfully.

How and where do you submit the TC-116 Form?

The completed TC-116 Form, along with all required documentation, should be submitted to the Utah State Tax Commission. It can be filed electronically through the state's official tax website or mailed to the commission's designated address. Ensure that you have signed the form and provided accurate contact information to facilitate any communication regarding your application.

What is the deadline for filing the TC-116 Form?

The deadline for filing the TC-116 Form varies based on the tax period in question and the specific refund claim. Generally, claimants must submit their applications within a statutory timeframe from the date of fuel purchase or loss/event qualifying for the refund. Applicants should refer to the instructions provided with the form or consult the Utah State Tax Commission for specific deadlines applicable to their situation to ensure timely submission.

Common mistakes

Filling out the Utah TC-116 form, which is used to apply for a fuel tax refund, can be a complicated process. To ensure that individuals and organizations maximize their refund potential, it's crucial to steer clear of common mistakes. Here are four common errors:

- Incorrect or Incomplete Information: Individuals often overlook the importance of providing complete and accurate information. Every field, including the applicant's name, address (both physical and mailing, if applicable), and telephone number, must be filled out correctly. Moreover, marking whether it's a new address or not is a step frequently missed. Inaccurate or missing information can lead to delays or even the denial of the application.

- Errors in Financial Data: The calculation of tax-paid gallons, whether it's motor fuel, undyed diesel, aviation fuel, or CNG, requires meticulous attention to detail. Mistakes made in listing the gallons purchased, exported, or lost can significantly impact the refund amount. It's imperative to accurately add up lines 1 through 7 for the total tax-paid gallons and ensure that the tax rates applied are correct according to the fuel type.

- Failing to Properly Identify the Type of Fuel: Each fuel type, including motor fuel, undyed diesel, aviation fuel, and CNG, has different tax rates and refund policies. Sometimes, applicants might mistakenly report gallons under the wrong fuel category. For instance, categorizing aviation fuel gallons under motor fuel can lead to incorrect refund calculations.

- Omission of Required Schedules: The Utah TC-116 form requires supplementary schedules for specific types of refunds, such as gallons exported from Utah or gallons purchased by government entities. Not attaching these required schedules, or incorrectly filling them out, can result in an incomplete application. Each eligible transaction type, like fuel lost or destroyed by fire, flood, crime, or accident, or gallons returned to the refinery for re-refining, must be documented on the right schedule.

Submitting an incomplete or incorrect Utah TC-116 form can delay the processing time and affect the refund amount. Careful review and adherence to the provided instructions can help avoid these common mistakes. It's beneficial to double-check all financial calculations and ensure that all required documents and schedules are attached before submission. For further clarification, consulting the detailed instruction manual or seeking professional advice is recommended.

Documents used along the form

When managing the intricacies of Utah's fuel tax system, the TC-116 form serves as an essential tool for applying for a fuel tax refund. However, to ensure comprehensive and compliant processing, it often requires the support of additional forms and documents. These additional items play pivotal roles in clarifying, substantiating, and providing context to the information submitted through the TC-116 form.

- TC-116A Utah Refund Application General Schedule: This form complements the TC-116 by providing detailed schedules related to various types of tax-paid gallons eligible for refund. It helps to further specify the nature of the claimants’ refund request, breaking down the gallons by purpose such as government entity usage, exports out of Utah, agricultural use, etc.

- Schedule 1 - Proof of Payment Documents: To support a TC-116 filing, claimants must provide evidence of the taxes paid on the fuel for which they are seeking a refund. These documents can include invoices, receipts, or other purchase records that clearly show the payment of Utah fuel excise taxes.

- Schedule 2 - Loss Reports: For fuel lost or destroyed due to fire, flood, crime, or accident, claimants need to attach a detailed report or documentation proving the loss. This could involve police reports, insurance claims, or other official documents that verify the circumstances and amount of fuel lost.

- Navajo Nation Fuel Tax Agreement Forms: If a refund claim involves fuel transactions with the Navajo Nation, relevant forms and documentation must be included to demonstrate eligibility under the specific tax agreement and applicable credits between Utah and the Navajo Nation. This specificity ensures compliance with the special tax considerations afforded to these transactions.

In navigating Utah's fuel tax refund process, understanding and compiling the requisite forms and documents is crucial. Each document serves a unique purpose, from detailing the nature of the refund claim to providing the necessary evidence to support it. Properly leveraging these tools not only streamulates the refund claim process but also aligns with the state's commitment to fiscal responsibility and regulatory compliance. Thus, knowledge and thoughtful preparation in this context can significantly enhance the efficiency and outcomes of tax refund endeavors.

