Official Utah Promissory Note Form

When entering into a borrowing agreement, individuals in Utah often rely on a legal document known as the Promissory Note. This form plays a crucial role in formalizing the terms between a borrower and a lender, serving as a binding promise for the borrower to repay the specified sum of money under agreed-upon conditions. It encompasses various critical aspects, including payment schedules, interest rates, consequences for late payments, and what happens in the event of a default. The use of a Promissory Note ensures clarity and protection for both parties involved, providing a structured and enforceable framework for the repayment of the loan. Whether used for personal loans among family members or more formal lending situations, understanding its key elements is essential for everyone involved in the transaction.

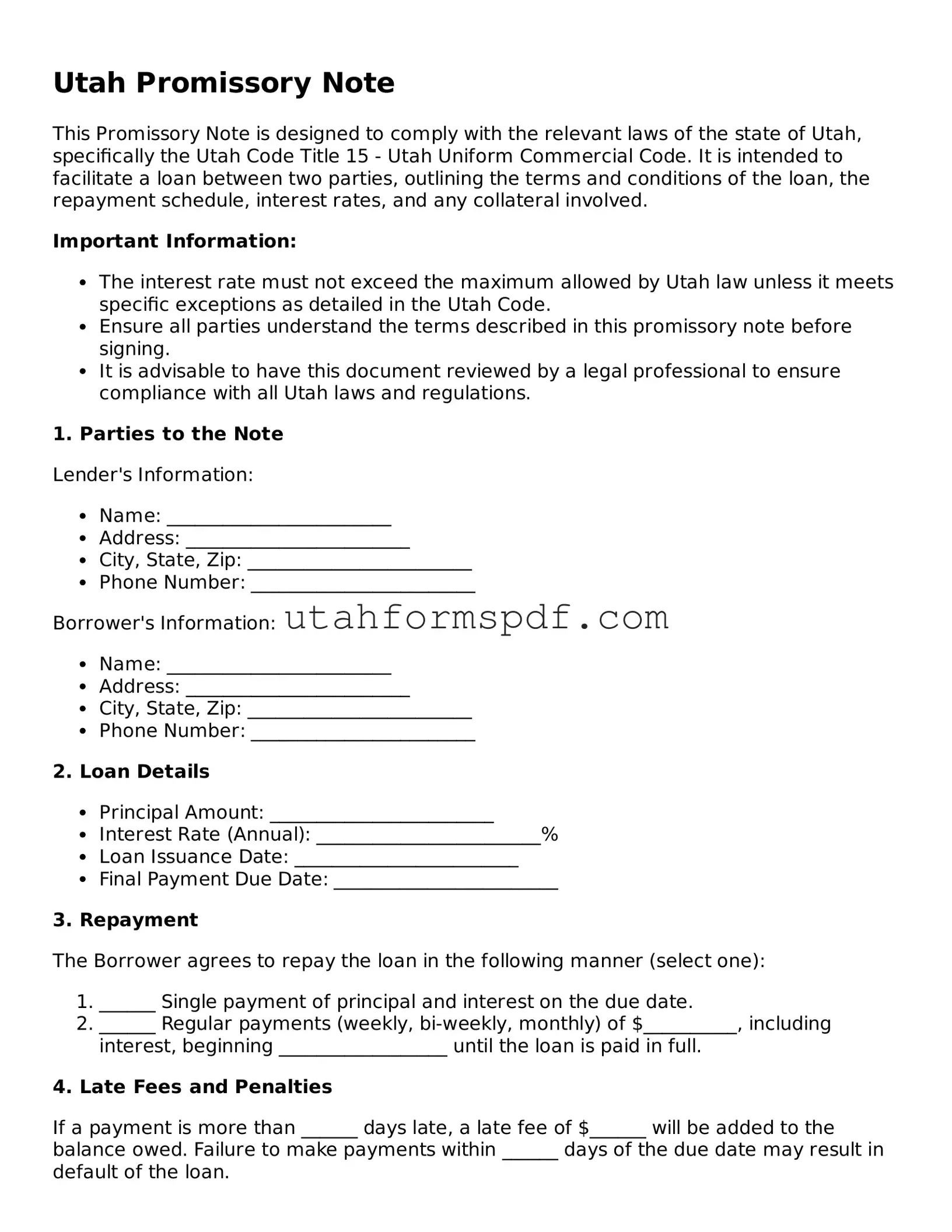

Form Preview Example

Utah Promissory Note

This Promissory Note is designed to comply with the relevant laws of the state of Utah, specifically the Utah Code Title 15 - Utah Uniform Commercial Code. It is intended to facilitate a loan between two parties, outlining the terms and conditions of the loan, the repayment schedule, interest rates, and any collateral involved.

Important Information:

- The interest rate must not exceed the maximum allowed by Utah law unless it meets specific exceptions as detailed in the Utah Code.

- Ensure all parties understand the terms described in this promissory note before signing.

- It is advisable to have this document reviewed by a legal professional to ensure compliance with all Utah laws and regulations.

1. Parties to the Note

Lender's Information:

- Name: ________________________

- Address: ________________________

- City, State, Zip: ________________________

- Phone Number: ________________________

Borrower's Information:

- Name: ________________________

- Address: ________________________

- City, State, Zip: ________________________

- Phone Number: ________________________

2. Loan Details

- Principal Amount: ________________________

- Interest Rate (Annual): ________________________%

- Loan Issuance Date: ________________________

- Final Payment Due Date: ________________________

3. Repayment

The Borrower agrees to repay the loan in the following manner (select one):

- ______ Single payment of principal and interest on the due date.

- ______ Regular payments (weekly, bi-weekly, monthly) of $__________, including interest, beginning __________________ until the loan is paid in full.

4. Late Fees and Penalties

