Blank Seller Utah Form

In the realm of real estate transactions within Utah, the Seller Financing Addendum reveals itself as a pivotal document, meticulously designed to supplement the Real Estate Purchase Contract (REPC). This addendum plays an essential role by delineating the specific terms under which the seller agrees to finance the purchase for the buyer, introducing an alternative to traditional lending institutions. It outlines various critical elements such as the creation and terms of credit documents, the allocation of responsibility for taxes, assessments, and insurance premiums, alongside payment terms including late payment repercussions and prepayment privileges. Furthermore, it addresses the necessary disclosures each party must provide, such as the buyer’s financial information and the seller's credit review process. This elaborate document ensures both parties are adequately informed and agree upon key factors such as due-on-sale clauses, title insurance, and tax identification number disclosures, reinforcing the seamless integration of seller financing into the real estate purchase agreement. Tailored to address the unique legal framework governing Utah's real estate transactions, the Seller Financing Addendum ensures a comprehensive understanding and agreement on financing terms, safeguarding the interests of both buyer and seller.

Form Preview Example

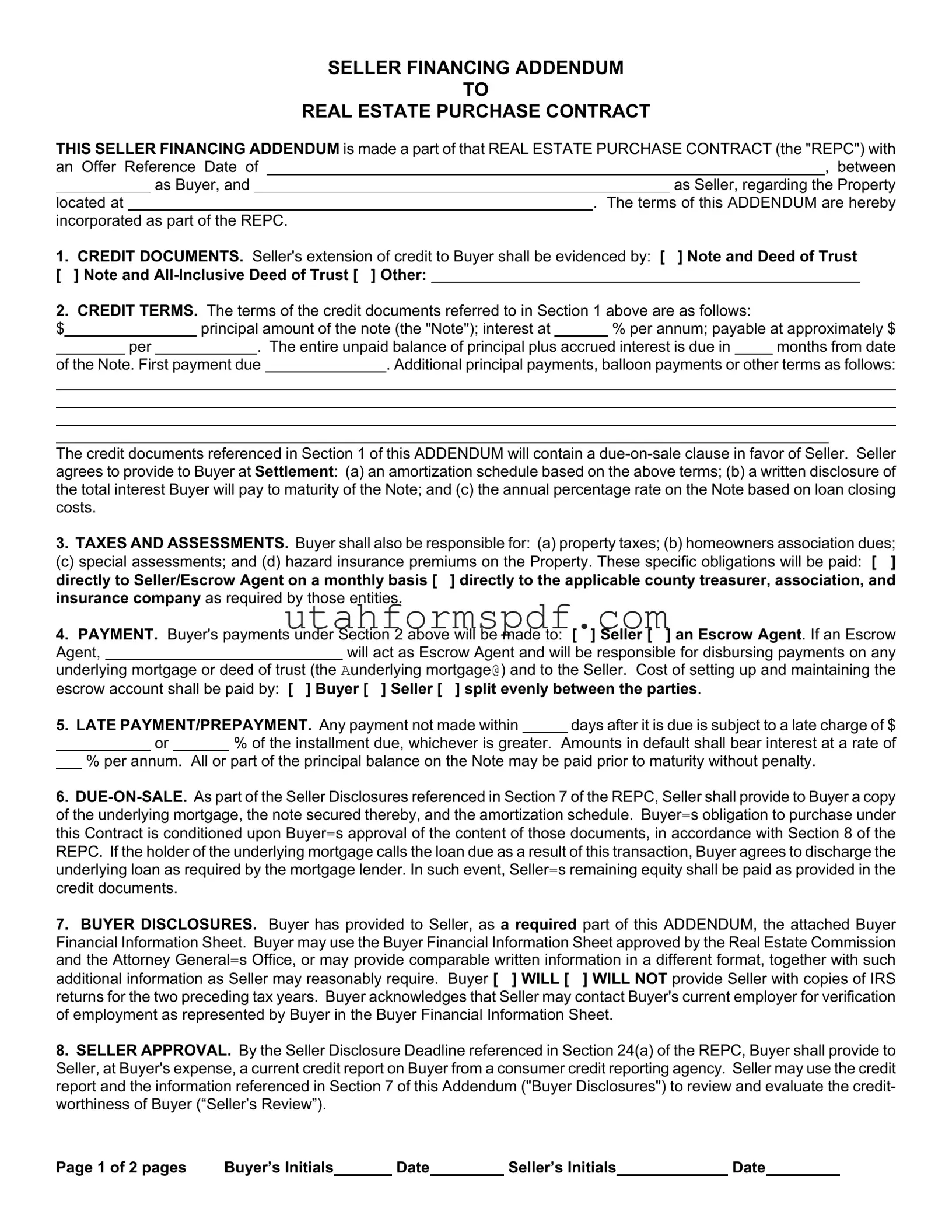

SELLER FINANCING ADDENDUM

TO

REAL ESTATE PURCHASE CONTRACT

THIS SELLER FINANCING ADDENDUM is made a part of that REAL ESTATE PURCHASE CONTRACT (the "REPC") with

an Offer Reference Date of |

|

|

|

, between |

|||

|

|

as Buyer, and |

|

|

as Seller, regarding the Property |

||

located at |

|

. The terms of this ADDENDUM are hereby |

|||||

incorporated as part of the REPC. |

|

|

|

||||

1. CREDIT DOCUMENTS. Seller's extension of credit to Buyer shall be evidenced by: [ ] Note and Deed of Trust [ ] Note and

2.CREDIT TERMS. The terms of the credit documents referred to in Section 1 above are as follows:

$ |

|

|

principal amount of the note (the "Note"); interest at |

|

% per annum; payable at approximately $ |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

