Blank Utah Tax Exemption Form

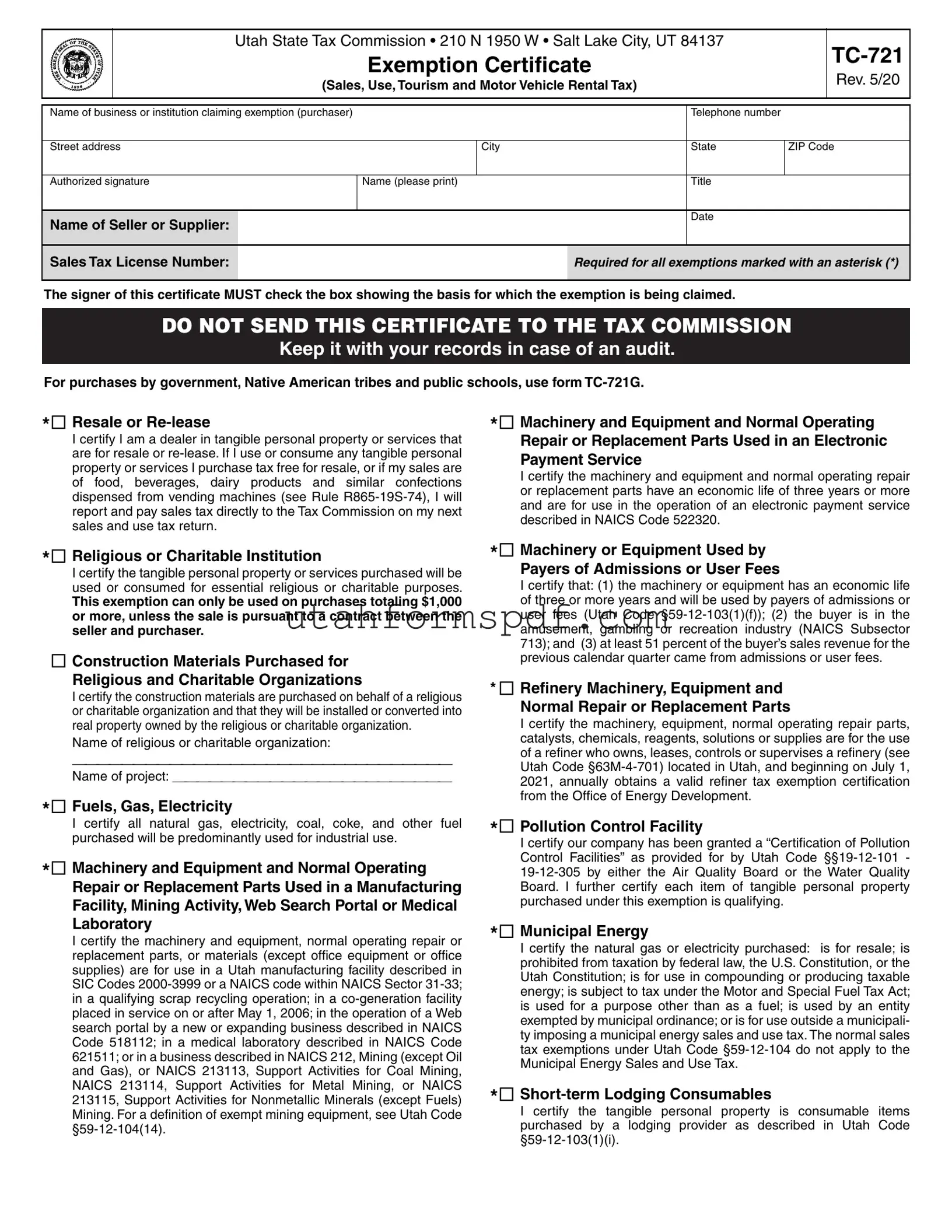

The Utah Tax Exemption form, officially known as the TC-721, serves as a critical document for businesses, institutions, and certain individuals seeking tax exemptions on purchases in the state of Utah. Issued by the Utah State Tax Commission, this comprehensive form encompasses a wide range of exemptions, covering sectors from sales and use, to tourism and motor vehicle rental tax. It is designed for entities claiming exemption on tangible personal property or services that are either resold, used in manufacturing, religious, charitable functions, or for several other specified purposes. The form mandates specifics like the business or institution's name, contact information, and an authorized signature to validate its claims. Additionally, it itemizes various exemption categories including machinery and equipment for manufacturing, items for resale, construction materials for religious and charitable organizations, and energy or fuel for industrial purposes, among others. Notably, the form underscores the buyer's responsibility to accurately check the box corresponding to the exemption being claimed and emphasizes the need to keep this certificate on file for audit purposes, rather than sending it to the Tax Commission. Through outlining prerequisites such as the sales tax license number for certain exemptions and delineating the correct usage of items under exemption claims, the TC-721 form is structured to ensure compliance with Utah's tax laws while facilitating tax relief for eligible purchases.

Form Preview Example

Utah State Tax Commission • 210 N 1950 W • Salt Lake City, UT 84137

Exemption Certificate

(Sales, Use, Tourism and Motor Vehicle Rental Tax)

Rev. 5/20

Name of business or institution claiming exemption (purchaser) |

|

|

|

Telephone number |

|

|

|

|

|

|

|

|

|

Street address |

|

City |

|

State |

ZIP Code |

|

|

|

|

|

|

|

|

Authorized signature |

Name (please print) |

|

|

Title |

|

|

|

|

|

|

|

|

|

Name of Seller or Supplier: |

|

|

|

|

Date |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sales Tax License Number: |

|

|

|

Required for all exemptions marked with an asterisk (*) |

||

|

|

|

|

|

|

|

The signer of this certificate MUST check the box showing the basis for which the exemption is being claimed.

DO NOT SEND THIS CERTIFICATE TO THE TAX COMMISSION

Keep it with your records in case of an audit.

For purchases by government, Native American tribes and public schools, use form

* Resale or

I certify I am a dealer in tangible personal property or services that are for resale or

* Religious or Charitable Institution

I certify the tangible personal property or services purchased will be used or consumed for essential religious or charitable purposes.