Similar forms

The Utah TC-116 form, designed for fuel tax refund applications, shares similarities with various other tax-related documents. Each document, while serving a unique purpose, incorporates comparable elements such as detailed personal or entity information, tax calculations, and specific eligibility criteria.

One document that bears resemblance to the TC-116 form is the IRS Form 8849, Schedule 1, "Claim for Refund of Excise Taxes." Both forms are used to claim refunds on taxes previously paid, though the IRS form covers a broader range of excise taxes. Like the TC-116, Form 8849 requires detailed information about the claimant and a specific calculation of the refund being requested, ensuring that only eligible amounts are claimed.

The IRS Form 720, "Quarterly Federal Excise Tax Return," is another document with similarities. This form is used for reporting and paying excise taxes, a process opposite to claiming a refund, yet it shares the requirement for detailed tax calculations and reporting specific tax incidents, just as the TC-116 form does for fuel tax refunds. Both forms are integral in the management and reconciliation of excise taxes.

A state-specific equivalent, such as the California BOE-770-DV, "Diesel Fuel Claim for Refund on Nontaxable Uses," also mirrors the TC-116 in purpose and structure. It targets a specific fuel tax scenario, focusing on diesel fuel, and requires detailed accounting of fuel purchases and uses that qualify for refunds, closely paralleling the structured detail seen in Utah's refund application.

The Federal Highway Administration's Form FHWA-556, "Statement of Materials and Labor Used by Contractors on Highway Construction Involving Federal Funds," is somewhat analogous. Although not a tax form, it necess (requires) the detailed reporting of materials (including fuel) used on federally funded projects. The emphasis on precise reporting and eligibility criteria links this form to the procedural specificity of TC-116.

Another document, the "Uniform Motor Fuel Refund Claim," commonly used in various U.S. jurisdictions for fuel tax refund requests by commercial carriers, shares the regimented structure and detailed accounting found in the TC-116 form. These documents facilitate refunds for specific eligible activities, demanding comprehensive documentation of fuel purchases and utilization.

The IRS Form 4136, "Credit for Federal Tax Paid on Fuels," is akin to the TC-116, as it allows taxpayers to claim a credit or refund for certain fuel taxes paid. While Form 4136 applies these credits against income tax, the focus on meticulously documented fuel transactions and tax calculations is a shared characteristic with the Utah form.

State rebate forms for alternative fuel vehicles or fueling infrastructure also share common ground with the TC-116 form. They typically require applicants to provide detailed information about the vehicle or infrastructure, proof of eligibility, and specific tax-related information, parallel to the detailed reporting and eligibility criteria of the TC-116.

Lastly, sales and use tax exemption certificates, like those used by tax-exempt entities when purchasing fuel, indirectly relate to the TC-116's purpose and structure. By providing detailed information about the tax-exempt status and nature of the fuel use, these certificates prevent tax charges upfront, similarly to how the TC-116 form is used to claim refunds after tax payment.

Overall, while each document serves a distinct purpose within the tax system, ranging from claiming refunds to reporting taxable transactions, they all emphasize the need for accurate, detailed reporting and strict adherence to eligibility criteria. This commonality underscores the complex interplay of regulations governing tax liabilities and refunds across various jurisdictions and tax types.

Dos and Don'ts

When filling out the Utah TC-116 form, which is designed to apply for a fuel tax refund, there are several dos and don'ts that can help ensure the process goes smoothly. Being attentive to these can save time and help avoid mistakes that could potentially delay your refund.

Do:

- Review the entire form first: Before you start, take a moment to read through the entire document to understand what information you need to gather.

- Gather all required documents: Make sure you have all the necessary documents, such as purchase invoices and proof of payment for the fuel tax, before you begin.

- Use black or blue ink: Fill out the form using black or blue ink to ensure that it is legible and can be scanned or photocopied without issues.

- Double-check your math: Errors in calculations can lead to delays in processing your refund, so take the time to verify your math.

- Provide complete information: Answer every question and fill out every field. If a section doesn't apply to you, indicate with "N/A" (not applicable) to show that you didn't overlook it.

- Sign and date the form: Your signature and the date are required to process the form. Ensure these fields are not left blank.

Don't:

- Omit your contact information: Make sure to provide your full address, telephone number, and email if available. This ensures that the Tax Commission can reach you if there are questions or issues.

- Use pencil or non-standard colors: Filling out the form in pencil or colors other than black or blue can make it difficult to read and may lead to processing errors.