per |

|

|

. The entire unpaid balance of principal plus accrued interest is due in |

|

months from date |

|||||

of the Note. First payment due |

|

. Additional principal payments, balloon payments or other terms as follows: |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The credit documents referenced in Section 1 of this ADDENDUM will contain a

3.TAXES AND ASSESSMENTS. Buyer shall also be responsible for: (a) property taxes; (b) homeowners association dues;

(c) special assessments; and (d) hazard insurance premiums on the Property. These specific obligations will be paid: [ ] directly to Seller/Escrow Agent on a monthly basis [ ] directly to the applicable county treasurer, association, and insurance company as required by those entities.

4. PAYMENT. Buyer's payments under Section 2 above will be made to: [ ] Seller [ ] an Escrow Agent. If an Escrow

Agent,will act as Escrow Agent and will be responsible for disbursing payments on any

underlying mortgage or deed of trust (the Aunderlying mortgage@) and to the Seller. Cost of setting up and maintaining the escrow account shall be paid by: [ ] Buyer [ ] Seller [ ] split evenly between the parties.

5. LATE PAYMENT/PREPAYMENT. Any payment not made within |

|

|

days after it is due is subject to a late charge of $ |

|||

|

or |

|

% of the installment due, whichever is greater. |

Amounts in default shall bear interest at a rate of |

||

%per annum. All or part of the principal balance on the Note may be paid prior to maturity without penalty.

6.

7.BUYER DISCLOSURES. Buyer has provided to Seller, as a required part of this ADDENDUM, the attached Buyer Financial Information Sheet. Buyer may use the Buyer Financial Information Sheet approved by the Real Estate Commission and the Attorney General=s Office, or may provide comparable written information in a different format, together with such

additional information as Seller may reasonably require. Buyer [ ] WILL [ ] WILL NOT provide Seller with copies of IRS returns for the two preceding tax years. Buyer acknowledges that Seller may contact Buyer's current employer for verification of employment as represented by Buyer in the Buyer Financial Information Sheet.