This exemption can only be used on purchases totaling $1,000 or more, unless the sale is pursuant to a contract between the seller and purchaser.

Construction Materials Purchased for

Religious and Charitable Organizations

I certify the construction materials are purchased on behalf of a religious or charitable organization and that they will be installed or converted into real property owned by the religious or charitable organization.

Name of religious or charitable organization:

________________________________

Name of project: _______________________

* Fuels, Gas, Electricity

I certify all natural gas, electricity, coal, coke, and other fuel purchased will be predominantly used for industrial use.

* Machinery and Equipment and Normal Operating Repair or Replacement Parts Used in a Manufacturing Facility, Mining Activity, Web Search Portal or Medical Laboratory

I certify the machinery and equipment, normal operating repair or replacement parts, or materials (except office equipment or office supplies) are for use in a Utah manufacturing facility described in SIC Codes

* Machinery and Equipment and Normal Operating Repair or Replacement Parts Used in an Electronic Payment Service

I certify the machinery and equipment and normal operating repair or replacement parts have an economic life of three years or more and are for use in the operation of an electronic payment service described in NAICS Code 522320.

* Machinery or Equipment Used by Payers of Admissions or User Fees

I certify that: (1) the machinery or equipment has an economic life of three or more years and will be used by payers of admissions or user fees (Utah Code

* Refinery Machinery, Equipment and Normal Repair or Replacement Parts

I certify the machinery, equipment, normal operating repair parts, catalysts, chemicals, reagents, solutions or supplies are for the use of a refiner who owns, leases, controls or supervises a refinery (see Utah Code

* Pollution Control Facility

I certify our company has been granted a “Certification of Pollution Control Facilities” as provided for by Utah Code

* Municipal Energy

I certify the natural gas or electricity purchased: is for resale; is prohibited from taxation by federal law, the U.S. Constitution, or the Utah Constitution; is for use in compounding or producing taxable energy; is subject to tax under the Motor and Special Fuel Tax Act; is used for a purpose other than as a fuel; is used by an entity exempted by municipal ordinance; or is for use outside a municipali- ty imposing a municipal energy sales and use tax. The normal sales tax exemptions under Utah Code

*

I certify the tangible personal property is consumable items purchased by a lodging provider as described in Utah Code

* Direct Mail

I certify I will report and pay the sales tax for direct mail purchases

on my next Utah SALES AND USE TAX RETURN.

