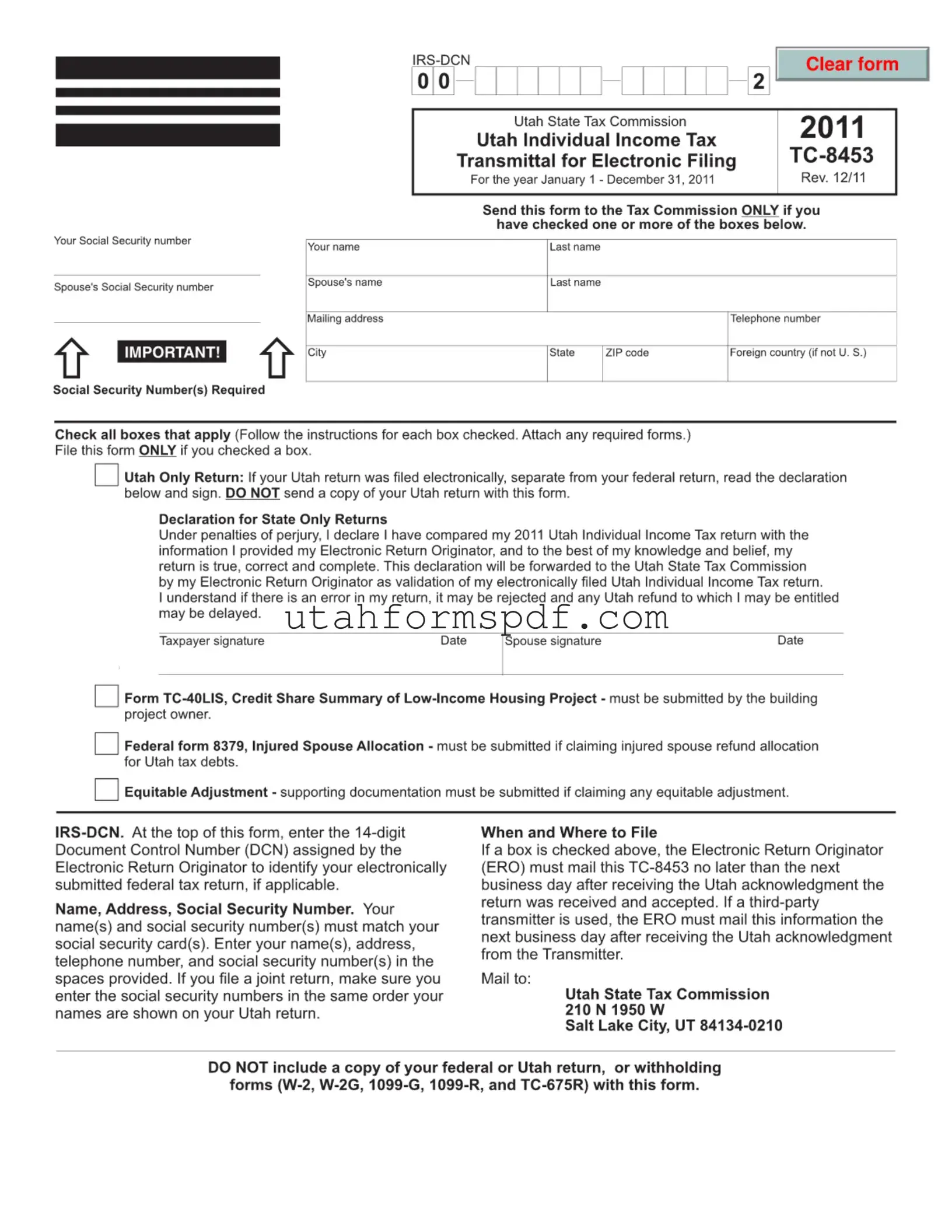

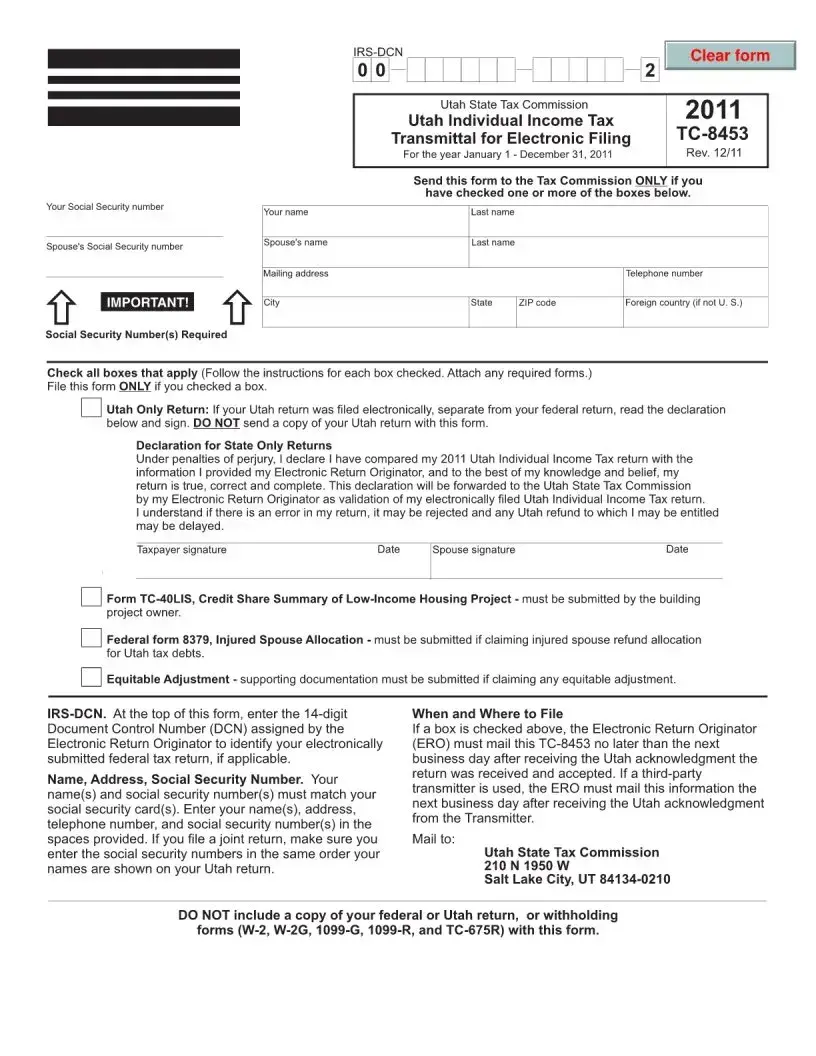

Blank Tc 8453 Utah Form

In the realm of state taxation, the TC 8453 Utah form emerges as a crucial document for residents engaging in the electronic filing of their tax returns. This form serves as an authorization for electronic filing, allowing taxpayers to verify their identity and consent to the electronic submission of their return. It is an integral part of ensuring that the electronic processing of taxes is both efficient and secure, providing a paper trail for electronic submissions. Each year, individuals who choose the convenience of filing electronically must complete this form, essentially confirming the accuracy of the information submitted to the Utah State Tax Commission. Moreover, it includes sections for declaring tax preparation fees and designating a third party to discuss the return with tax officials. By streamlining the filing process, the TC 8453 form plays a pivotal role in making tax season less daunting for Utah residents, while also maintaining high standards of accuracy and integrity in state tax administration.