If a payment is more than ______ days late, a late fee of $______ will be added to the balance owed. Failure to make payments within ______ days of the due date may result in default of the loan.

5. Prepayment

The Borrower has the right to pay off the loan in advance without incurring any penalties.

6. Governing Law

This Promissory Note will be governed under the laws of the state of Utah.

7. Signature

By signing below, both the Lender and Borrower agree to adhere to and be bound by the terms of this Promissory Note. This document, along with any attachments or addendums, represents the entire agreement between the parties.

Lender's Signature: ________________________ Date: ________________________

Borrower's Signature: ________________________ Date: ________________________

Witness's Signature (if applicable): ________________________ Date: ________________________

PDF Form Details

| Fact Name | Description |

|---|---|

| Definition | A Utah Promissory Note is a legal agreement in which a borrower promises to repay a loan to a lender according to specified terms. |

| Governing Laws | These forms are governed by Title 15 of the Utah Code, which lays out the state’s laws on contracts and commercial transactions. |

| Types | There are primarily two types of promissory notes in Utah: secured and unsecured. Secured notes are backed by collateral, while unsecured notes are not. |

| Interest Rate Limit | Utah law caps the maximum interest rate at 10% per annum if not specified in the agreement, as per Utah Code §15-1-1. |

| Legal Requirements | The note must include the loan amount, interest rate, repayment schedule, and parties' signatures to be legally enforceable. |

Detailed Steps for Writing Utah Promissory Note

When preparing to fill out a Utah Promissory Note form, it's important to gather all necessary information ahead of time. This document is a binding agreement between a borrower and a lender, detailing the borrower's promise to pay back a specified sum of money to the lender. Accuracy and attention to detail are crucial to ensure the agreement is enforceable and reflects the terms agreed upon by both parties. Follow these steps to correctly complete the form.

- Start by entering the date at the top of the form. This marks when the promissory note becomes effective.

- Fill in the full legal names of the borrower and the lender in the designated spots. If there are co-borrowers, include their names as well.

- Specify the principal amount of money being loaned. Write this both in numerical form and spell it out to avoid any confusion.

- Detail the interest rate annually (APR) agreed upon by both parties. If the interest rate is variable, clearly describe how it will be calculated.