* Commercial Airlines

I certify the food and beverages purchased are by a commercial airline for

* Commercials, Films, Audio and Video Tapes

I certify that purchases of commercials, films, prerecorded video tapes, prerecorded audio program tapes or records are for sale or distribution to motion picture exhibitors, or commercial television or radio broadcasters. If I subsequently resell items to any other customer, or use or consume any of these items, I will report any tax liability directly to the Tax Commission.

* Alternative Energy

I certify the tangible personal property meets the requirements of UC

* Locomotive Fuel

I certify this fuel will be used by a railroad in a locomotive engine. Starting Jan. 1, 2021, all locomotive fuel is subject to a 4.85% state tax.

* Research and Development of Alternative Energy Technology

I certify the tangible personal property purchased will be used in research and development of alternative energy technology.

* Life Science Research and Development Facility

I certify that: (1) the machinery, equipment and normal operating repair or replacement parts purchased have an economic life of three or more years for use in performing qualified research in Utah; or (2) construction materials purchased are for use in the construc- tion of a new or expanding life science research and development facility in Utah.

* Mailing Lists

I certify the printed mailing lists or electronic databases are used to send printed material that is delivered by U.S. mail or other delivery service to a mass audience where the cost of the printed material is not billed directly to the recipients.

* Semiconductor Fabricating, Processing or Research and Development Material

I certify the fabricating, processing, or research and development materials purchased are for use in research or development, manufac- turing, or fabricating of semiconductors.

* Telecommunications Equipment, Machinery or Software

I certify these purchases or leases of equipment, machinery, or software, by or on behalf of a telephone service provider, have a useful economic life of one or more years and will be used to enable or facilitate telecommunications; to provide 911 service; to maintain or repair telecommunications equipment; to switch or route telecommunications service; or for sending, receiving, or transport- ing telecommunications service.

* Aircraft Maintenance, Repair and Overhaul Provider

I certify these sales are to or by an aircraft maintenance, repair and overhaul provider for the use in the maintenance, repair, overhaul or refurbishment in Utah of a

* Ski Resort

I certify the

* Qualifying Data Center

I certify that the machinery, equipment or normal operating repair or replacement parts are: (1) used in a qualifying data center as defined in Utah Code

Leasebacks

I certify the tangible personal property leased satisfies the following conditions: (1) the property is part of a

(2) sales or use tax was paid on the initial purchase of the property; and, (3) the leased property will be capitalized and the lease payments will be accounted for as payments made under a financ- ing arrangement.

Film, Television, Radio

I certify that purchases, leases or rentals of machinery or equip- ment will be used by a motion picture or video production company for the production of media for commercial distribution.

Prosthetic Devices

I certify the prosthetic device(s) is prescribed by a licensed physician for human use to replace a missing body part, to prevent or correct a physical deformity, or support a weak body part. This is also exempt if purchased by a hospital or medical facility. (Sales of corrective eyeglasses and contact lenses are taxable.)

I certify this tangible personal property, of which I am taking posses- sion in Utah, will be taken

Agricultural Producer

I certify the items purchased will be used primarily and directly in a commercial farming operation and qualify for the Utah sales and use tax exemption. This exemption does not apply to vehicles required to be registered.

Tourism/Motor Vehicle Rental

I certify the motor vehicle being leased or rented will be temporarily used to replace a motor vehicle that is being repaired pursuant to a repair or an insurance agreement; the lease will exceed 30 days; the motor vehicle being leased or rented is registered for a gross laden weight of 12,001 pounds or more; or, the motor vehicle is being rented or leased as a personal household goods moving van. This exemption applies only to the tourism tax (up to 7 percent) and the

Textbooks for Higher Education

I certify that textbooks purchased are required for a higher education course, for which I am enrolled at an institution of higher education, and qualify for this exemption. An institution of higher education means: the University of Utah, Utah State University, Utah State University Eastern, Weber State University, Southern Utah Universi- ty, Snow College, Dixie State University, Utah Valley University, Salt Lake Community College, or the Utah System of Technical Colleges.

