Blank Tc 738 Utah Form

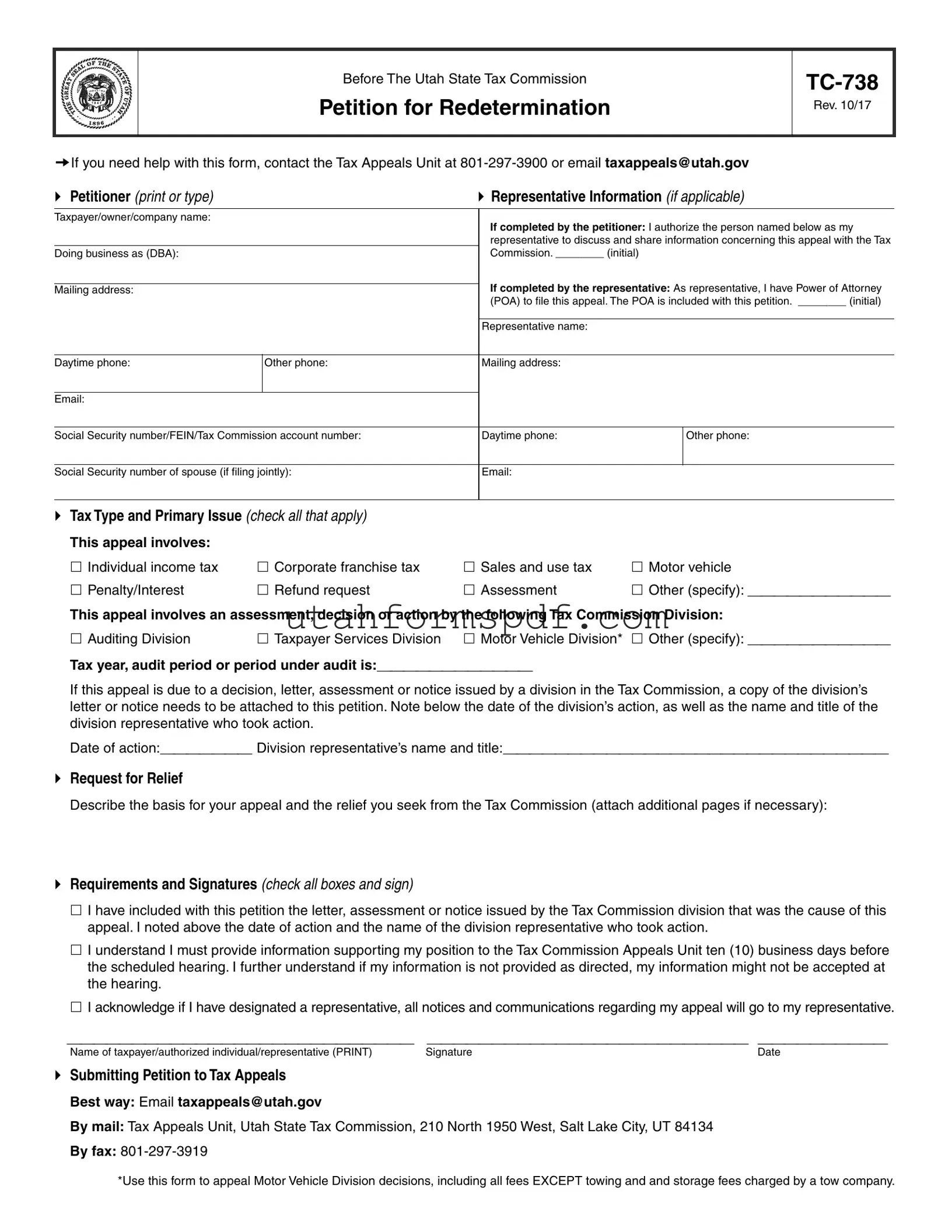

Understanding the TC 738 Utah form is essential for anyone seeking to appeal a decision by the Utah State Tax Commission. This comprehensive form serves as a Petition for Redetermination, allowing taxpayers to contest assessments, decisions, or actions taken by the Tax Commission. Whether you're an individual disputing an income tax assessment, a company challenging a corporate franchise tax, or facing disputes related to sales and use tax or motor vehicle taxes, this form is your initial step toward making your case. It meticulously outlines the necessary information for both the petitioner and their representative, if applicable, including authorization for representation and power of attorney details. Additionally, the form requires specifics on the tax type, primary issue at stake, and details about the contested decision or action, including any assessments or notices received from the Tax Commission. Importantly, petitioners are instructed to provide the basis for their appeal and the relief they seek, ensuring the Tax Appeals Unit has a clear understanding of the case. The necessity of including relevant documentation with the petition is emphasized, along with the petitioner's understanding of procedural requirements ahead of a scheduled hearing. Submission details offer various avenues for lodging the appeal, ensuring accessibility for all petitioners. Through this form, the Utah State Tax Commission ensures a structured process for appeals, emphasizing the importance of detailed information and adherence to submission guidelines.

Form Preview Example

Before The Utah State Tax Commission

Petition for Redetermination

Rev. 10/17

If you need help with this form, contact the Tax Appeals Unit at

Petitioner (print or type) |

Representative Information (if applicable) |

Taxpayer/owner/company name:

Doing business as (DBA):

Mailing address:

If completed by the petitioner: I authorize the person named below as my representative to discuss and share information concerning this appeal with the Tax Commission. ________ (initial)

If completed by the representative: As representative, I have Power of Attorney (POA) to file this appeal. The POA is included with this petition. ________ (initial)

Representative name:

Daytime phone:

Other phone:

Mailing address:

Email:

Social Security number/FEIN/Tax Commission account number:

Daytime phone:

Other phone:

Social Security number of spouse (if filing jointly):

Email:

Tax Type and Primary Issue (check all that apply)

This appeal involves: |

|

|

|

Individual income tax |

Corporate franchise tax |

Sales and use tax |

Motor vehicle |

Penalty/Interest |

Refund request |

Assessment |

Other (specify): ___________ |

This appeal involves an assessment, decision or action by the following Tax Commission Division: |

|||

Auditing Division |

Taxpayer Services Division |

Motor Vehicle Division* Other (specify): ___________ |

|