8.SELLER APPROVAL. By the Seller Disclosure Deadline referenced in Section 24(a) of the REPC, Buyer shall provide to Seller, at Buyer's expense, a current credit report on Buyer from a consumer credit reporting agency. Seller may use the credit report and the information referenced in Section 7 of this Addendum ("Buyer Disclosures") to review and evaluate the credit- worthiness of Buyer (“Seller’s Review”).

Page 1 of 2 pages |

Buyer’s Initials |

|

Date |

Seller’s Initials |

Date |

|||

|

|

|

|

|

|

|

|

|

8.1Seller Review. If Seller determines, in Seller’s sole discretion, that the results of the Seller’s Review are unacceptable, Seller may either: (a) no later than the Due Diligence Deadline referenced in Section 24(b) of the REPC, cancel the REPC by providing written notice to Buyer, whereupon the Earnest Money Deposit shall be released to Buyer without the requirement of further written authorization from Seller; or (b) no later than the Due Diligence Deadline referenced in Section 24(b), resolve in writing with Buyer any objections Seller has arising from Seller’s Review.

8.2Failure to Cancel or Resolve Objections. If Seller fails to cancel the REPC or resolve in writing any objections Seller has arising from Seller’s Review, as provided in Section 8.1 of this ADDENDUM, Seller shall be deemed to have waived the Seller=s Review.

9.TITLE INSURANCE. Buyer [ ] SHALL [ ] SHALL NOT provide to Seller a lender=s policy of title insurance in the amount of the indebtedness to the Seller, and shall pay for such policy at Settlement.

10.DISCLOSURE OF TAX IDENTIFICATION NUMBERS. By no later than Settlement, Buyer and Seller shall disclose to each other their respective Social Security Numbers or other applicable tax identification numbers so that they may comply with federal laws on reporting mortgage interest in filings with the Internal Revenue Service.

To the extent the terms of this ADDENDUM modify or conflict with any provisions of the REPC, including all prior addenda and counteroffers, these terms shall control. All other terms of the REPC, including all prior addenda and counteroffers, not

modified by this ADDENDUM shall remain the same. [ ] Seller [ ] Buyer shall have until |

|

[ ] AM [ ] PM |

||

Mountain Time on |

|

(Date), to accept the terms of this SELLER FINANCING ADDENDUM in |

||

accordance with Section 23 of the REPC. Unless so accepted, the offer as set forth in this SELLER FINANCING ADDENDUM shall lapse.

_________________________________________________________________________________________________

[ ] Buyer [ ] Seller Signature(Date) (Time)Social Security Number

_________________________________________________________________________________________________

[ ] Buyer [ ] Seller Signature |

(Date) (Time) |

Social Security Number |

ACCEPTANCE/COUNTEROFFER/REJECTION

CHECK ONE:

[ ]ACCEPTANCE: [ ] Seller [ ] Buyer hereby accepts these terms.

[]COUNTEROFFER: [ ] Seller [ ] Buyer presents as a counteroffer the terms set forth on the attached ADDENDUM NO.

______.

[]REJECTION: [ ] Seller [ ] Buyer rejects the foregoing SELLER FINANCING ADDENDUM.

(Signature) |

(Date) |

(Time) |

(Signature) |

(Date) |

(Time) |

|

|

|

|

|

|

(Signature) |

(Date) |

(Time) |

(Signature) |

(Date) |

(Time) |

THIS FORM APPROVED BY THE UTAH REAL ESTATE COMMISSION AND THE OFFICE OF THE UTAH ATTORNEY GENERAL,

EFFECTIVE AUGUST 27, 2008. AS OF JANUARY 1, 2009, IT WILL REPLACE AND SUPERSEDE THE PREVIOUSLY APPROVED VERSION OF THIS FORM.