*Purchaser must provide sales tax license number in the header on page 1.

NOTE TO PURCHASER: You must notify the seller of cancellation, modification, or limitation of the exemption you have claimed. Questions? Email taxmaster@utah.gov, or call

Form Breakdown

| Fact Name | Detail |

|---|---|

| Form Title | Exemption Certificate (Sales, Use, Tourism and Motor Vehicle Rental Tax) |

| Form Number | TC-721 Rev. 5/20 |

| Issuing Body | Utah State Tax Commission |

| Submission Requirement | Do not send this certificate to the Tax Commission; keep it for your records in case of an audit. |

| Special Form for Certain Entities | For purchases by government, Native American tribes, and public schools, use form TC-721G. |

| Governing Laws | Varies by exemption type, including Utah Code §§59-12-104(14), 63M-4-701, 19-12-101 - 19-12-305, etc. |

Detailed Steps for Writing Utah Tax Exemption

Once you've determined your eligibility for a Utah Tax Exemption, filling out the form is the next crucial step in the process. This document is essential for businesses, institutions, and organizations that qualify for sales, use, tourism, and motor vehicle rental tax exemptions in the State of Utah. The information provided will establish your entitlement to these exemptions, so it's important to fill out the form accurately and retain it with your records for any future audits. Here are the easy-to-follow steps to complete your Utah Tax Exemption form:

- At the top of the form, enter the Name of business or institution claiming exemption (purchaser) along with its Telephone number.

- Underneath, fill in the Street address, City, State, and ZIP Code of the purchaser.

- In the section labeled Authorized signature, the person filling out the form should sign their name.

- Adjacent to the signature, print the signer's Name and record their Title within the company or institution.

- Specify the Name of Seller or Supplier from whom the purchases are made.

- Record the Date when the form is filled out.

- Enter the Sales Tax License Number in the designated area. This is mandatory for all exemptions that are marked with an asterisk (*) on the form.

- Choose the appropriate exemption box that applies to the basis of your claim by checking it. Each exemption category has specific requirements, so ensure the selection accurately reflects the purpose of your tax-exempt purchases.

- For specific exemptions that require additional details (e.g., religious or charitable institutions, construction materials purchased for religious or charitable organizations, etc.), provide the requested information on the form such as Name of religious or charitable organization or Name of project.

- After completing the form, remember not to send it to the Tax Commission. Instead, keep it filed with your records to have it handy in case of an audit.

It's essential to carefully review the exemptions and choose the one that accurately fits the nature of your purchases or activities. If at any time the exemption you have claimed changes, it's your responsibility to notify the seller of any cancellation, modification, or limitation to the exemption you have previously claimed. Accuracy and honesty in filling out this form will ensure that your exemption is valid and recognized by both the seller and the Utah State Tax Commission.

Common Questions

Who needs to file a Utah Tax Exemption form?

Businesses or institutions claiming exemption from sales, use, tourism, and motor vehicle rental tax in Utah need to file a Tax Exemption Certificate (TC-721). This includes entities such as dealers in tangible personal property or services for resale, religious or charitable institutions, manufacturers, agricultural producers, and others specified in the exemption categories.

What should be done with the Utah Tax Exemption Certificate after it's filled out?

Do not send the completed certificate to the Utah State Tax Commission. Instead, it should be kept with the purchaser’s records in case of an audit. It serves as evidence of the claim for tax exemption for transactions between the seller and purchaser.

Are there any exemptions specifically for construction materials?

Yes, construction materials purchased on behalf of a religious or charitable organization, which will be installed or converted into real property owned by such an organization, can be exempted. A specific section on the certificate needs to be completed to claim this exemption.

Can fuel purchases be exempt from tax?

Fuel purchases, including natural gas, electricity, coal, coke, and other fuels used predominantly for industrial purposes, may qualify for an exemption. The purchaser must certify that their use of these fuels meets the criteria for industrial usage.

How does a business claim an exemption for machinery and equipment used for manufacturing?

Businesses must certify that the machinery, equipment, and parts purchased are for use in a qualifying Utah manufacturing facility, mining activity, web search portal, or medical laboratory, among others. This indicates compliance with specific industry and usage codes provided in the TC-721 form.