Tax year, audit period or period under audit is:____________

If this appeal is due to a decision, letter, assessment or notice issued by a division in the Tax Commission, a copy of the division’s letter or notice needs to be attached to this petition. Note below the date of the division’s action, as well as the name and title of the division representative who took action.

Date of action:_______ Division representative’s name and title:______________________________

Request for Relief

Describe the basis for your appeal and the relief you seek from the Tax Commission (attach additional pages if necessary):

Requirements and Signatures (check all boxes and sign)

I have included with this petition the letter, assessment or notice issued by the Tax Commission division that was the cause of this appeal. I noted above the date of action and the name of the division representative who took action.

I understand I must provide information supporting my position to the Tax Commission Appeals Unit ten (10) business days before the scheduled hearing. I further understand if my information is not provided as directed, my information might not be accepted at the hearing.

I acknowledge if I have designated a representative, all notices and communications regarding my appeal will go to my representative.

___________________________ _________________________ __________

Name of taxpayer/authorized individual/representative (PRINT) |

Signature |

Date |

Submitting Petition to Tax Appeals

Best way: Email taxappeals@utah.gov

By mail: Tax Appeals Unit, Utah State Tax Commission, 210 North 1950 West, Salt Lake City, UT 84134

By fax:

*Use this form to appeal Motor Vehicle Division decisions, including all fees EXCEPT towing and and storage fees charged by a tow company.

Form Breakdown

| Fact Number | Fact Detail |

|---|---|

| 1 | The form is designed for petitions for redetermination with the Utah State Tax Commission. |

| 2 | The latest revision of the form is from October 2017. |

| 3 | Assistance for filling out the form can be obtained by contacting the Tax Appeals Unit via phone or email. |

| 4 | A petitioner can authorize a representative to discuss and share information about the appeal. |

| 5 | Representatives filing on behalf of a petitioner must have Power of Attorney and include it with the petition. |

| 6 | The form allows appeals on various tax types and issues, including assessments, decisions, or actions by different divisions. |

| 7 | A necessary part of the submission is attaching the letter, assessment, or notice issued by the Tax Commission division that prompted the appeal. |

| 8 | Petitioners must provide supporting information to the Tax Commission Appeals Unit ten business days before a scheduled hearing. |

| 9 | There's an acknowledgment that if a representative is designated, all notices and communications will be sent to them. |

| 10 | The form can be submitted via email, mail, or fax, with specific contact details provided for each method. |