- Outline the repayment schedule. Include the number of payments, the amount of each payment, and the due dates for these payments. Mention if the payments are monthly, quarterly, or as otherwise agreed.

- If there is a provision for late fees, specify the amount of the fee and the grace period before the fee is applied after a missed payment.

- Address the method of payment. Clarify whether payments will be made by check, electronic transfer, or another method.

- Include clauses regarding prepayment. This refers to whether the borrower can pay off the balance early and if there are any penalties for doing so.

- Sign and date the form. The borrower(s), lender, and any co-signers must sign the note for it to be valid. Including the date next to each signature is essential.

- If applicable, have the promissory note notarized. Some promissory notes require notarization to be legally binding. Check local laws or consult with a lawyer to see if this step is necessary for your situation.

Once the Utah Promissory Note form is fully completed and signed by all parties, it becomes a legally binding document. Each party should keep a copy for their records. The form outlines the terms of the loan, ensuring clarity and agreement on the repayment plan. For further legal protection, consider having the document reviewed by a legal professional.

Common Questions

Frequently Asked Questions about the Utah Promissory Note Form:

What is a Promissory Note?

A promissory note is a written agreement, promising to repay a debt under specified conditions including the repayment schedule, interest rate, and the signatures of both the lender and the borrower. In Utah, such a note forms a legally binding contract specific to the repayment of money.

Do I need a lawyer to create a Utah Promissory Note?

While it’s not strictly necessary to have a lawyer to draft a promissory note in Utah, consulting with one can ensure the document meets all legal requirements and protects the interests of both parties. Complex lending situations may especially benefit from professional legal advice.

What should be included in a Utah Promissory Note?

A comprehensive Utah promissory note should include the total loan amount, interest rate, repayment schedule, details of the parties involved (lender and borrower), collateral details (if secured), and governing state laws. Additionally, including signatures of both parties is crucial for enforceability.

Is a written Promissory Note always required in Utah?

While verbal agreements can be legally binding, a written promissory note is highly recommended in Utah. It serves as a tangible record of the terms agreed upon, reducing misunderstandings and providing a clear basis for legal proceedings if needed.

Can I charge any interest rate on a loan in Utah?

Utah law permits lenders to charge interest, but rates must comply with state regulations to avoid being deemed usurious. It’s important to check the current legal limits on interest rates in Utah before finalizing your promissory note.

How is a Promissory Note enforced in Utah?

In the event of non-payment, the holder of a promissory note in Utah can initiate legal action to enforce the document. Enforcement may lead to the recovery of the owed amount, potentially through the seizure of collateral (in the case of a secured note) or other remedies permitted by law.

Can I modify a Promissory Note after signing it?

Yes, a promissory note can be modified after it has been signed, but any modifications must be agreed upon by all parties involved. It’s advisable to document any amendments clearly and have them signed by the lender and borrower.

Common mistakes

Filling out a Utah Promissory Note form is an important step in formalizing a loan between two parties. However, it's not uncommon for individuals to make mistakes during this process, which can lead to misunderstandings or legal complications down the line. Here are eight common mistakes to watch out for when completing a Utah Promissory Note form.

Not specifying the loan amount in clear terms. It's crucial to write the exact loan amount in both numerical and written form to ensure clarity. Omitting this information or presenting it vaguely can cause confusion regarding the actual loan amount agreed upon.

Forgetting to include the interest rate. The interest rate must be clearly stated and agreed upon by both parties. This rate should comply with Utah's legal limits to avoid any issues of usury, which concerns charging an excessively high interest rate.

Omitting the repayment schedule. Detailing how and when repayments will be made (e.g., monthly installments, lump sum at a specific date) is essential. Without this, there’s no clear agreement on how the borrower is expected to fulfill their debt obligations.

Leaving out the consequences of late payments. It’s important to outline any late fees or penalties for missed payments within the promissory note. These terms provide an incentive for timely repayment and clarify the ramifications of failing to pay as agreed.

Not identifying parties correctly. Full legal names and contact information for both the borrower and the lender should be clearly listed. This mistake can lead to significant issues, especially if a dispute arises and legal action is required.