Form Preview Example

Form Breakdown

| Fact Name | Description |

|---|---|

| Form Title | TC-8453 Utah Form |

| Purpose | Used for electronic filing of Utah state tax returns |

| Governing Law | Utah State Tax Code |

| Use Case | Individuals who choose to file their state taxes electronically |

| Requirement | Must be completed by taxpayers who opt for electronic filing |

| Accessibility | Available for download from the Utah State Tax Commission's official website |

| Filing Deadline | Typically aligns with the federal tax return deadline, April 15th, unless otherwise specified |

Detailed Steps for Writing Tc 8453 Utah

Once an individual or entity has completed their tax returns digitally, the next step involves authenticating and submitting these documents to the relevant tax authorities. The Tc 8453 Utah form plays a critical role in this process, as it serves as the electronic filing declaration for individuals. Proper completion and submission of this form ensure that the tax return is processed efficiently and accurately. Before starting, ensure that you have all necessary information, including social security numbers, tax amounts, and any relevant financial documents. Follow these steps carefully to fill out the Tc 8453 Utah form correctly.

- Start by entering the primary taxpayer's Social Security Number (SSN) in the designated space. If filing jointly, include the spouse's SSN in the provided area.

- Fill in the primary taxpayer's first name, middle initial, and last name. For joint returns, include the spouse's first name, middle initial, and last name in the subsequent field.

- Enter the primary taxpayer’s phone number, including the area code, to facilitate communication regarding the tax return.

- Provide the complete address of the primary taxpayer, including street address or PO box, city, state, and zip code.

- If applicable, fill in the Identity Protection Personal Identification Number (IP PIN) for the primary taxpayer and spouse. This is necessary for those who have been assigned an IP PIN by the IRS.

- Under the tax return information section, specify the tax year and form number you are filing. This ensures that the declaration is matched to the correct tax return.

- Input the total amount of state tax refund, if any, as reported on the tax return. This figure is crucial for accurately assessing state tax obligations.

- Detail the amount of use tax included in the tax return. The use tax applies to purchases made outside of the state for use within Utah.

- Enter the preparer’s PTIN (Preparer Tax Identification Number) and ERO’s EFIN (Electronic Filer Identification Number), if applicable. This information is required for returns prepared or filed by a professional.

- Finally, the primary taxpayer (and spouse, if filing jointly) must sign and date the form to validate the information provided and authorize the electronic filing. If a paid preparer completed the return, they must also sign and date the form.

After filling out the form, it is essential to review all information for accuracy before submission. Ensure that all signatures are in place and that the form is directed to the appropriate tax processing center. Submitting the Tc 8453 Utah form is a crucial final step in electronically filing your tax returns, marking the completion of your tax filing obligations for the year.

Common Questions

-

What is the TC 8453 Utah form?

The TC 8453 Utah form, known as the "Utah Individual Income Tax Return E-file Signature Authorization," is a document used by taxpayers in Utah. It allows them to authorize the electronic filing of their state income tax return by a third party, such as a tax professional. This form serves as a confirmation that the taxpayer has reviewed their return, agrees with the information presented, and authorizes the electronic submission to the Utah State Tax Commission.

-

Do all taxpayers need to file the TC 8453 Utah form?

Not all taxpayers need to file the TC 8453 Utah form. This form is specifically for those choosing to file their Utah state income tax return electronically through a third party. If you file your tax return by mail or personally e-file without the assistance of a tax preparer, this form is not required.

-

How do I complete the TC 8453 Utah form?

- Provide your name, social security number, and contact information.

- Review the tax return information for accuracy.

- Sign and date the form to authorize e-filing.

- If filing jointly, ensure that both spouses' information is included and both sign the form.

This form is designed to be straightforward, ensuring you can easily authorize the electronic filing of your tax return.

-

Where can I find the TC 8453 Utah form?

The TC 8453 Utah form is available on the Utah State Tax Commission's official website. It can be downloaded for free. Additionally, most tax preparation services will have access to this form and can provide it to you when they prepare your taxes.

-

Is there a filing deadline for the TC 8453 Utah form?

Since the TC 8453 Utah form accompanies your state tax return, it shares the same deadline as your tax return. Generally, this deadline is April 15th. However, if the 15th falls on a weekend or holiday, the deadline may be the next business day. It's important to check the current year's exact filing dates to avoid any late submission penalties.