- Guess on dates or amounts: Be accurate with the dates of fuel purchases and the amounts. Estimates can cause discrepancies that delay your refund.

- Forget to mark the tax type: Clearly indicate whether you are claiming a refund for motor fuel, undyed diesel, aviation fuel, CNG, or other fuel types by marking the correct box.

- Leave sections incomplete: If you leave sections incomplete, it may appear as if you missed them, causing unnecessary delays.

- Ignore the instructions: Each section has specific instructions. Failing to follow them can result in mistakes that slow down the refund process.

Misconceptions

Understanding the Utah TC-116 form, which deals with applications for fuel tax refunds, is crucial but can be complicated due to widespread misconceptions. Here’s a breakdown of common misunderstandings:

Misconception 1: The TC-116 form is only for businesses.

Actually, while businesses frequently use it, government entities and non-profit agricultural organizations can also apply for fuel tax refunds using this form.Misconception 2: You can claim a refund for any fuel purchase.

In truth, the form is designed for specific situations, such as fuel bought by government entities, exported from Utah, or lost due to disasters.Misconception 3: It's only applicable for gasoline purchases.

The form covers various types of fuel, including diesel, aviation fuel, and compressed natural gas (CNG), not just gasoline.Misconception 4: Personal vehicle fuel expenses are reimbursable.

Refunds generally do not cover personal vehicle fuel expenses unless they meet very specific criteria laid out in the form.Misconception 5: The process is quick and doesn’t require documentation.

Filing for a refund demands detailed records, including the purchase date, invoice numbers, and amounts of fuel, among other details. The process also involves a review period.Misconception 6: Only Utah residents can file the form.

Entities located outside of Utah but conducting eligible fuel transactions within the state can indeed file for a refund.Misconception 7: Refunds are calculated at a flat rate for all types of fuel.

The refund rate varies depending on the type of fuel and the circumstances of the purchase or loss.Misconception 8: You cannot claim a refund for fuel lost due to theft or accidents.

Contrary to this belief, such losses are eligible under specific conditions outlined in the form, like fuel lost or destroyed by crime, accident, fire, or flood.Misconception 9: The TC-116 form also covers fuel tax credits.

While it does deal with refunds, tax credits are a separate matter and generally require different forms.Misconception 10: All sections of the form must be filled out by all applicants.

Different parts of the form apply to different entities and situations, so not all sections will be relevant to every applicant.

Understanding these points clears up a lot of confusion and makes navigating the process of applying for a fuel tax refund via the Utah TC-116 form much smoother.

Key takeaways

- The Utah TC-116 form is used to apply for a fuel tax refund by various entities, including government bodies, the Ute Indian Tribe, non-profit agricultural operations, and those who have experienced fuel loss due to disaster or accident.

- Applicants must mark an "X" if there has been a change of address, ensuring the Utah State Tax Commission has current contact information.

- The form requires detailed information about tax-paid gallons of various fuel types, including motor fuel, undyed diesel, aviation fuel, and compressed natural gas (CNG), necessitating accurate record-keeping to complete.

- There are specific categories for reporting fuel, such as fuel exported from Utah, fuel purchased by eligible entities, and gallons lost or destroyed, each requiring its own calculation.

- Applicants must calculate the total tax-paid gallons and the corresponding refund amount by applying the correct tax rate for each fuel type, as detailed in the form instructions.

- In addition to the fuel tax refund, the form also addresses the Utah Environmental Assurance Fee, which applies to gallons exported from Utah, placed in nonparticipating tanks, or repackaged oil, highlighting the various facets of fuel use and taxation in Utah.

- The Navajo Nation Refund section provides a method to calculate refunds for fuel transactions related to the Navajo Nation, underscoring the specific consideration given to tribal lands in tax matters.

- Before submission, the applicant must certify the accuracy of the information provided on the form, making it essential to review all details thoroughly to ensure compliance with state tax laws.

- The form includes schedules for documenting specific transactions, like fuel purchased by government entities and aviation fuel tax rates, requiring detailed and organized record-keeping for proper tax reporting and refund application.

Common PDF Templates

What Is Odometer Rollback - This form is a declaration by the seller (transferor) regarding the actual mileage of a vehicle at the time of sale or transfer of ownership.

Utah State Tax Forms - The TC-895 form not only aids in reducing environmental pollution but also helps vehicle owners meet legal requirements efficiently.

Utah Tax Forms - Filing the TC-941D is a compliance requirement for businesses needing to reconcile their withholding tax discrepancies in Utah.