Detailed Steps for Writing Tc 738 Utah

Filling out the TC-738 form is a necessary step for individuals or entities in Utah wishing to challenge a decision made by the Utah State Tax Commission. This form is used to petition for a redetermination of a tax-related decision, whether it's concerning individual income tax, corporate franchise tax, vehicle tax, penalties, interest, or other assessments. By carefully following the steps outlined below, petitioners can ensure their appeal is properly submitted for consideration.

- Start with the section titled Petitioner (print or type). Fill in the taxpayer/owner/company name and, if applicable, the Doing Business As (DBA) name.

- Provide the complete mailing address of the petitioner.

- If the petition is being completed by the petitioner, initial the statement authorizing a representative to discuss and share information concerning the appeal, if applicable.

- For representatives filing the petition, fill in the representative's name, daytime phone, other phone, and mailing address. Include the representative's email and initial the statement about having Power of Attorney (POA), ensuring the POA document is attached to the petition.

- Enter the Social Security number/FEIN/Tax Commission account number, the daytime phone, other phone, and email of the petitioner. If filing jointly, include the spouse's Social Security number.

- Under Tax Type and Primary Issue, check all boxes that apply to the nature of the appeal. Specify other types of tax or issues if the listed ones do not apply.

- Specify the tax year, audit period, or period under review.

- Attach a copy of the letter, assessment, or notice issued by the Tax Commission division related to the appeal. Clearly write the date of the division’s action and the name and title of the division representative.

- In the Request for Relief section, describe in detail the basis of your appeal and the type of relief you are seeking from the Tax Commission. Attach additional pages if necessary.

- Under Requirements and Signatures, check all the boxes to acknowledge you have included all necessary documents with your petition and understand the submission guidelines. Sign and date the form in the designated area.

- To submit your petition, choose the best way for you based on convenience and confirmation receipt: email (taxappeals@utah.gov), mail (address provided), or fax (801-297-3919).

After the form is submitted, the Tax Appeals Unit of the Utah State Tax Commission will review the submitted petition. They may contact the petitioner or the representative for additional information or clarification before scheduling a hearing. It's crucial to provide accurate contact information and to check all information for completeness before submission to avoid delays in the petition process.

Common Questions

Frequently Asked Questions about the TC-738 Utah Form

- What is the purpose of the TC-738 form?

The TC-738 form, also known as the "Petition for Redetermination," is designed for individuals, companies, or representatives seeking to appeal a decision, action, or assessment made by the Utah State Tax Commission. Whether it concerns individual income tax, corporate franchise tax, sales and use tax, motor vehicle issues, or other tax-related matters, this form initiates the formal process of contesting the Tax Commission's determination.

- Who should complete the TC-738 form?

Any taxpayer or entity (referred to as the petitioner) disputing a tax-related decision or assessment by the Utah State Tax Commission should complete the TC-738 form. Additionally, a representative, such as an attorney or accountant with Power of Attorney (POA) for the taxpayer, can also complete the form on behalf of the petitioner, provided the POA documentation is included with the petition.

- What information is required to fill out the form?

The TC-738 form requires detailed information from the petitioner or their representative, including the taxpayer's name, doing business as (DBA) name if applicable, mailing address, contact information, and relevant tax identification numbers. The form also requires specifics about the tax type and primary issue being contested, details about the Tax Commission's decision or action including dates and representative names, and a clear statement describing the basis for the appeal and the relief sought.

- How does one submit the TC-738 form?

The form can be submitted to the Tax Appeals Unit of the Utah State Tax Commission through three primary methods: by email to taxappeals@utah.gov, by mail to the Tax Appeals Unit at the address provided on the form, or by fax at 801-297-3919. It's crucial to include all required documentation, such as the Tax Commission's letter or notice that instigated the appeal and any other supporting materials.

- Is there a deadline for submitting the TC-738 form?

While the TC-738 form itself does not specify a submission deadline, it is generally recommended to file your petition as soon as possible after receiving the decision or assessment you wish to appeal. Keep in mind, specific tax matters may have their own deadlines for appeal under Utah law, so it's advisable to act swiftly to ensure your appeal is considered.