Failing to detail the security, if any, for the loan. If the loan is secured with collateral, this should be described in detail, including what happens if the borrower defaults. Without this information, the lender’s rights to the collateral can be unclear.

Forgetting to include a clause about prepayment. Terms regarding whether the borrower can pay off the loan early and, if so, whether there's a penalty for doing so should be specified. This provides flexibility and clarity for both parties.

Neglecting to have the document witnessed or notarized, if required. While not all Utah promissory notes need to be notarized, doing so can add an extra layer of validity. Failing to comply with the appropriate witnessing or notarization requirements can potentially weaken the enforceability of the document.

When individuals are careful to avoid these mistakes, they help ensure that the promissory note is both clear and legally binding. This protects the interests of both the borrower and the lender, reducing the potential for misunderstandings and legal issues in the future. It's always a good idea to review the completed promissory note carefully and possibly consult with a legal professional to ensure that it meets all legal requirements and accurately reflects the agreement between the parties.

Documents used along the form

When preparing a Utah Promissory Note, it is often necessary to complete and gather additional documents to ensure a comprehensive and enforceable agreement. These documents can provide clarity, legal protection, and define more detailed aspects of the financial transaction. Below is a list of forms and documents that are commonly used alongside the Utah Promissory Note form.

- Loan Agreement: Outlines the broader terms and conditions of the loan, including the responsibilities of both the lender and borrower beyond the repayment schedule.

- Security Agreement: Used when the loan is secured by collateral, detailing the rights to the collateral if the borrower defaults.

- Guaranty: A form signed by a third party, guaranteeing they will assume the debt obligation if the borrower cannot make repayments.

- Amortization Schedule: Provides a detailed breakdown of each payment throughout the life of the loan, including how much goes toward the principal and how much toward interest.

- Mortgage Agreement: Applies if the loan is used to purchase real estate, securing the loan with the property as collateral.

- Deed of Trust: Similar to a mortgage agreement but involves a third party, which holds the title until the loan is paid in full. Used in some states as an alternative to a mortgage.

- UCC-1 Financing Statement: Filed by the lender to publicly declare their right to potential ownership of the borrower's collateral. Required for secured loans involving personal property.

- Notice of Default: A formal notification sent to the borrower indicating a default on the loan, often the first step in the foreclosure process.

- Release of Liability: Used once the loan is fully repaid, releasing the borrower from any further obligation to the lender.

- Co-Signer Agreement: An agreement that includes a co-signer on the loan, providing additional security for the lender that the loan will be repaid.

Collecting and properly executing these documents can be crucial for the protection of both parties involved in a loan agreement. The right combination of forms serves to clear any ambiguities regarding the terms of the loan, the responsibilities of each party, and the procedures for dealing with default or other issues that may arise. Therefore, it is always recommended to consider which additional documents should accompany the Utah Promissory Note to ensure a smooth and secure transaction.

Similar forms

The Utah Promissory Note form shares similarities with the Loan Agreement. Both documents serve as legally binding agreements between two parties about a sum of money to be borrowed and repaid under specific terms. Like the Promissory Note, a Loan Agreement details the loan amount, interest rate, repayment schedule, and the consequences of non-payment. However, a Loan Agreement typically includes more comprehensive terms regarding the responsibilities and obligations of both lender and borrower, making it more complex.

Mortgage Agreements bear resemblance to the Utah Promissory Note form as well, especially since they both establish an obligation to repay borrowed money. The main difference lies in the fact that a Mortgage Agreement specifically uses real estate as collateral to secure the loan. If the borrower fails to repay the loan, the lender has the right to take possession of the property. Despite this difference, both documents outline payment terms, interest, and the conditions under which the borrower must repay the borrowed funds.

Another document similar to the Utah Promissory Note form is the Personal Loan Agreement. This type of agreement is used when an individual borrows money from another person or a financial institution. Like the Promissory Note, a Personal Loan Agreement includes the amount borrowed, interest rate, repayment schedule, and the consequences for failing to repay. The primary difference is that Personal Loan Agreements are often less formal and used for smaller, personal loans rather than business or commercial loans.