Page 2 of 2 pages |

Buyer’s Initials |

|

Date |

Seller’s Initials |

Date |

|||

|

|

|

|

|

|

|

|

|

Form Breakdown

| Fact Name | Description |

|---|---|

| Form Purpose | This form serves as an addendum to a Real Estate Purchase Contract, specifically addressing terms related to seller financing. |

| Credit Documentation | The extension of credit from seller to buyer is evidenced by either a Note and Deed of Trust, a Note and All-Inclusive Deed of Trust, or another specified document. |

| Credit Terms | Details provided include the principal amount, interest rate, payment amounts, and due dates for the financed sum. |

| Additional Financial Obligations | Buyers are responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums, with specified payment procedures. |

| Payment Mechanism | Payments under the seller financing terms can be made directly to the seller or an escrow agent, with specified responsibilities for each. |

| Late Payment and Prepayment Terms | Specifies charges for late payments and conditions for prepayment without penalty. |

| Due-On-Sale Clause | The addendum contains a due-on-sale clause, which may trigger repayment of the underlying loan if the property is sold. |

| Buyer Disclosures | Buyers are required to provide financial information, potentially including tax returns, and consent to employment verification. |

| Seller's Right to Review and Approve | The seller can review the buyer's creditworthiness and either approve, cancel the contract, or resolve objections by specified deadlines. |

| Title Insurance | The buyer may be obligated to provide the seller with a lender’s policy of title insurance in the amount of the indebtedness. |

| Governing Law | The form is approved by the Utah Real Estate Commission and the Office of the Utah Attorney General, indicating it is governed by Utah law. |

Detailed Steps for Writing Seller Utah

Filling out the Seller Financing Addendum to the Real Estate Purchase Contract (REPC) is a critical step when you're buying or selling property with seller financing in Utah. This addendum details the terms under which the seller extends credit to the buyer for purchasing the property, including the payment structure, interest rate, and other financial responsibilities. Carefully completing this form ensures clarity and legal compliance for both parties throughout the transaction process. Below are the prescribed steps to accurately fill out the form.

- Start with the Offer Reference Date at the top of the form, ensuring it matches the date on the original REPC.

- Enter the Buyer's and Seller's names to confirm the parties involved in the transaction.

- Fill in the complete address of the Property being sold under this agreement.

- Under Section 1, select the type of credit document(s) being used (Note and Deed of Trust, Note and All-Inclusive Deed of Trust, or Other) and specify if "Other" is selected.

- In Section 2, detail the credit terms including the principal amount of the note, interest rate per annum, payment amount, the due date for the first payment, and any additional terms like balloon payments.

- Choose who will be responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums in Section 3 and specify the payment method.

- Indicate where payments under Section 2 will be made, to the Seller or an Escrow Agent, in Section 4. If an Escrow Agent is selected, provide their name.

- For late payments and prepayment terms, specify the late charge and interest on amounts in default in Section 5, along with terms for early principal balance payments.

- Section 7 requires attaching a Buyer Financial Information Sheet. Check whether IRS returns for the two previous tax years will be provided.

- In Section 8, acknowledge that by the Seller Disclosure Deadline, the Buyer must furnish a current credit report for the Seller's review.

- Decide in Section 9 if Title Insurance will be provided by the Buyer, and who will bear the cost.

- Before the Settlement, both parties must disclose their tax identification numbers in Section 10.

- Review and ensure all terms in the Addendum do not conflict with those in the original REPC. Make necessary adjustments or confirmations as needed.

- Both Buyer and Seller should initial and date each page to affirm their agreement to the terms laid out in the document.

- Finally, all parties involved should sign and date at the end of the document, indicating acceptance, counteroffer, or rejection of the addendum terms.

After completing these steps, the Seller Financing Addendum will effectively modify the original REPC, setting the terms under which the property will be sold with seller financing. Ensure all information is accurate and thoroughly reviewed by both parties or seek legal advice if necessary.

Common Questions

When entering into a real estate transaction in Utah that involves seller financing, parties often have many questions about the Seller Financing Addendum. Here are detailed answers to some of the most common questions regarding this document.

What is the Seller Financing Addendum in Utah?