-

Can I file the TC 8453 Utah form electronically?

Yes, the TC 8453 form is designed to accompany your electronic tax return and thus can be submitted electronically through your tax preparer. However, you must manually sign the form, or use an approved electronic signature method if your tax preparer offers this option.

-

What happens if I make a mistake on the TC 8453 Utah form?

If you discover a mistake on the TC 8453 form after submission, it's important to act quickly. You should contact the Utah State Tax Commission or your tax preparer for guidance on correcting the error. Corrections may involve submitting an amended tax return or other documentation, depending on the nature of the mistake.

-

Do I need to keep a copy of the TC 8453 Utah form?

Yes, you should keep a copy of the TC 8453 Utah form for your records. It's recommended to keep copies of all tax-related documents for at least three years. These documents may be needed for future reference or in the event you are audited by the state tax authority.

-

Is the TC 8453 Utah form required for amending a tax return?

Yes, if you are amending your tax return electronically, you will need to complete a new TC 8453 Utah form to authorize the electronic filing of the amended return. This ensures that your authorization is up to date and reflects any changes made to your original tax return.

Common mistakes

Filling out tax forms can be a daunting task, and the TC 8453 Utah form is no exception. People often make mistakes when completing this document, which can lead to delays or problems with their tax returns. Understanding some of the common errors can help filers avoid these pitfalls and ensure their submissions are processed smoothly.

One of the most frequent mistakes is not double-checking the information entered against their tax return documents. This includes figures such as income, tax credits, deductions, and personal information. It's crucial that the details on the TC 8453 form match exactly with those on the tax return. An oversight here can cause unnecessary delays.

- Not signing the form. The TC 8453 is an electronic return originator form, which means it requires a signature to verify its authenticity. Skipping the signature step is a common mistake that can invalidate the document.

- Incorrect identification numbers. Taxpayer Identification Numbers (TIN) or Social Security Numbers (SSN) must be accurate. Entering these numbers incorrectly can lead to processing errors.

- Forgetting to include the PIN. The Personal Identification Number is a critical piece of information that confirms the taxpayer's identity. Neglecting to include it is a frequent oversight.

- Mismatching names and numbers. Every detail on the form must match the information the IRS has on file. This includes names, SSNs, and TINs.

- Leaving sections blank. Every required field must be filled out. Empty sections can cause the form to be returned.

- Failing to attach the necessary documents. Certain documents must accompany the TC 8453 form for verification purposes. Not including these can result in processing delays.

- Using outdated information. Tax laws and form requirements can change from year to year. Using the wrong version of the form or outdated instructions can lead to mistakes.

- Selecting the wrong tax year. Filing for the wrong tax year is a surprisingly common error that can confuse the processing system.

- Ignoring IRS instructions. The IRS provides specific instructions for the TC 8453 form. Overlooking these can result in incorrect or incomplete filling out of the form.

To avoid these mistakes, filers should take their time, carefully review all instructions and details, and double-check their work against their tax return paperwork. Additionally, consulting with a tax professional or using tax software can help ensure that everything is completed accurately. Preparing and submitting tax forms correctly is crucial for a smooth tax return process, avoiding delays, penalties, and headaches.

Documents used along the form

When individuals prepare to file their state taxes in Utah, they often encounter a variety of forms and documents, one pivotal piece being the TC-8453 Utah form. This crucial document serves as the Utah Individual Income Tax Return Electronic Filing Declaration, an essential part of the electronic filing process. Filing taxes electronically ensures accuracy, speeds up the refund process, and is more environmentally friendly than paper filing. However, the TC-8453 form is but one of several documents taxpayers may need to successfully navigate their state tax obligations. Below, we describe additional forms and documents frequently used in tandem with the TC-8453 form to provide a comprehensive overview of the tax preparation process in Utah.

- W-2 Form: This wage and tax statement is issued by employers to report an employee's annual income and taxes withheld. Essential for all individuals employed during the tax year, it provides necessary information to complete income tax returns accurately.