What is the exemption for agricultural producers?

Agricultural producers can claim an exemption for items used primarily and directly in a commercial farming operation. This exemption does not apply to vehicles that are required to be registered.

Is there a tax exemption available for educational materials?

Yes, textbooks required for courses at institutions of higher education qualify for an exemption. The institution must be recognized within the Utah System of Higher Education, and the textbooks must be necessary for the enrolled courses.

What are the requirements for claiming the pollution control facility exemption?

Companies must have received a “Certification of Pollution Control Facilities” either from the Air Quality Board or the Water Quality Board of Utah. Additionally, they need to certify that each item of tangible personal property purchased under this exemption qualifies.

Can a business claim an exemption on purchases for resale?

Yes, businesses reselling or re-leasing tangible personal property or services can claim an exemption. They must certify that if they use any of these tax-free purchases for purposes other than resale, they will report and pay the sales tax due on their next tax return.

How does a lodging provider claim an exemption for short-term lodging consumables?

Lodging providers, as described under Utah Code §59-12-103(1)(i), can certify that tangible personal property purchased as consumable items for their lodging facilities qualifies for an exemption. This certification is part of the TC-721 form.

Common mistakes

Filling out Utah's Tax Exemption form, a critical document for businesses and organizations seeking sales, use, tourism, and motor vehicle rental tax exemptions, requires careful attention to detail. Unfortunately, mistakes can easily be made, potentially leading to delays, audits, and the payment of unanticipated taxes. Here are eight common errors:

- Incorrect Business Information: One of the most frequent oversights is providing incorrect or outdated business information. This includes the name of the business, address, and telephone number. Accuracy is essential, as this information is used to verify the entity's eligibility for the exemption.

- Failure to Provide Sales Tax License Number: Exemptions marked with an asterisk (*) require the purchaser's sales tax license number. Overlooking this requirement can result in the form being rejected since it's crucial for confirming the legitimacy of the business or institution claiming the exemption.

- Unchecked Exemption Boxes: Each exemption has a specific qualification criterion. Not checking the box that outlines the basis for claiming an exemption is a mistake that can lead to the assumption that no basis exists for the claim, rendering the application incomplete.

- Misunderstanding Exemption Categories: Selecting the wrong exemption category because of a misunderstanding of the terms or qualifications can lead you to claim an exemption for which your purchase doesn’t qualify, potentially causing compliance issues down the line.

- Omission of Authorized Signature: The form requires an authorized signature to certify the claim. Failing to sign the document is a common error that invalidates the submission. The signature is a testament to the accuracy and truthfulness of the information provided.

- Not Checking Eligibility for Exemptions: Not all purchases qualify for exemptions under the categories provided. A common mistake is assuming eligibility without checking the specific requirements listed under each exemption category, such as minimum purchase amounts or the nature of the goods purchased.

- Incorrect Date: An often overlooked detail is the date of the form. The form must have the current date to be considered valid. An incorrect date can cause delays or questioning of the document’s validity.

- Not Keeping Records: The instruction to not send the certificate to the Tax Commission but keep it for records is occasionally misinterpreted or ignored. Maintaining these documents is critical for audits. Failing to do so can lead to complications in proving exemption eligibility later on.

To ensure the best chance of your Tax Exemption form being accepted without issue, double-check each of these areas before submission. Attention to detail, clarity, and having a proper understanding of the form’s requirements will guide you through the process efficiently, allowing you to benefit from the intended tax exemptions.

Documents used along the form

When handling the Utah Tax Exemption form, several other documents and forms often complement its usage for various purposes, such as ensuring compliance, providing detailed information, or satisfying specific requirements of certain exemptions. Familiarizing oneself with these additional documents can streamline processes and aid in the more efficient handling of tax-related matters.

- TC-721G: Specifically designed for purchases made by government bodies, Native American tribes, and public schools, this form is used in lieu of the general tax exemption certificate when these entities are making exempt purchases.

- Articles of Incorporation or Organization: These documents provide proof of the legal existence and status of a religious or charitable organization, which is necessary for claiming exemptions on purchases for essential religious or charitable purposes.