The Seller Financing Addendum is a legal document that modifies the original Real Estate Purchase Contract (REPC) to include terms under which the seller provides financing to the buyer for purchasing property. It integrates all details such as credit documents, payment terms, responsibilities for taxes, and assessments into the REPC.

What are Credit Documents in the context of this Addendum?

Credit documents refer to the paperwork evidencing the extension of credit from the seller to the buyer. These may include a Note and Deed of Trust, an All-Inclusive Deed of Trust, or other forms as agreed between the parties. They outline the loan's principal amount, interest rate, payment schedule, and due date for the unpaid balance.

How are interest rates and payments structured?

Interest rates are determined as a percentage per annum on the principal amount of the note. Payments are made monthly, and the exact amount depends on the agreed interest rate and principal amount. The contract also specifies when the first payment is due and outlines any terms for additional principal or balloon payments.

Who is responsible for property taxes and insurance?

The buyer is responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums. Payments can be made directly to the seller or an Escrow Agent, or to the respective county treasurer, association, and insurance company, as required.

What happens if a payment is late?

Late payments are subject to a charge, either a fixed amount or a percentage of the installment due, whichever is greater. The default amounts will accrue interest at a specified annual rate until paid.

Can the principal balance be paid off early?

Yes, buyers can pay all or part of the principal balance on the Note prior to maturity without facing any penalties for early payment.

What is a due-on-sale clause?

A due-on-sale clause is a provision that requires the full repayment of the outstanding loan if the property is sold. This clause ensures that the seller can call the loan due if the buyer decides to sell the property before the loan matures.

What are the seller's approval criteria for financing?

The seller's approval is contingent upon reviewing the buyer's creditworthiness, which includes a credit report and financial information provided by the buyer. The seller has the right to cancel the REPC or resolve objections by specified deadlines if they are not satisfied with the buyer's credit.

Is title insurance required?

Whether to provide a lender’s policy of title insurance is at the buyer's discretion unless specified otherwise. If opted, the buyer bears the cost of this insurance, which protects the seller’s interest in the property up to the amount owed under the seller financing.

How do the terms of this Addendum affect the original REPC?

The terms stated in the Seller Financing Addendum modify or supersede any conflicting terms in the original REPC, including prior addenda and counteroffers. However, any aspect of the REPC not altered by this Addendum remains in effect.

Proper understanding and execution of the Seller Financing Addendum are crucial for both buyer and seller in a real estate transaction. It ensures clarity, legality, and security in the agreement, paving the way for a smooth and agreeable sale process.

Common mistakes

When filling out the Seller Financing Addendum to the Real Estate Purchase Contract in Utah, there are several common mistakes that can complicate the transaction for both the buyer and the seller. Recognizing and avoiding these errors can ensure a smoother process and protect the interests of both parties involved.

Firstly, a frequent mistake made by individuals is not providing complete details in the Offer Reference Date, Buyer, and Seller fields. It is crucial to clearly state the names of the parties involved and the effective date of the offer to avoid any ambiguity. Secondly, in the section regarding Credit Documents, failing to specify the type of credit evidence (Note and Deed of Trust, Note and All-Inclusive Deed of Trust, or Other) can lead to misunderstandings about the legal instruments governing the lending agreement.

Thirdly, when outlining the Credit Terms, ambiguities or omissions in specifying the principal amount, interest rate, payment amounts, and schedule can cause significant confusion. Miscommunication about these financial terms can impact the buyer's understanding of their obligations and the seller's expectations. Fourthly, the parties sometimes neglect to accurately detail how taxes, assessments, and insurance premiums will be paid, leading to disputes about financial responsibilities after closing.

Fifthly, another error involves not clearly agreeing upon how the payment is made to the seller or an escrow agent and who covers the escrow account setup and maintenance costs. Sixthly, a lack of clarity about the consequences of late payments or the policy on prepayments can lead to disputes or financial penalties that one party may not have anticipated.