- 1099 Form: Various 1099 forms report income from sources other than employment, such as independent contractor earnings (1099-NEC), interest and dividends (1099-INT and 1099-DIV), and government payments like tax refunds or unemployment compensation (1099-G).

- Schedule A (Form 1040): For those who itemize deductions instead of taking the standard deduction, Schedule A is required. It covers deductible expenses such as medical and dental expenses, taxes paid, interest paid, gifts to charity, casualty and theft losses, and other miscellaneous deductions.

- UTAH Schedule TC-40B: This is the Non or Part-year Resident Income Schedule, necessary for individuals who have either moved to Utah and became residents or moved out of Utah and became nonresidents during the tax year. It helps in determining the amount of income subject to Utah taxes.

- TC-547: The Payment Coupon is used when individuals owe taxes to the state of Utah and are not making their payment electronically. This coupon accompanies the check or money order used to pay Utah state taxes.

- TC-40: The Utah Individual Income Tax Return form is the standard form for Utah residents. While the TC-8453 is for electronic filing, the TC-40 is the comprehensive form used to calculate Utah state income tax owed or the refund due to the taxpayer.

Engaging with these documents, each designed for specific circumstances, reinforces the importance of a thorough and individualized approach to state tax preparation. Depending on personal or financial situations, such as changes in residency, employment, or investments, the complexity of one's tax situation may vary. Therefore, understanding and utilizing the appropriate forms, including the TC-8450 Utah form, facilitates accurate and efficient tax filing, ensuring that taxpayers meet legal obligations while optimizing their financial outcomes.

Similar forms

The TC 8453 Utah form, primarily used for submitting state income tax returns electronically, bears a resemblance to the Federal Form 8453, "U.S. Individual Income Tax Transmittal for an IRS e-file Return". Both serve as authorization documents, allowing for the electronic transmission of tax returns to their respective tax authorities. The similarity lies in their purpose, as they ensure that electronic filings are accompanied by necessary documentation that cannot be submitted electronically, ensuring compliance and verification of the taxpayer's information.

Similar to the IRS Form 8868, "Application for Automatic Extension of Time To File an Exempt Organization Return", the TC 8453 form also facilitates a type of submission to tax authorities, albeit for different purposes. Where Form 8868 is utilized to request more time for filing an organization's tax return, the TC 8453 covers individual electronic filing. Both share the critical function of maintaining timely communication with tax authorities, ensuring that taxpayers or organizations remain in good standing while they complete necessary filings.

Another document of similarity is the Form W-2, "Wage and Tax Statement". While the Form W-2 is an employer-issued document that reports an employee's annual wages and the amount of taxes withheld from their paycheck, its submission is pivotal for individuals filing their tax returns, including when using forms like the TC 8453 for electronic filing. The connection between them arises from the necessity of accurate and verified income information to fulfill tax obligations.

The Schedule K-1 (Form 1065), used by partnerships to report the income, deductions, and credits of each partner, shares commonalities with the TC 8453 in the aspect of tax reporting. Taxpayers who receive a Schedule K-1 will use the information when completing their own tax returns, possibly electronically using forms like the TC 8453. Both documents are integral parts of the tax reporting and filing process, linking individual income reporting to the collective financial activities of a partnership.

The IRS Form 1040, "U.S. Individual Income Tax Return", is the foundation for both traditional and electronic tax filings, into which the TC 8453 form integrates. The Form 1040 collects an individual's yearly income, tax deductions, and credits details. The connection to the TC 8453 lies in its facilitation of electronic filing for taxpayers who fill out Form 1040, allowing them to submit their tax returns and accompanying documentation to the state tax authority securely.

Form 1099-MISC, "Miscellaneous Income", is issued to report various types of income outside wages, salaries, and tips. Individuals receiving this form may include the information when filing their state tax returns electronically, using documents like the TC 8453. The similarity hinges on the role of both forms in the tax reporting and filing process, ensuring the comprehensive accounting of an individual's annual income from diverse sources for accurate tax assessment.