- Energy Certification: For claiming exemptions on fuels, gas, and electricity predominantly used for industrial purposes, an official certification or statement that validates the primary use of these energies in qualifying activities is required.

- Commercial Lease Agreement: When claiming exemptions under the leaseback arrangement, a copy of the commercial lease agreement can be necessary to prove that the property is part of a sale-leaseback transaction and that sales or use tax was paid at the point of initial purchase.

- Manufacturer’s Statement or Invoice: This document is crucial when claiming exemptions for machinery and equipment used in manufacturing, mining, or qualifying activities, as it verifies the nature and use of the purchased items.

- Prescription for Prosthetic Devices: For purchases of prosthetic devices exempt from sales tax, a prescription from a licensed physician is required to verify that the device is necessary for the bearer, ensuring the purchase aligns with exemption qualifications.

In conclusion, the effective use of the Utah Tax Exemption form, along with these relevant additional documents, can significantly enhance the precision and legitimacy of tax exemption claims. Ensuring the proper documentation supports each claim not only facilitates smoother transactions but also helps in maintaining compliance with tax laws and regulations.

Similar forms

The Utah Sales and Use Tax Exemption Certificate is akin to the Resale Certificate used in various states. This document serves as a declaration by the purchaser that the goods being bought will be resold or leased in the normal course of business. Like the Utah exemption form, it allows businesses to purchase goods without paying sales tax at the point of sale, under the condition that the final product will be taxed when sold to the end consumer. Both certificates aim to avoid double taxation of goods by exempting sales for resale from sales tax.

Similarly, the Machinery and Equipment Exemption Certificate found in numerous states parallels this Utah document, particularly in sections that exempt machinery and equipment used in manufacturing, mining, or other qualifying operations. These certificates permit businesses to avoid sales tax on purchases of equipment that is essential for their operational processes. The underlying principle is to encourage economic activity and investment in capital-intensive sectors by reducing the upfront cost of purchasing new equipment.

The Exemption Certificate for Government Purchases, like the variant specifically for government entities, Native American tribes, and public schools mentioned in the Utah form, validates that goods or services purchased by governmental bodies are exempt from sales tax. This recognition stems from the principle that government entities should not be taxed by the state, as this would essentially be the government taxing itself, thereby reallocating rather than generating revenue.

Another document with similarities is the Charitable or Religious Organizations Sales Tax Exemption Certificate. This parallels the sections in the Utah certificate that exempt purchases made by religious or charitable institutions. Both documents recognize the non-profit nature of these organizations and their contributions to societal welfare, thereby exempting them from sales tax on purchases that support their exempt purposes.

The Direct Pay Permit is also related, allowing holders to buy goods and services tax-free and then self-assess and pay tax on their use of the goods and services directly to the taxing authority. Similar to the Utah form's provisions for direct payment on certain purchases like direct mail, this approach offers businesses the flexibility to manage tax liability directly, ensuring correct tax treatment for their operations.

The

Finally, the Construction Materials Exemption Certificate, akin to the Utah exemption for construction materials purchased for religious and charitable organizations, highlights the specificity in tax-exempt purchases for construction projects. By exempting these purchases, the certificates aim to support the construction and expansion of facilities that will be used for charitable, educational, or religious purposes, reflecting a recognition of their benefit to the public interest.

In essence, each of these documents, while serving a specific function or catering to a distinct sector, embodies the principle of incentivizing certain activities or behaviors through tax relief. By understanding the similarities and purposes behind these certificates, entities can navigate tax laws more efficiently and leverage exemptions to which they are entitled.

Dos and Don'ts

When completing the Utah Tax Exemption form, paying attention to detail and accuracy is crucial. Here are some key do's and don'ts to guide you through the process:

- Do ensure that the name of the business or institution claiming the exemption is accurately filled out. This should match the official records exactly.

- Do check the appropriate box indicating the basis for the exemption claim. Understanding the specific criteria for each exemption can help avoid misinterpretation or error.

- Do provide a clear and authorized signature. An unsigned form may be considered invalid and can lead to unnecessary delays.

- Do include a valid Sales Tax License Number where required. This is essential for exemptions that necessitate this detail.

- Do retain the certificate within your records rather than sending it to the Tax Commission. This will be important for audits or future reference.