Seventh, often buyers and sellers do not properly address the due-on-sale clause provisions, risking the acceleration of the loan without clear agreement on how to manage such a situation. Lastly, failing to accurately complete the sections related to Buyer and Seller Disclosures can leave one party with incomplete information, hampering the seller's ability to evaluate the buyer's creditworthiness and potentially leading to contract termination.

To mitigate these common pitfalls, both buyers and sellers should approach the Seller Financing Addendum with careful attention to detail and clear communication. Ensuring each section is completed fully and accurately reflects the agreement between the parties, supports a successful real estate transaction, and protects the interests of all involved.

Documents used along the form

When engaging in the complex and detailed process of seller financing in the state of Utah, the Seller Financing Addendum is a pivotal document. Yet, its effectiveness and comprehensiveness are significantly enhanced when accompanied by additional legal forms and documents. These complementary documents ensure a transparent, legally sound, and forthright transaction between the buyer and the seller.

- Real Estate Purchase Contract (REPC): This is the foundational agreement between the buyer and the seller outlining the terms and conditions of the real estate sale. It includes details such as the purchase price, property description, and contingency clauses. The Seller Financing Addendum modifies or supplements the terms of the REPC with specific financing terms agreed upon by both parties.

- Buyer Financial Information Sheet: A crucial document referenced within the Seller Financing Addendum, this form requires the buyer to disclose financial information to the seller. This allows the seller to evaluate the buyer's creditworthiness before extending financing. The form typically includes the buyer's employment details, income, assets, and liabilities.

- Amortization Schedule: Provided by the seller to the buyer, this document details the payment plan for the loan, including the amount of each payment allocated towards the principal and interest over the loan's term. It offers both parties a clear timeline of the payment expectations and the loan's maturity.

- Title Insurance Policy: While the Seller Financing Addendum stipulates that the buyer shall provide a lender's policy of title insurance, the title insurance policy itself is a separate document. It ensures the buyer's legal ownership of the property and protects against potential legal issues or claims against the property's title that may arise after the sale.

Together, these documents create a more detailed and secure framework for executing a seller-financed real estate transaction. They not only clarify the responsibilities and expectations of each party but also provide protections and assurances that facilitate a smooth and equitable exchange. Understanding and properly utilizing these documents is essential for both buyers and sellers to navigate the complexities of seller financing with confidence.

Similar forms

The "Mortgage Agreement" is a document that shares components with the Seller Financing Addendum. This agreement outlines the terms under which the lender provides funds to the borrower for purchasing real estate, similar to how seller financing allows a buyer to pay the seller directly over time. Both documents typically include details on the principal amount, interest rate, payment schedule, and the security interest in the property.

The "Promissory Note" is another document related to the Seller Financing Addendum. It serves as the evidence of debt owed by the buyer to the seller and outlines the repayment terms. This documentation is essential in both seller financing scenarios and more traditional loan settings, specifying the loan amount, interest rate, repayment schedule, and potential penalties for late payments.

An "Amortization Schedule" is typically provided with both the Seller Financing Addendum and traditional mortgage agreements. It breaks down the repayment plan into a schedule showing how much of each payment goes toward the principal balance versus interest over the life of the loan. This schedule helps both parties understand the timeline of the loan repayment and the financial obligations at each stage.

"Deed of Trust" documents are similar to the Seller Financing Addendum in scenarios where this latter is used alongside a note to secure the debt. The Deed of Trust involves a third party, the trustee, holding the title to the property until the loan is fully repaid. In seller financing, the seller may also secure their loan through similar means, ensuring they have recourse if the buyer defaults on payments.

"Real Estate Purchase Contract" (REPC) is fundamentally related to the Seller Financing Addendum since the addendum modifies or supplements the terms of the REPC. The REPC outlines the overall terms of the real estate transaction, including purchase price, closing date, and contingencies, while the Seller Financing Addendum specifically details the financing terms agreed upon between the buyer and the seller.