The IRS Form 4868, "Application for Automatic Extension of Time to File U.S. Individual Income Tax Return", parallels the TC 8453 in providing mechanisms for taxpayers to meet their filing obligations adequately. Form 4868 offers individuals additional time to file their Federal income tax returns, similar to how the TC 8453 facilitates the electronic submission of state tax returns and accompanying documents, highlighting a shared goal of supporting taxpayer compliance with filing deadlines and requirements.

Form 2555, "Foreign Earned Income", used by taxpayers to report income earned abroad, ties into the process of electronic filing with the TC 8453 for state taxes, especially for those who must account for foreign income on their state tax returns. The linkage between these forms comes from the necessitation to accurately report all sources of income, domestic or foreign, ensuring that taxpayers fulfill their state tax obligations comprehensively and in compliance with tax laws.

The IRS Form 8949, "Sales and Other Dispositions of Capital Assets", is requisite for taxpayers to report the sale or exchange of capital assets, which could include stocks, bonds, and real estate. For individuals utilizing the TC 8453 for their state electronic filing, information from Form 8949 may need to be considered to accurately reflect gains or losses that impact state tax liabilities. This similarity underscores the importance of both forms in ensuring accurate tax reporting and compliance.

Lastly, the IRS Form 940, "Employer's Annual Federal Unemployment (FUTA) Tax Return", shares a conceptual link with the TC 8453 by dealing with taxation matters, though for different subjects. Where Form 940 is concerned with unemployment taxes that employers must file, the TC 8453 assists individuals with their state income tax electronic filings. Both documents play pivotal roles in the broader tax filing ecosystem, ensuring that different aspects of taxation are adequately addressed and complied with according to federal and state laws.

Dos and Don'ts

Filling out the TC 8453 Utah form, which is an essential document for taxpayers who choose to electronically file their tax returns, requires careful attention to detail and understanding of what is expected. To assist you in this process, here are seven do's and don'ts that aim to guide you through filling out this form accurately and efficiently.

Do:

- Verify your personal information thoroughly, including your full name, address, and Social Security Number (SSN), to ensure they match the records with the Social Security Administration and your tax documents.

- Use a black or blue ink pen if you are filling out the form by hand. This makes your information legible and ensures that it is captured correctly during processing.

- Review the tax figures you report on this form against your tax return to confirm their accuracy. Any discrepancies can lead to delays or errors in processing your return.

- Sign and date the form in the designated areas. Your signature is crucial as it validates the form and authorizes the electronic filing of your return.

- Keep a copy of the signed form for your records. This will be helpful for future reference or in case the IRS requires further verification.

- Contact a professional if you encounter any questions or uncertainties. Tax laws can be complex, and professional advice can help mitigate errors.

- Submit the form within the deadline. Prompt submission avoids penalties and interest charges associated with late filing.

Don't:

- Forget to attach any required documentation that may need to accompany your TC 8453 form. Failure to do so can result in processing delays.

- Use correction fluid or tape on the form. If you make an error, it is advisable to start with a fresh form to avoid any misinterpretations of your entries.

- Ignore the instructions provided with the form. These instructions are designed to help you complete the form correctly and answer any common questions.

- Overlook the importance of double-checking your routing and account numbers if you are expecting a refund to be deposited directly into your bank account. Incorrect information can delay your refund or direct it to the wrong account.

- Submit the form without making sure all required fields are completed. Incomplete forms can be rejected or result in processing delays.

- Rush through filling out the form without verifying the details of your tax return. Mistakes can lead to further scrutiny, audits, or adjustments by the IRS.

- Be tempted to leave the signature date blank or to pre-date your signature. The IRS requires an accurate signature date to process your electronic filing effectively.