- Can I appoint a representative to handle my appeal?

Yes, you are allowed to designate a representative, such as a lawyer or certified public accountant, to act on your behalf in the appeal process. You must indicate this on the TC-738 form by initializing the appropriate section and including the representative's contact information. It's important to also attach a Power of Attorney document that authorizes your representative to discuss and share information concerning your appeal with the Tax Commission.

Common mistakes

When filling out the TC-738 Utah form, also known as the Petition for Redetermination form before the Utah State Tax Commission, individuals often make mistakes that can delay or negatively impact the processing of their appeal. Understanding these common errors can help in correctly completing the form and streamlining the appeals process.

One frequent mistake is not including the required documentation to support the appeal. The form explicitly asks petitioners to attach a copy of the letter, assessment, or notice issued by the Tax Commission division that was the cause of the appeal. Failing to do so can result in an incomplete petition, which may delay the review process or lead to outright rejection of the appeal. It's crucial to gather and attach all relevant documentation before submitting the form.

Another common error is inaccurately or incompletely filling out contact information. The form requests detailed contact information, including mailing addresses, daytime and other phone numbers, and email addresses for both the petitioner and, if applicable, the representative. Misinformation or omissions in this section can hinder communication between the Tax Commission and the individuals involved, possibly affecting the outcome of the appeal.

- Not authorizing a representative correctly is a critical misstep. If a petitioner chooses to have a representative, they must initial the section authorizing this individual to act on their behalf. Additionally, the representative needs to indicate they have Power of Attorney (POA) and include the POA document with the petition. Failure to complete this step properly can lead to procedural delays or the Tax Commission disregarding the representative's communications.

- Overlooking the checkboxes in the "Requirements and Signatures" section is another slip-up. Petitioners must actively check each box to affirm they have attached the necessary documentation, understand the requirements for providing supporting information, and acknowledge the communication protocol if a representative is involved. This oversight could lead to the petitioner's appeal not being processed in a timely manner.

Ensuring all details and documentation are accurately represented on the TC-738 form is paramount. Aside from the errors mentioned, there are general best practices to follow:

- Double-check all filled-out sections for completeness and accuracy.

- Be clear and concise in the "Request for Relief" section, explaining the basis for the appeal and the specific outcome desired.

- Maintain copies of the submitted form and all attached documents for personal records.

By avoiding these common pitfalls and adhering to the form's requirements, petitioners can ensure a smoother process in their appeal before the Utah State Tax Commission.

Documents used along the form

When dealing with the Utah State Tax Commission, particularly for concerns requiring a Petition for Redetermination (TC-738), it's common to encounter the need for additional documents. These documents play a pivotal role in supporting the appeal, providing required legal authorization, or ensuring compliance with regulatory demands. Below is a description of other forms and documents often used in conjunction with the TC-738 form.

- Power of Attorney (POA): This legal document authorizes a representative to act on behalf of the petitioner in tax matters. It is crucial when a petitioner has designated someone else to handle their appeal.

- Notice of Agency Action: Issued by the Tax Commission, this notice informs of the decision or action taken that is being appealed. A copy of this notice is critical for providing the context and basis for the appeal.

- Evidence Documentation: This includes any records, receipts, ledgers, or other forms of documentation that support the petitioner's case against the Audit, Taxpayer Services, or Motor Vehicle Division's decision.

- Letter of Assessment: A formal notice from the Tax Commission detailing taxes owed, including penalties and interest. This document is necessary when appealing against an assessed tax liability.

- Registration Forms for Business Entities: When the appeal involves a business, especially relating to sales and use tax or corporate franchise tax, the most current business registration details might be required to establish the legitimacy of the business involved in the appeal.

- Financial Statements: For certain types of appeals, especially those involving large sums or complex financial situations, audited financial statements or other financial records may be requested to substantiate the petitioner's financial position and claims.

Comprehending and gathering these documents is crucial for a thorough and compelling appeal to the Utah State Tax Commission. Not only do these documents support the appeal's narrative by providing essential details and evidence, but they also ensure that the process adheres to the procedural requirements set forth by the Commission. Individuals and businesses aiming for a successful appeal should make meticulous preparations, including obtaining and organizing these supplemental documents, to fortify their case.