The "Escrow Agreement" can be related to aspects covered under the Seller Financing Addendum, particularly involving the management and disbursement of funds. In seller financing setups, an escrow agent may be appointed to manage payments from the buyer, including payment of underlying mortgages, property taxes, and insurance, ensuring that financial obligations are met timely and appropriately.

"Buyer's Disclosure" documents bear similarity to the disclosure requirements within the Seller Financing Addendum. These documents require the buyer to provide financial information and other relevant details to assess their creditworthiness. The disclosure process helps sellers decide whether to proceed with the financing arrangement, mirroring traditional loan application processes where buyers must disclose financial information to lenders.

The "Title Insurance Policy" requirement is common both in traditional mortgage agreements and under the Seller Financing Addendum. This policy protects the buyer and the seller/lender against losses resulting from disputes over property ownership and other title issues. Its inclusion ensures that the title is clear and the transaction can proceed with reduced legal risk.

Finally, the "Federal Tax Reporting Requirements" document is linked with the necessity in the Seller Financing Addendum for both parties to disclose tax identification numbers for reporting interest payments to the IRS. This requirement is a critical aspect of financing agreements, ensuring compliance with federal tax laws and enabling the proper reporting of mortgage interest payments.

Dos and Don'ts

Filling out the Seller Utah Form is a critical step in the process of a real estate transaction when seller financing is involved. Paying attention to detail and understanding the responsibilities of both parties can greatly impact the outcome. Here are things you should and shouldn't do when completing this form:

Things You Should Do

- Review All Sections Carefully: Ensure you understand each section before filling it out. This form sets important financial terms and conditions that will govern the sale.

- Confirm Credit Terms: Make sure the credit terms, including the principal amount, interest rate, and payment schedule, are clear and agreed upon by both parties.

- Provide Accurate Disclosures: Accurately complete the Buyer Disclosures and Seller Approval sections. This includes providing a current credit report and financial information sheet as required.

- Consult with Professionals: If any part of the form or process is unclear, consult with a real estate attorney or a professional with expertise in seller financing. Understanding legal and financial implications is crucial.

- Leave Sections Blank: Do not leave any sections incomplete. Each part of the form is designed to protect both seller and buyer, and omitting information can lead to misunderstandings or legal issues.

- Sign Without Agreement: Never sign the form if there are unresolved issues or if any terms are not fully understood and agreed upon. Signing the form signifies that both parties accept all terms.

- Ignore Deadlines: Failing to adhere to the provided deadlines for disclosures, credit reports, and acceptance can void the agreement or lead to penalties.

- Overlook Tax and Insurance Responsibilities: Ensure clarity on who is responsible for taxes, assessments, insurance, and other obligations. Misunderstandings here can lead to financial strain and conflict later.

By following these guidelines, both the seller and buyer can ensure a smoother and more transparent seller financing arrangement. Always prioritize open communication and legal advice when filling out and agreeing to the terms in the Seller Utah Form.

Misconceptions

When dealing with a Seller Financing Addendum in the state of Utah, understanding its components is crucial for both buyers and sellers. However, misconceptions can arise, leading to confusion and potential conflicts. Below are ten common misconceptions about the Seller Financing Addendum form in Utah, clarified to provide a clearer understanding of the process.

It's commonly believed that all seller financing transactions in Utah require a standard contract. However, the Seller Financing Addendum to the Real Estate Purchase Contract (REPC) is specifically designed for these types of transactions, ensuring that terms of the seller financing are clearly outlined and agreed upon by both parties.

Many think that the interest rate on a seller-financed loan can be arbitrarily set by the seller. The truth is, while the seller and buyer have the freedom to negotiate the interest rate, it must comply with state usury laws to avoid legal consequences.

There's a misconception that buyer's financial information is optional for seller financing. In reality, sellers typically require a Buyer Financial Information Sheet and may also request additional documentation, such as tax returns and employment verification, to assess the buyer's creditworthiness.