Misconceptions

The TC-8453 Utah form, associated with tax filings, often comes under discussion due to misunderstandings regarding its purpose, requirements, and processing. Highlighting these misconceptions helps clarify its role and importance for taxpayers in Utah. Here are seven common misconceptions about the TC-8453 form:

- Misconception 1: The TC-8453 is only for businesses. While businesses do use this form, it's also designed for individual taxpayers. Its primary purpose is to authenticate electronic filings of Utah tax returns, applicable to both personal and business tax submissions.

- Misconception 2: If you file electronically, the TC-8453 doesn't need to be submitted. Contrary to this belief, the form acts as a verification for electronically filed returns. Taxpayers who e-file are required to fill out this form and keep it for their records; it is not typically sent to the Utah State Tax Commission unless requested.

- Misconception 3: The form is complicated and requires professional help to fill out. The TC-8453 form is straightforward and comes with instructions that make it easy for most people to complete without professional assistance. It primarily requires basic personal information and details about the tax return filed electronically.

- Misconception 4: There's a filing fee associated with the TC-8453. Filing the TC-8453 form does not incur a fee. It is a declaration document that accompanies an electronic filing to ensure the authenticity of the information provided in the tax submission.

- Misconception 5: You must mail the TC-8453 to the Utah State Tax Commission immediately after filing taxes. Taxpayers should retain the completed form and only submit it if requested by the Tax Commission. The act of retaining the form serves as proof of the electronically filed return.

- Misconception 6: The TC-8453 form is only relevant the year you file your taxes. This form must be kept as part of your tax records for at least three years from the date of filing or two years from the date the tax was paid, whichever is later. This retention period aligns with the audit period during which your records may be reviewed.

- Misconception 7: Digital signatures are not allowed on the TC-8453. In reality, the Utah State Tax Commission does accept digital signatures on the TC-8453 form, recognizing the move towards digital documentation and processes. It's a convenient option for taxpayers who manage their documents electronically.

Key takeaways

The TC 8453 form, also known as the Utah State Individual Income Tax Return Declaration for Electronic Filing, plays a crucial role for residents when filing their state taxes electronically. Here are some of the key takeaways to ensure a smooth and accurate filing process:

- The form functions as an authorization document, allowing the electronic submission of a taxpayer's return to the Utah State Tax Commission. It's crucial for taxpayers who prefer the ease and efficiency of online filing.

- Accuracy is paramount when completing the TC 8453 form. Taxpayers must ensure that all information, including their full name, address, Social Security Number, and the tax year, aligns exactly with what's on their federal return.

- When it comes to signing the TC 8453, electronic signatures are accepted. This feature simplifies the process, enabling taxpayers or their representatives to authenticate the document without the need for a physical signature.

- There's a section designated for a paid preparer's use, should a taxpayer decide to engage a professional for their tax filing. This section requires the preparer's information and signature, attesting to the accuracy of the return as per the available documentation.

- It's important for taxpayers to attach any required documentation that is necessary to support their electronic filing. This may include W-2s or other tax documents that verify the information submitted electronically.

- Before submitting the TC 8453, a thorough review is advisable to catch any possible errors or omissions. Mistakes on this form can lead to processing delays or issues with the tax return.

- Finally, keeping a copy of the completed TC 8453 form for personal records is a wise practice. This ensures that the taxpayer has a reference, should any questions or issues arise with the state tax return at a later date.

Understanding and properly completing the TC 8453 form is essential for taxpayers who choose the convenience of electronic filing for their Utah state tax return. It streamlines the process, making it faster and more efficient, provided the information is accurate and complete.

Common PDF Templates

Bankruptcy Forms - Provides a clear avenue for creditors to assert rights to wages, salaries, or compensation priority claims.

Utah Dopl Ap - Fingerprinting can be completed at DOPL's office or at BCI, local police stations, or authorized agencies, with electronic scanning offered as a quicker alternative to traditional ink fingerprinting.

What Is Odometer Rollback - Through the TC-891, Utah ensures that the transfer of vehicle ownership is both truthful and compliant with legal standards.