Similar forms

The TC-738 Utah form, which facilitates appeals in tax-related disputes or decisions by the tax authority, shares similarities with the IRS Form 9423 (Collection Appeal Request). Both serve as a bridge for taxpayers to contest decisions regarding assessments, penalties, or other determinations made by the respective tax authority. While the TC-738 is Utah-specific, addressing state tax matters, IRS Form 9423 is utilized on a federal level. Both forms require taxpayers to provide detailed information about the dispute, including the type of tax in question, the specific issue being appealed, and the desired outcome or relief sought. Additionally, both forms emphasize the necessity for accompanying documentation and set forth procedures for taxpayers to formally authorize representation.

Comparable to the TC-738 form is the IRS Form 12153 (Request for a Collection Due Process or Equivalent Hearing). This form is used for appealing various collection actions taken by the IRS, such as liens or levies on property. Similar to the TC-738, the Form 12153 allows taxpayers to dispute the collection actions by providing a structured way to request a hearing before an independent office. Both forms act as a critical tool for taxpayers seeking to challenge the actions of their tax authority, protect their rights, and potentially alter the outcome of a tax decision or collection action against them.

Another document akin to the TC-738 is the Form SSA-561 (Request for Reconsideration), used in the context of Social Security. While this form is specific to the Social Security Administration and focuses on benefits rather than tax disputes, its function mirrors that of the TC-738 in providing a formal channel for challenging decisions, such as benefits denials or changes in benefit amounts. Both forms enable individuals to articulate their disagreement with an official decision and submit evidence in support of their appeal, showcasing the universal need for structured appeals processes across different facets of governmental decision-making.

The Administrative Review Request Form utilized within many state-level government agencies for various administrative decision appeals also parallels the TC-738. While the specific name and form number may vary by state and agency, this type of form universally allows individuals or entities to request a review of or appeal against decisions made by government bodies that affect them. Like the TC-738, these forms provide a necessary means for accountability and transparency within the public administrative process, enabling a reevaluation of decisions that may impact individuals' rights, responsibilities, or entitlements.

Dos and Don'ts

Filling out the TC-738 Utah form requires careful attention to detail and an understanding of the specific requirements set forth by the Utah State Tax Commission. Here are five important dos and don’ts to consider when preparing your petition for redetermination.

Dos:

- Double-check the taxpayer/owner/company information: Ensure that the name, doing business as (DBA) status, and mailing address are correctly entered to prevent any processing delays.

- Properly authorize representation: If you're designating a representative, remember to initial the authorization section. This grants them the permission to discuss and share information concerning your appeal.

- Include Power of Attorney (POA) if applicable: If a representative is filling out the form, a Power of Attorney must be attached to confirm their authorization to file this appeal on your behalf.

- Attach necessary documentation: It's crucial to include a copy of the letter, assessment, or notice issued by the Tax Commission division with your petition. Note the date of action and the representative's name and title for clarity.

- Provide supporting information: Ensure that all supporting information for your position is submitted to the Tax Commission’s Appeals Unit ten business days before the scheduled hearing.

Don’ts:

- Overlook the details of your appeal: Neglecting to check the applicable boxes under the “Tax Type and Primary Issue” section can lead to misunderstandings regarding the nature of your appeal.

- Forget to describe your request for relief: Failing to clearly articulate the basis of your appeal and the relief you seek could weaken your case. Attach additional pages if necessary to make your situation clear.

- Skip requirement checkboxes: Each requirement and signature box must be checked to confirm your understanding and compliance with the appeal process, omitting this can result in an incomplete submission.

- Miss the submission details: Not choosing the best submission method for your appeal might delay its processing. Consider the pros and cons of email, mail, and fax submissions.

- Omit digital signature and date: The form requires a signature and date to be considered complete. An unsigned or undated form will not be processed.

By adhering to these guidelines, individuals can navigate the process of submitting a TC-738 form more smoothly and increase the likelihood of a favorable outcome in their appeal.

Misconceptions

Many people find tax forms and the appeal process intimidating, especially when dealing with the specifics of Utah's TC-738 form for petitioning a redetermination with the Utah State Tax Commission. Let's clear up some common misconceptions about this form to make the process a bit more approachable.