The IOU (I Owe You) document also shares characteristics with the Utah Promissory Note. Both are written acknowledgments of debt. However, an IOU is much simpler, typically consisting only of the amount owed and the debtor's name. Unlike the Promissory Note, IOUs generally lack detailed terms of repayment, interest, and legal protections for the lender, making them less enforceable in a court of law.

Lines of Credit Agreements are similar to the Utah Promissory Note in that they allow borrowers to access funds up to a certain limit and require repayment. The key difference is that a Line of Credit Agreement offers ongoing access to funds, whereas a Promissory Note applies to a single lump sum of money. Despite this, both documents will specify repayment terms, interest rates, and security, if applicable.

The Student Loan Agreement is another document that parallels the Utah Promissory Note form, particularly in the context of borrowing money for education. Both agreements outline the terms under which money is borrowed and repaid, including the interest rate and repayment schedule. However, Student Loan Agreements often contain specific provisions related to the borrower's status as a student, such as deferment options and conditions tied to academic performance or graduation.

Credit Card Agreements share certain similarities with the Promissory Note as both involve borrowing money that must be repaid to the lender under agreed-upon terms. While a Promissory Note is generally straightforward, detailing the repayment of a fixed amount, Credit Card Agreements are more complex, covering credit limits, variable interest rates, minimum payments, and fees. Despite their differences, both documents are legally binding and contain provisions for interest and repayment.

The Bill of Sale is somewhat akin to the Utah Promissory Note form in that it serves as a written record of a transaction between two parties. However, while a Promissory Note documents a promise to pay a sum of money, a Bill of Sale confirms the transfer of ownership of an item from a seller to a buyer. Although the purposes of these documents differ—one for borrowing and one for buying—they both provide legal evidence of an agreement between two parties.

Dos and Don'ts

When it comes to filling out the Utah Promissory Note form, precision, clarity, and adherence to legal standards are key. To ensure that you navigate this process effectively, here are some do's and don'ts that can guide you:

- Do:

- Double-check the accuracy of names and addresses of both the borrower and lender to prevent any misunderstandings or misidentifications.

- Clearly specify the loan amount in words and numbers to ensure there is no confusion about the total sum being borrowed.

- Outline the repayment schedule in detail, including due dates, amounts, and the final payment date, to avoid any ambiguities.

- Include the interest rate, stating whether it's fixed or variable, to make sure both parties are clear about the cost of borrowing.

- Mention any collateral securing the loan if applicable, providing a clear description to safeguard the lender's interests.

- State the governing law that will apply to the agreement, noting that Utah law will govern the promissorry note to ensure legal clarity.

- Both borrower and lender should sign the document to validate the agreement legally and officially.

- Consult with a legal professional if there's any uncertainty about the promissory note's terms or its implications.

- Don't:

- Leave any sections incomplete, as this could lead to disputes or legal challenges down the line.

- Use vague language that could be open to interpretation; be as specific as possible to ensure clarity.

- Forget to specify the penalty for late payments, as this is crucial for enforcing the agreement.

- Neglect to outline the conditions under which the loan would be considered in default to protect both parties' interests.

- Overlook the requirement to have witnesses or a notary public present at signing if required by Utah law, to ensure the document's enforceability.

- Make alterations or addenda to the document without the agreement and signatures of both parties, as any changes made unilaterally could be contested.

- Fail to provide a copy of the signed document to the borrower, as both parties should have a copy for their records.

- Rely solely on verbal agreements or assurances; everything should be documented in writing within the promissory note.

By following these guidelines, you can help ensure that your Utah Promissory Note is comprehensive, clear, and legally enforceable. This will provide both the borrower and the lender with peace of mind and a clear framework within which the loan will be repaid.

Misconceptions

One common misconception is that a Utah Promissory Note form must be complicated to be legally valid. The truth is, for a promissory note to be considered valid in Utah, it needs to include the basic elements of the agreement such as the amount borrowed, the interest rate, and repayment terms. Keeping it straightforward often avoids misunderstandings.