- Do contact the listed emails or phone numbers provided at the bottom of the form if you have any questions. Clarification can prevent mistakes.

- Don't leave any required fields empty. Make sure all necessary information is provided before submitting the form.

- Don't check boxes that do not apply to your specific situation, as this can lead to incorrect processing or legal issues down the line.

- Don't forget to review the specific exemptions and understand the definitions provided in the Utah Code references. Incorrect classification could affect your exemption status.

- Don't use the form for purposes it's not intended for. For example, government, Native American tribes, and public schools should use form TC-721G instead.

- Don't ignore the requirement for certain exemptions that only apply to purchases totaling $1,000 or more. This detail is critical to qualify for some exemptions.

- Don't hesitate to provide updates to the seller regarding any cancellation, modification, or limitation of the exemption you have claimed as noted in the reminder at the bottom of the form.

Misconceptions

Understanding the Utah Tax Exemption form can sometimes be challenging. It's essential to clear up common misconceptions to ensure accurate and lawful completion of the document. Here are five common misunderstandings:

- Any business can use the TC-721 form for exemptions: This form is specifically designed for certain types of organizations and purposes, such as government entities, religious or charitable institutions, and businesses purchasing for resale. Not all businesses qualify for exemptions.

- The form grants an automatic exemption: Simply completing the form does not grant exemption. The purchasing entity must meet specific criteria, and the form must accurately reflect the basis for exemption. Misuse or inaccuracies can result in penalties.

- Exemptions apply to all purchases: Some businesses mistakenly believe once they fill out the form, all their purchases are exempt from tax. However, exemptions are specific to the type of goods or services bought and their intended use. For example, machinery used in manufacturing might be exempt, while office supplies are not.

- Sending the form to the Tax Commission: The instruction "DO NOT SEND THIS CERTIFICATE TO THE TAX COMMISSION" is clear. You're required to keep the form for your records and present it during an audit, not send it to the Tax Commission upon completion.

- No need for detailed records: Some may wrongly assume that completing this form negates the need for keeping detailed records of exempt purchases. In reality, maintaining comprehensive records is crucial for substantiating your exemptions in case of an audit.

It's crucial for businesses and institutions claiming tax exemptions through the Utah TC-721 form to understand these points. Misconceptions can lead to unintended misuse of the form, resulting in penalties or disqualification of exemptions. Always ensure your eligibility and use the exemption accurately to comply with Utah tax laws.p>

Key takeaways

Understanding the Utah Tax Exemption form is crucial for businesses and institutions operating within the state to ensure compliance with tax laws and to take advantage of exemptions for which they qualify. Below are key takeaways to navigate the complexities of this form:

- The Utah Tax Exemption form (TC-721 Rev. 5/20) is intended for use by businesses or institutions claiming tax exemptions on purchases related to sales, use, tourism, and motor vehicle rental tax.

- Entities such as government organizations, Native American tribes, and public schools are directed to use a specific form, the TC-721G, indicating a tailored approach to different types of exempt organizations.

- It's important that the form is not directly sent to the Utah State Tax Commission but instead retained among the purchaser's records for audit purposes, emphasizing the need for accurate record-keeping.

- Exemptions are varied and include, but are not limited to, purchases for resale, materials bought on behalf of religious or charitable organizations, machinery and equipment used in certain industries, and items used for pollution control, indicating a broad scope of tax relief opportunities.

- Certain exemptions require the purchaser to provide a sales tax license number, highlighting the need for businesses to be registered for sales tax where applicable.

- The purchaser must communicate any cancellation, modification, or limitation of the exemption claimed with the seller, stressing the importance of maintaining transparent and up-to-date transaction records.

- For specific questions, the form directs users to contact the Utah State Tax Commission through email or phone, offering a channel for clarification and ensuring compliance.

This form serves as a vital tool for eligible organizations to manage their tax obligations effectively, underscoring the importance of understanding and accurately applying for exemptions.

Common PDF Templates

Utah State Tax Form for Employees - With the TC-194 form, Utah residents have an accessible means to personalize their vehicles, contributing to the state's unique cultural mosaic.

Utah Estimated Tax Payments - The detachable coupon design of the TC-559 form simplifies the payment process for taxpayers.