Only individuals can file a TC-738 form: Actually, not just individuals, but businesses, or anyone acting as a representative, such as a tax attorney or accountant, can also file, provided they have the appropriate authorization or Power of Attorney (POA). The form itself provides space for both petitioner and representative information, emphasizing the inclusive nature of appeal rights.

The form is only for disputing tax penalties: While the TC-738 form is certainly used for appealing penalties and interest, it's also applicable to a variety of other tax-related issues. This can include disputes over individual income tax, corporate franchise tax, sales and use tax, and even motor vehicle tax issues. The form has checkboxes for the primary issue of the appeal, highlighting its broad applicability.

Filing the form starts the appeal process immediately: Submitting the form is just the beginning. Petitioners are also required to provide supporting documentation and information to the Tax Commission’s Appeals Unit well before the scheduled hearing (at least 10 business days in advance). Without this preparation, the appeal might not proceed as planned, proving there's more to it than filling out and sending the form.

You don't need to include documentation from the Tax Commission: In fact, petitioners must attach a copy of the letter, assessment, or notice issued by the Tax Commission division that prompted the appeal. This is a crucial part of the form, ensuring all sides have the same reference point during proceedings.

An attorney must fill out the form: While it’s true that legal knowledge can help, the form is designed to be accessible to taxpayers without requiring legal representation. If a petitioner feels comfortable doing so, they can complete and submit the form on their own. However, they have the option to designate a representative with Power of Attorney to manage the appeal process.

Understanding the TC-738 form is a crucial step in exercising your rights as a taxpayer in Utah. By clarifying these misconceptions, filing an appeal becomes less daunting, enabling taxpayers or their representatives to navigate the process with confidence.

Key takeaways

Filing the TC-738 Utah form is a critical process for appealing decisions made by the Utah State Tax Commission. Understanding the key aspects of this form can streamline the process and enhance your chances for a favorable outcome. Below are five essential takeaways to assist individuals and entities in navigating this appeal procedure effectively.

- Complete Identification Information Is Mandatory: The form requires detailed identification information for both the petitioner and the representative, if one is involved. This includes names, Social Security numbers, or Tax Commission account numbers, as well as contact information. It is essential for ensuring the Tax Commission can easily contact you or your designated representative regarding the appeal.

- Specify the Tax Issue and Relief Sought: Clearly marking the type of tax and primary issue at hand is crucial. The form allows for selection among various tax types such as individual income tax, corporate franchise tax, and sales and use tax, among others. Articulating the specific relief sought from the Tax Commission is also imperative, and additional pages may be attached if the space provided is insufficient.

- Attach Supporting Documents: For the appeal to be considered, you must attach any relevant letters, assessments, or notices issued by the Tax Commission division related to your appeal. Documenting the date of action and the name of the division representative who took the action is also required. This documentation is vital for providing context and evidence for your appeal.

- Understand the Representational Authorization: If a representative is completing the form on behalf of a petitioner, it's essential they have a Power of Attorney (POA) and that the POA is included with the petition. The petitioner must initial to authorize this representation, ensuring that the Tax Commission can lawfully communicate with and disclose information to the named representative.

- Adherence to the Submission Guidelines: The petition can be submitted via email, mail, or fax, offering flexibility based on your preference or the urgency of the matter. It's important to follow the best submission route as recommended by the Tax Appeals Unit to expedite the processing of your appeal. Additionally, ensure all requirements and signatures are completed to avoid delays or rejection of your petition.

In conclusion, careful attention to detail when completing and submitting the TC-738 Utah form is fundamental. By following these key takeaways, petitioners can ensure their appeal is clearly communicated and duly considered by the Utah State Tax Commission, facilitating a smoother resolution to their tax concerns.

Common PDF Templates

801-297-7300 - Realize the significance of individual case merits in the Utah State Tax Commission's waiver request evaluations.

Dmv Forms Utah - The TC-55A form outlines a clear process for submitting a claim for a refund, including all necessary documentation and receipts.

Utah State Tax Form for Employees - It represents a legal pathway to obtain a personalized plate, ensuring all customizations are recorded and recognized by the state.