Sometimes, it is misunderstood that seller financing does not allow for prepayment penalties. The terms of the Addendum specify that the principal balance on the Note can be paid off early without incurring a penalty, promoting flexibility for the buyer.

A common belief is that taxes and assessments on the property are the seller's responsibility. Contrary to this belief, the Addendum distinctly places this responsibility on the buyer, including property taxes, homeowners association dues, and special assessments.

It's incorrectly assumed that the Seller Financing Addendum guarantees the seller's acceptance of financing. Seller approval is mandatory, and the seller has the right, upon reviewing the buyer's credit, to either proceed with or cancel the REPC before the due diligence deadline.

Many are under the impression that all payments made by the buyer go directly to the seller. While this can be the case, payments can also be made to an Escrow Agent, who is responsible for managing the payments effectively, including disbursing funds to cover any underlying mortgages and to the seller.

Some believe that late payment fees are standardized or fixed. The Addendum clearly states that any late payment may incur a charge, with the amount being the greater of a specified dollar amount or percentage of the installment due, underscoring the importance of punctuality in payments.

A misconception exists that buyer and seller can only communicate through their agents. By the closing date, both parties are required to disclose their Social Security Numbers or tax identification numbers directly to each other to comply with federal reporting laws, indicating direct communication is sometimes necessary and legally mandated.

Lastly, it's wrongly assumed that the Seller Financing Addendum is merely a formality without legal enforceability. This document is a legal addendum to the REPC, and once signed by both parties, it becomes a legally binding part of the purchase contract, with specific terms that modify or supersede those in the main contract if in conflict.

Understanding these common misconceptions and their corrections can help both buyers and sellers navigate the complexities of seller financing with greater clarity and confidence. It’s always recommended to seek legal advice or counseling from real estate professionals when engaging in any form of real estate transaction, including seller financing, to ensure compliance and protect the interests of all parties involved.

Key takeaways

When utilizing the Seller Utah Form, it’s essential to comprehend its purpose and provisions fully. Below are key takeaways for both buyers and sellers to consider:

- Integrating with the REPC: The Seller Financing Addendum modifies and becomes an integral part of the Real Estate Purchase Contract (REPC), shaping the terms of the sale and financing.

- Evidence of Credit: The extension of credit from the seller to the buyer must be documented through specified credit documents, like a note and deed of trust, ensuring legal clarity on the financial arrangements.

- Details of Credit Terms: The addendum outlines specific terms regarding the principal amount, interest rate, payment schedules, and any balloon payments or additional principal payments, providing a clear financial roadmap for both parties.

- Responsibility for Taxes and Other Expenses: The buyer is responsible for covering property taxes, homeowners association dues, special assessments, and hazard insurance premiums, though payment methods may vary.

- Payment and Escrow Arrangements: Payments under the seller financing terms can be made directly to the seller or an escrow agent, with arrangements for handling and disbursing payments clearly outlined.

- Late Payment and Prepayment Terms: The addendum specifies charges for late payments and conditions for prepaying the principal balance, offering flexibility while ensuring prompt payments.

- Due-on-Sale Clause: A vital protection for the seller, this clause can call the loan due if the property is sold, necessitating the buyer to approve all underlying loan documents.

- Creditworthiness and Seller’s Review: The buyer must provide financial information for the seller’s review to assess creditworthiness, including potentially supplying a credit report and IRS returns, impacting the seller's decision on proceeding with the contract.

These elements emphasize the necessity of diligence and transparency in the seller financing process, safeguarding the interests of both the buyer and the seller while providing a framework for mutually beneficial financing arrangements.

Common PDF Templates

Utah State Tax Form for Employees - Utah allows for a degree of personal expression through vehicle plates, with the TC-194 form being the gateway for this customization.

Utah Cpe Requirements - This form provides a clear outline of what qualifies as CPE, helping CPAs make informed decisions about their education.

Utah Estimated Tax Payments - Clear labeling on the TC-559 coupon facilitates the correct selection of payment type, such as estimated or return payments.