Many believe that only loans involving large sums of money necessitate a promissory note. This isn’t accurate. Any amount of money lent, regardless of its size, can benefit from the clarity a promissory note provides. It formalizes the loan, making it clear it's not a gift.

There's a misconception that promissory notes are only for transactions between strangers or businesses. However, promissory notes can also be extremely useful in transactions between friends or family members, helping to preserve relationships by clearly documenting obligations.

Some think that a lawyer is required to draft a promissory note. While legal advice can certainly be beneficial, especially for large or complex loans, it's not a necessity. Various templates can provide a good starting point, ensuring you include all essential information.

Another incorrect belief is that promissory notes in Utah are the same regardless of the loan's purpose. In fact, depending on whether the loan is for personal purposes, a business transaction, or even real estate, certain specific provisions might need to be included to comply with relevant Utah laws.

It’s a common misunderstanding that a promissory note by itself is enough to secure a loan. If lenders want assurance beyond the borrower's promise to pay, they should consider securing the loan with collateral and mention this in the promissory note, creating a secured promissory note.

Many people incorrectly assume that if the borrower signs the promissory note, it negates the need for any witnesses or notarization. While not always legally required, having the document witnessed or notarized can add an extra layer of legitimacy and may be helpful in the event of a dispute.

There's a misconception that a promissory note is binding the moment it's written. In reality, it must be agreed upon and signed by all parties involved to be legally binding. Both the lender and borrower need to understand and agree to the terms set forth in the document.

Finally, some believe that once signed, the terms of a Utah Promissory Note cannot be changed. This isn't the case. Both parties can agree to modify the terms of the note at any point, as long as both consent to the changes. Such amendments should be documented in writing and attached to the original note.

Key takeaways

When dealing with the Utah Promissory Note form, it's essential to understand its significance and the proper way to fill it out. This form is a legal agreement between a borrower and a lender, detailing a loan's repayment terms. To ensure clarity and prevent any future disputes, here are nine key takeaways to consider:

- Identify the Parties Clearly: Make sure to include the full legal names and addresses of both the borrower and the lender. This makes it clear who is involved in the agreement.

- Determine the Loan Amount: The principal amount of the loan should be specified accurately. This is the amount the borrower promises to repay, not including interest.

- Clarify the Interest Rate: Utah law allows for interest to be charged, but rates must comply with state regulations to avoid being considered usurious. The annual interest rate should be clearly defined.

- Set Repayment Terms: Detail how the loan will be repaid. This includes the repayment schedule, whether in monthly installments or a lump sum, and the due date for the final payment.

- Include Consequences of Default: Specify what constitutes as default on the loan, and the steps the lender is entitled to take if the borrower fails to meet the agreed upon terms.

- Detail Any Security: If the loan is secured by collateral, describe the collateral in detail. This provides the lender with assurance that the borrower has a strong incentive to repay the loan.

- Right to Prepayment: State whether the borrower has the right to pay off the loan early and if any prepayment penalties apply. This could save the borrower on interest expenses.

- Governing Law: Mention that the promissory note is governed by the laws of Utah. This ensures that any legal disputes will be resolved under Utah law.

- Signatures: Both the borrower and the lender must sign the promissory note for it to be legally binding. Include a place for the date of the agreement next to the signatures.

Understanding and accurately completing the Utah Promissory Note form is crucial for both parties involved. It lays the groundwork for a straightforward and enforceable agreement. Taking the time to review and verify that all aspects of the promissory note are correct can prevent misunderstandings and legal issues down the line.

Other Utah Forms

Notice to Tenant - By using a Notice to Quit, landlords signal the importance of adhering to lease terms and the consequences of failing to do so.

How to Fill Out a Bill of Sale Utah - Essential for maintaining an accurate history of the trailer’s ownership for future reference.

Utah Rental Application - May include specific questions regarding tenant’s lifestyle or pet ownership to ascertain compatibility with rental policies.